Download

1 / 33

410 likes | 831 Views

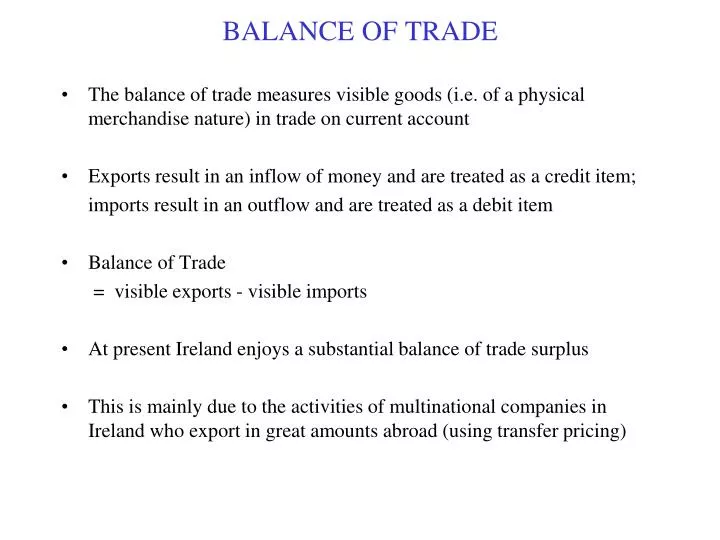

BALANCE OF TRADE. The balance of trade measures visible goods (i.e. of a physical merchandise nature) in trade on current account Exports result in an inflow of money and are treated as a credit item; imports result in an outflow and are treated as a debit item Balance of Trade

E N D

BALANCE OF TRADE • The balance of trade measures visible goods (i.e. of a physical merchandise nature) in trade on current account • Exports result in an inflow of money and are treated as a credit item; imports result in an outflow and are treated as a debit item • Balance of Trade = visible exports - visible imports • At present Ireland enjoys a substantial balance of trade surplus • This is mainly due to the activities of multinational companies in Ireland who export in great amounts abroad (using transfer pricing)

BALANCE OF PAYMENTS • The balance of payments includes invisible items in trade • Factor flows relate to money which is earned in one country yet repatriated to another - in Ireland multinational companies make large profits which are repatriated overseas (mainly US) leading to a negative flow; repatriation back home from Irish companies abroad would lead to a positive flow - repayment of interest on foreign debt would also lead to a negative flow - in past emigrants remittances were received in large amounts from Irish workers abroad • Services e.g. tourism, financial services, software development now increasingly are traded internationally. • Overall, services is now greater in value than merchandise trade with Ireland ranked 9th in the world for exports of services - There are very large invisible exports in software (with Ireland ranked no. 1 internationally in this category - however equally there are large invisible imports with respect to consultancy services and royalty payments by multinational companies

BALANCE OF PAYMENTS (con) • Invisible payments also arise due to international transfers of funds • Ireland is a member of the EU and contributes to and receives money from the EU budget - in past Ireland received much more from budget than it contributed - however because of substantial income growth during the Celtic Tiger years we are contributing more and receiving less • Overall there is a massive deficit on invisible trade in Ireland • This largely wipes out the surplus on the trading balance so that we now have just a small surplus on the balance of payments • Balance of Payments (on current account) = (visible + invisible exports) – (visible + invisible imports)

BASIC BALANCE • Trade also takes place in capital items • Long term capital transactions involve activities such as investment by foreign companies in Ireland and Government foreign borrowing (for capital purposes) • Short terms capital transactions reflect financial activity of stock markets • Capital transactions by their nature tend to be very volatile • When net capital transactions are added to current we get the overall balance of payments) referred to as the Basic Balance • In the past corrective action had to be taken by governments when a large basic balance existed - now because of membership of the Eurozone the overall balance for this bigger region is more important

