Download

1 / 81

810 likes | 827 Views

This framework defines the concept of independence and outlines threats and safeguards for public interest entities. It also covers network firms, related entities, and considerations for those charged with governance.

E N D

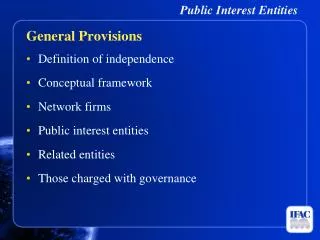

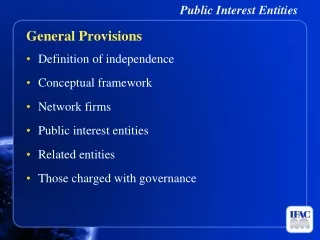

Public Interest Entities General Provisions • Definition of independence • Conceptual framework • Network firms • Public interest entities • Related entities • Those charged with governance

Public Interest Entities General Provisions – cont’d • Documentation • Engagement period • Mergers and acquisitions • Otherconsiderations

Public Interest Entities Definition of Independence • Independence of Mind • The state of mind that permits the expression of a conclusion without being affected by influences that compromise professional judgment, thereby allowing an individual to act with integrity and exercise objectivity and professional skepticism. • Independence in Appearance • The avoidance of facts and circumstances that are so significant that a reasonable and informed third party would be likely to conclude, weighing all the specific facts and circumstances, that a firm’s, of a member of the audit team’s, integrity, objectivity or professional skepticism has been compromised.

Public Interest Entities Conceptual Framework Approach – Threats and Safeguards

Public Interest Entities Conceptual Framework – Threats • Self-interest • The threat that a financial or other interest will inappropriate influence the professional accountant’s judgment or behavior. • Self-review • The threat that a professional accountant will not appropriately evaluate the results of a previous judgment made or service performed on which the accountant will rely when forming a judgment as part of providing the current service. • Advocacy • The threat that a professional accountant will promote a client’s position to the point that the accountant’s objectivity is compromised.

Public Interest Entities Conceptual Framework – Threats • Familiarity • The threat that due to a long or close relationship with a client, a professional accountant will be too sympathetic to their interests or too accepting of their work. • Intimidation • The threat that a professional accountant will be deterred from acting objectively because of actual or perceived pressures, including attempts to exercise undue influence over the accountant.

Public Interest Entities Conceptual Framework – Safeguards • Safeguards fall into two broad categories: • Those created by the profession, legislation or regulation; and • Those in the work environment.

Public Interest Entities Conceptual Framework – Prohibitions When safeguards are never adequate

Public Interest Entities Network Firms • Network firms are required to be independent of audit clients of other firms within the network • Network is defined as a larger structure that is: • Aimed at co-operation; and • Clearly aimed at profit or cost sharing or shares common ownership, control or management, common quality control policies and procedures, common business strategy, the use of a common brand-name, or a significant part of professional resources.

Public Interest Entities Public Interest Entities • Public interest entities defined as: • Listed entities; and • Entities • defined by regulation or legislation as a public interest entity, or • for which the audit is required by regulation or legislation to be conducted in compliance with the same independence requirements that apply to the audit of listed entities.

Public Interest Entities Public Interest Entities • Firms and member bodies are encouraged to determine whether to treat other entities as public interest entities because the entities have a large number and wide range of stakeholders • Factors to be considered include: • The nature of the business, such as the holding of assets in a fiduciary capacity for a large number of stakeholders; • Size; and • Number of employees.

Public Interest Entities Related Entities • Related entities of the audit client are defined as: • An entity that has direct or indirect control over the client if the client is material to such entity; • An entity with a direct financial interest in the client if that entity has significant influence over the client and the interest in the client is material to such entity; • An entity over which the client has direct or indirect control; • An entity in which the client, or an entity over which the client has direct or indirect control, has a direct financial interest that gives it significant influence over such entity and the interest is material to the client and its related entity; and • An entity which is under common control with the client (a “sister entity”) if the sister entity and the client are both material to the entity that controls both the client and the sister entity.

Public Interest Entities Related Entities • Listed entities • References to “audit client” include its related entities • Independence is required from all related entities. • Non-listed entities • Independence is required from related entities over which the audit client has direct or indirect control. • When the audit team knows, or has reason to believe, a relationship or circumstance involving a related entity is relevant to the evaluation of the firm’s independence, that related entity shall be included in the evaluation of independence.

Public Interest Entities Those Charged with Governance • Regular communication with those charged with governance is encouraged. • Communication enables those charged with governance to: • Consider the firm’s judgments in identifying and evaluating threats to independence, • Consider the appropriateness of safeguards applied, and • Take appropriate action.

Public Interest Entities Documentation • The professional accountant shall document conclusions regarding compliance with independence requirements and the substance of relevant discussions supporting conclusions: • When safeguards are required, the nature of the threat and safeguards in place or applied to reduce threat to an acceptable level shall be documented. • When a threat required significant analysis to determine whether safeguards were necessary and the accountant concluded safeguards were not necessary because the threat was already at an acceptable level, the nature of the threat and rationale for the conclusion shall be documented.

Public Interest Entities Engagement Period Independence is required during the engagement period and the period covered by the financial statements. The engagement period starts when the audit team begins to perform audit services and ends when the audit report is issued. If the engagement is recurring, the period ends at the later of the notification by either party that the professional relationship has terminated or the issuance of the final report.

