Download

1 / 9

90 likes | 222 Views

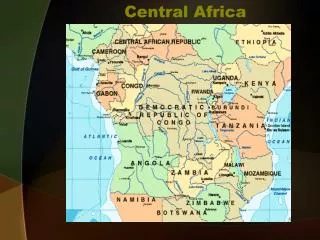

Rural finance WCA Strategy & Action Plan. M. Manssouri, Country Program Manager Implementation Workshop, Bamako, 8-11 March 2005. Western and Central Africa. Regional Context. Benin Burkina Faso Cape Verde Cameroon Central African Republic Chad Congo Democratic Republic of Congo

E N D

Rural finance WCA Strategy & Action Plan M. Manssouri, Country Program Manager Implementation Workshop, Bamako, 8-11 March 2005 Western and Central Africa

Regional Context • Benin • Burkina Faso • Cape Verde • Cameroon • Central African Republic • Chad • Congo • Democratic Republic of Congo • Côte d'Ivoire • Equatorial Guinea • Gabon • the Gambia • Ghana • Guinea • Guinea-Bisseau • Liberia • Mali • Mauritania • Niger • Nigeria • Sao Tome and Principe • Senegal • Sierra Leone • Togo • Presently, IFAD has a loan portfolio of approximately USD 3.35 billion in 90 countries. • The Western and Central Africa Division currently manages an active portfolio of 51 loan projects totalling about USD 610 million in 16 countries. • About 1/3 of IFAD resources have historically been devoted to rural finance.

Rural finance in the Region: From Unsustainable Projects to Integrated Systems MFI Commercial Bank Integration Development Bank MFI Project Viability Outreach Linkages Sustainability (participation, Interest Rate) 1980’s Centralized Systems (Top-down approach) 1990’s Development of Decentralized Systems 2000’s Integrated Systems Development

Recurrently Insufficient Access to Rural finance in the region Lack of access to capital (for income-generating activities, schooling, emergency situations, social obligations…) Integrated projects with credit component Official agricultural credit institutions Commercial Banks Informal savings & credit mechanisms Disappointing results in terms of repayment, sustainability and impact Problems of interference and low repayment rates is discouraging Cannot adapt their financial products to the needs of poor and isolated clients Exist but are insufficient

Rural Finance in The Region : Insufficient Access in Rural Areas • West Africa • 272 MFIs reaching 2,351,800 clients • ECOWAS zone: 20% of households have access to MFI services. • MFIs have strong rural tradition (esp. in cash crops) • Central Africa • 1,034 MFIs reaching 414,000 clients • CEMAC zone: 8% of households have access to MFI services • MFIs are mainly urban • Few MFIs have reached financial self-sufficiency. Only 40% of MFIs achieved operational self-sufficiency • The need for capacity and institutional building far exceeds the need for capital

THIS WAY CAUTION ! STOP Bob's.ppt http://www.geocities.com/bkip20002/index.html Graphics by Bob http://home.att.net/~kip20002/ Lessons learned: From unsustainable project to sustainable institutions • Credit provision within a project serious problems encountered when projects directly administer credit programmes • Existing financial networks Using formal financial institutions as a channel for distribution of direct credit to poor rural populations is not always promising • Support for self-sufficient sustainable MFIs: a long term effort • Support for national rural finance systems through: • macro-economic stability • a regulatory and political environment that provides incentive for MFIs • Efficient Partnership among Government, MFIs/MFAs, funding agencies…

Future Challenges: Filling The Gap, Developing the Market, Serving the Rural Poor • Economically active populations & viable zones • Forms of Support • Dispersed, marginal populations • Urban population • Cash crop zone population • Untapped market • Non-viable market Co-operative banks and specialized lending institutions • 20%-30% • 20% • 30-40% Extended micro-finance services Other appropriate forms of support • 10-20%

The Rural Finance Strategy • To increase viability and outreach of rural finance • To strengthen implementation capacity at all levels for more effective rural finance interventions • To improve MFI monitoring & reporting and impact assessment of rural finance interventions

Operationalising the Strategy • How to support quality rural financial institutions to reach the rural poor? • How to build a conducive regulatory environment? • How to meet the unmet needs (agriculture, poorest people…)? 1. Increase outreach and viability of rural finance 2. Strengthen Implementation capacity for more effective rural finance interventions • How to further develop capacities at all levels? • How to improve program implementation? 3. Improve M&E & Impact Assessment • What is the Role of M&E in terms of increasing efficiency, learning, and policy dialogue ?