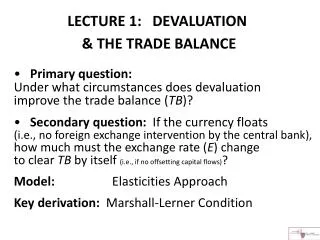

DEFINITION OF EXCHANGE RATES • An exchange rate measures the value of one currency in terms of another • As with goods and services, the values of a currency against another is determined by demand and supply • When goods are exported from Ireland payment must be made in our currency (i.e. the euro) • When goods are imported into Ireland - say from the UK - payment must be made in the UK’s currency (i.e. sterling) • When the euro rises - say against sterling or the dollar - it becomes more expensive to sell goods in the UK and the US (but cheaper to import from these countries) • When the euro falls against these currencies it becomes cheaper to sell abroad but more expensive to import

EXCHANGE RATES (con) • Factors determining exchange rates - demand for exports and imports- inflationary pressures- changes in interest rates- speculation- political factors • Intervention on Foreign Markets - using reserves- borrowing abroad- raising interest rates- deflationary policy- supply-side policies- controls on imports

c d QD QS Determination of the rate of exchange S by UK $ price of £ D by USA Q of £

EXCHANGE RATES • Fixed - absolutely fixed - adjustable pegs - crawling pegs • Floating - pure - managed • Basket of Currencies - composite mix of currencies - examples

FIXED RATES • Advantages - creates more certain environment for trade - reduces speculation • Disadvantages - creates strains in terms of managing Balance of Payments - not in keeping with market approach - can lead to instability and damaging devaluations (and revaluations)

External Reserves • European Central Bank’s reserve assets, December 2000 € billions % • Foreign exchange 234.1 59.5 • SDR 4.3 1.1 • Reserve position at IMF 20.8 5.3 • Gold 117.8 29.9 • Other claims 16.4 4.2 • Total 393.4 100.0 • Source: European Central Bank, Monthly Bulletin, November 2001, Table 8.7. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Fixed versus Floating Exchange Rates • Advantages of free-floating rates • automatic correction • no problem of international liquidity • insulation from external events • less constraint on domestic macro policy • Disadvantages of free-floating rates • possibly unstable exchange rates • speculation • uncertainty for business but use of forward markets • lack of discipline on economy

Fixed Exchange Rate Systems • Gold Standard (1870 – 1914): • Currencies fixed to gold. • Bretton Woods (1945-71): • $ fixed to gold ($35/1 ounce). All other currencies fixed to $. • Establishment of IMFand World Bank. • Snake System ( 1973-78): • European currencies held inside a band of +/- 1.125% around a central rate. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Gold Standard (1870-1914) • Currencies fixed to gold. • Automatic adjustment mechanism which removes BP surpluses or deficits. • BP (-) currency outflow Ms P improvement in competitiveness removal BP (-) • Note incorporation of Quantity Theory. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Exchange Rates and Balance of Payments • Exchange rates and the balance of payments: government intervention • reducing short-term fluctuations • using reserves • borrowing from abroad • changes in interest rates • maintaining a fixed rate of exchange over the longer term • deflation / reflation • supply-side policies • import controls

FEATURES OF ECONOMIC UNION Single market for persons, goods, services and capital High level of co-ordination of economic policy - esp. central control of fiscal policy Greater role for competition policies Structural Funds - transfer of funds to weaker countries

FEATURES OF MONETARY UNION Total and irreversible convertibility of currencies Complete liberalisation of capital movements Full integration of banking and other financial markets Elimination of margins of fluctuation and irrevocable locking of exchange rates (implying a single currency)

ADVANTAGES OF EMU Symbolic of overall union Would reduce transaction costs for business Would eliminate uncertainty due to exchange rate adjustments facilitating trade Individual countries do not have to hold reserves as all are pooled Would encourage more co-ordination of economic policies Beneficial effects on efficiency Currency would become international reserve asset Help to reduce interest rates Help to reduce inflation Could facilitate overall growth and employment in Community

