Download

1 / 4

40 likes | 192 Views

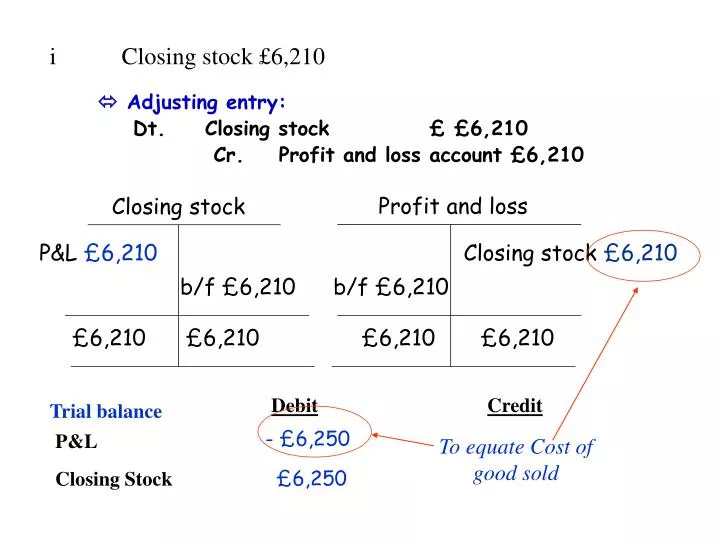

i Closing stock £6,210. Adjusting entry: Dt. Closing stock £ £6,210 Cr. Profit and loss account £6,210. Closing stock. Profit and loss. P&L £6,210. Closing stock £6,210. b/f £6,210. b/f £6,210. £6,210. £6,210. £6,210. £6,210. Debit Credit P&L. Trial balance.

E N D

i Closing stock £6,210 • Adjusting entry: • Dt. Closing stock £ £6,210 • Cr. Profit and loss account £6,210 Closing stock Profit and loss P&L£6,210 Closing stock £6,210 b/f £6,210 b/f £6,210 £6,210 £6,210 £6,210 £6,210 DebitCredit P&L Trial balance - £6,250 To equate Cost of good sold Closing Stock £6,250

ii £60 of insurance is prepaid Adjusting entry: Dt Prepaid Insurance xx Cr Insurance xx Insurance Prepaid Insurance Cash/Bank £860 Prepaid Ins £60 Insurance £60 b/f £60 b/f £800 £60 £860 £860 £60 DebitCredit Insurance£860 Trial balance £60 New Balance Prepaid Insurance - £60 = £800

e. During the first month Family Health Care earns patient fees of RM5,500 in cash. Assets = liability + Owner equity Cash Land Equipt. = Note + Capital earning Payable stock Bal. 9,000 12,000 5,000 = 20,000 6,000 e. 5,500 5,500 fees Bal. 14,500 12,000 5,000 = 20,000 6,000 5,500