Why Join EMU? Economic Benefits • 1. Completing the internal market. • A. Single currency increases price transparency. • Should lead to a convergence of prices in Eurozone. • Indirect taxes still a serious problem. • B. Elimination of exchange rate transaction costs. Savings of about 0.5% of GDP. • Downside is a fall in earnings in financial sector. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • 2. Reduction in exchange rate uncertainty. • Should stimulate trade and investment. • But little evidence to support this view. Trade between USA and Japan has grown dramatically even though the exchange rate is flexible. • Also 60-70 per cent of Irish trade is outside the Eurozone. Still very exposed to swings in the dollar and sterling exchange rates. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • 3. Scale economies. • Firms spread plants around Europe to hedge against currency movements. Now build plants to reap economies of scale. • Lead to regional specialisation and an efficiency gain. • However, peripheral regions could suffer a decline as firms shift to the centre. • Could be a cost as far as Ireland is concerned. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • 4. Low inflation. • Inflation is determined by the ECB. Given the single currency, this inflation rate should be transmitted (on average) to the rest of the Eurozone. • In effect, Irish inflation has diverged considerably from EU rate. • Argued that this is better than an anti-inflation policy based on internal rules (doing it for ourselves). • Note that Ireland had achieved a low inflation rate prior to EMU entry. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • 5. Low interest rates. • Given the single currency, there can be only one interest rate in the Eurozone. • The current rate represents a significant fall for high interest rate countries like Ireland, Spain, Portugal and Italy. • In 2002, real interest rates were negative in several Eurozone countries. • Represents a transfer of resources from savers to borrowers. • Also major implications for macroeconomy. Leddin and Walsh Macroeconomy of the Eurozone, 2003

POSSIBLE DISADVANTAGES Considerable loss in national sovereignty Effects might not be equally spread throughout Community Possible difficulties in dealing with crisis situations No guarantees in relation to stability of currency in relation to other world currencies Special problems for Ireland (in relation to UK and US currencies)

Costs Associated with EMU Membership • 1. Transition costs. • A. £1 = €1.269738 or €1 = £0.787564. Euro prices are 27% higher. • Introduced on the basis of “new currency – same price”. • Does not appear to be the case. Survey by the Consumer Association of Ireland found that the euro resulted in price rises in a whole range of products and services. • B. Cost to banks is around £130 m +. • C. Cost of adopting new international payments system. • D. Cost of withdrawing domestic notes and coins. Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • 2. Problem of adjustment within a monetary union. • Economy can suffer asymmetric shocks. • For example, swings in sterling and dollar exchange rate, foot and mouth disease, downturn in US economy, September 11th. • In EMU, countries no longer have control over the money supply, interest rates or the exchange rate. • Also fiscal policy is constrained by the Stability Pact. • Represents a considerable loss of economic independence. • A country may find itself in recession and be unable to do anything about it. • Raises key issues regarding present EU response to deepening recession? Leddin and Walsh Macroeconomy of the Eurozone, 2003

Continued • EMU results in a loss of economic independence. • No longer has a country control over money supply, interest rates or the exchange rate. Fiscal policy is constrained by the Growth and Stability Pact. • Means the burden of adjustment switches from monetary and fiscal policies to the “wage adjustment” effect and an “international competitiveness” effect. • But the labour market is much less flexible than the money market (and good reasons to believe that it has proven ineffective with respect to adjustment in Ireland). • Result is that the economy may be slow to adjust. • Booms and recession may last longer giving rise to the possibility of abrupt or “hard” landings. Leddin and Walsh Macroeconomy of the Eurozone, 2003

EMU AND IRELAND (Con) Economic Benefits - completing internal market - price transparency - reduced transactions costs - reduction in exchange rate uncertainty - scale economies Economic Costs - transition costs - difficulty in adjusting to shocks - loss of fiscal autonomy - loss of economic independence - loss of unemployment/inflation trade-off

EMU (PRESENT PROBLEMS) During early years of Euro currency, banks from all countries had access to a huge largely unregulated market for both loaning and borrowing funds In some countries, such as Ireland huge bank debts arose as result of property crash; however this problem was not confined to Ireland with the bulk of these loans relating to lending by other EU banks (esp. UK, Germany and France) Official policy of the ECB - fearing a huge possible bank problem in many countries – initially was that all bank loans (to senior bondholders) should be fully honoured and was enforced in Ireland. This policy was totally unfair however from a social perspective as it placed all the burden of adjustment on shareholders and (innocent) taxpayers while not penalising the rash lending policies of the EU banks which significantly contributed to this problem Huge burden of adjustment now being felt by peripheral economies (such as Greece, Ireland and Portugal) then Spain and Italy and more recently Cyprus as the stronger economies such as France and Germany seek to protect national interests. Lack of sufficient political integration is endangering the future of the Euro which now requires radical interventions to stem market fears

EMU (PRESENT PROBLEMS con.) Possible responses would include - a dramatic increase in size of European Satbility Mechanism (ESM) that has European Finance and Stability Facility (EFSF) and European finacial stabilisation Mechanism (EFSM) to meet possible costs of bailing out larger economies such as Spain and Italy. (This however is likely to be resisted strongly by Germany which would be expected to be main contributor). - a reversal of traditional ECB policy towards quantitative easing (as has happened in US). This would enable the ECB to effectively create additional money which then could be used to buy bonds (at lower interest rates than market) from countries that are finding it presently expensive to borrow. However this would also be likely to sharply increase inflation (though this would have the virtue of reducing the real cost for countries like Ireland of redeeming debt). Though some relaxation has taken place under Mario Draghi, once again this proposal is likely to be resisted strongly by Germany and will only be considered in the context of substantial tightening of fiscal controls agreed to when signing the new fiscal Treaty (the fiscal compact). - the issuance of a common Euro bond (backed by all Eurozone countries) for at least a significant proportion of a country’s borrowing needs. However this would mean higher rates of interest for countries such as Germany (who once again are opposed to this idea). - The imposition of austerity through a significant increase in intervention by the EU in each member’s domestic fiscal policy and banking policy controlling all key targets and decisions. Though favoured by Germany this would lead to a considerable loss of national sovereignty (and be resisted by member governments). Also it would significantly increase danger of recession throughout Europe.

EMU (PRESENT PROBLEMS con.) - the large scale default of commitments to senior bondholders at both a private banking and - possibly - sovereign level. Many observers believe that Ireland will eventually be forced down this route. However the possible implications both political and economic are hard to forecast Acceptance that the Eurozone is not working in its present form preparing the way for its possible breakup. One favoured scenario would see the stronger economies (inc, Germany, France, Austria, Holland, Finland, Luxembourg form a hard Euro would other economies possibly including Ireland former a softer Euro (that would initially undergo considerable devaluation against the hard currency). Another scenario would have strong countries like Germany leaving to once again restore their national currency with other countries continuing in a more flexible Eurozone. Another possibility is that the weaker peripheral economies would leave reverting to national currencies that would eventually try and track the Euro. What Ireland would take in this scenario is very difficult to say as there are problems with all possible options

PRESENT PROBLEMS (and Ireland) Ireland is still in a bail-out programme involving the troika (the EU Commission, the ECB and the IMF) which it hopes to exist later this year. This entails brining the Government deficit down to accepted levels of 3% GDP by 2015. At present deficit is still close to 9% Crucial to this is success achieved through obtaining debt relief through renegotiation of a promissory note for Anglo Irish debt currently costing over €3 bl. each year and also renegotiation payment terms for troika money lent to Ireland. Compensation for the €30 bl. Taxpayers, money put into the pillar banks for recapitalisation looks more difficult to achieve. New European Stability Mechanism (ESM) has been created to help EU countries in financial difficulty. However it is highly unlikely that this will be used retrospectively to help with Irish banking issues Though Irish exports have performed very strongly in recent years a return of economic growth is likely to be greatly hampered through a deepening of recession within the EU with the German economy now expected to grow by just 0.4% next year.