Public Interest Entities Mergers and Acquisitions • When, as a result of merger or acquisition, an entity becomes a related entity of the audit client, the firm shall: • Identify and evaluate previous and current relationships that could affect independence, and • Take steps necessary by the effective date of the merger or acquisition to terminate any current interests or relationships that are not permitted.

Public Interest Entities Mergers and Acquisitions • If the firm cannot reasonably terminate an interest or relationship by the effective date, the firm shall: • Evaluate the significance of the threat, and • Discuss the matter with those charged with governance and if those charged with governance request the firm to continue as auditor, the firm shall do so only if: • The interest or relationship will be terminated as soon as reasonably possible and in all cases within six months of the effective date; • Any individual with such an interest or relationship is not a member of the engagement team or the individual responsible for the engagement quality control review; and • Appropriate transitional measures are applied and discussed with those charged with governance.

Public Interest Entities Mergers and Acquisitions • When the firm has completed a significant amount of audit work before the effective date of the merger or acquisition and can complete the audit in a short period of time, and those charged with governance request the firm to complete the audit while continuing with an interest or relationship that would otherwise be prohibited, the firm shall do so only if : • The firm has evaluated the significance of the threats and discussed such evaluation with those charged with governance; • The individual with such an interest or relationship is not a member of the engagement team or the individual responsible for the engagement quality control review; • Appropriate transitional measures are applied; and • The firm ceases to be the auditor no later than the issuance of the audit report.

Public Interest Entities Mergers and Acquisitions • In all cases, the firm shall determine whether, even if all the requirements can be met, the interests or relationships create threats that would remain so significant that objectivity would be compromised . • The firm shall document any prohibited interests or relationships that will not be terminated by the effective date of the merger or acquisition, including the: • Reasons why the interest or relationship was not terminated; • Transitional measures applied; • Results of the discussion with those charged with governance; and • Rationale as to why the threats that remain are not so significant that objectivity would be compromised.

Public Interest Entities Other Considerations • An inadvertent violation of an independence requirement generally will be deemed not to compromise independence provided: • The firm has appropriate quality control policies and procedures (equivalent to ISCQ 1) in place to maintain independence; and • Once discovered, the violation is corrected promptly and any necessary safeguards are applied to eliminate any threat or reduce it to an acceptable level. • The firm shall determine whether to discuss the matter with those charged with governance.

Public Interest Entities Key Independence Provisions General Provision Financial interests Loans and guarantees Business relationship Family and personal relationships Employments with an audit client

Public Interest Entities Key Independence Provisions Temporary staff assignments Recent service with an audit client Serving as a director or officer Long association (including partner rotation) Provision of non-assurance services Fees

Public Interest Entities Key Independence Provisions • Compensation and evaluation policies • Gifts and hospitality • Actual of threatened litigation • Reports that include a restriction on use or distribution

Public Interest Entities General Provision • The slides that follow cover particular circumstances or relationships addressed in Section 290 of the Code. • However, Section 290 does not describe all of the circumstances or relationships that create or may create threats to independence. • The firm and members of the audit team shall evaluate the implications of similar, but different, circumstances and relationships and determine whether safeguards can be applied when necessary to eliminate the threats or reduce them to an acceptable level.

Public Interest Entities Financial Interests • A firm, a member of the audit team, or an immediate family member shall not have a direct financial interest or material indirect financial interest in the audit client.

Public Interest Entities Financial Interests Partners, and their immediate family members, shall not have a direct financial interest or material indirect financial interest in any audit client served by engagement partners located in the same office. Partners and managerial employees who provide non-audit services to an audit client, except those whose involvement is minimal, or their immediate family members, shall not have a direct financial interest or material indirect financial interest in such audit client.

Public Interest Entities Financial Interests– cont’d • Financial interests held by immediate family members of: • Partners in the office of the engagement partner, or • Partners or managerial employees who provide non-audit services to the audit client will not compromise independence if the interest is received as a result of the family member’s employment rights and safeguards are applied when necessary. • When the immediate family member has the right to dispose of the interest or, in the case of stock options, exercise the option, the interest shall be disposed of or forfeited as soon as practicable.

Public Interest Entities Financial Interests • Those prohibited from having a direct or material indirect financial interest in an audit client shall not hold such interest as trustee unless: • The trustee, or immediate family member, or the firm are not beneficiaries of the trust; • The interest in the audit client is not material to the trust; • The trust cannot exercise significant influence over the audit client; and • The trustee, or immediate family member, or the firm cannot significantly influence any investment decision involving a financial interest in the audit client.

Public Interest Entities Financial Interests A firm, a member of the audit team, or an immediate family member shall not have a financial interest in an entity that the audit client also has an interest in if the interest is material to any party and the audit client can exercise significant influence over the entity.

Public Interest Entities Financial Interests • If the firm, a partner or employee of the firm, or immediate family member, receives a financial interest that would not be permitted, for example by way of an inheritance, gift or as a result of a merger: • If received by the firm, a member of the audit team, or immediate family member, the interest shall be disposed of immediately, or if the interest is indirect, a sufficient amount shall be disposed of such that the remaining interest is immaterial • If received by an individual who is not a member of the audit team, or immediate family member, the interest shall be disposed of as soon as possible, or if the interest is indirect, a sufficient amount shall be disposed of such that the remaining interest is immaterial

Public Interest Entities Financial Interests • Threats may be created: • If a member of audit team knows a close family member, or other individuals ,such as professionals in the firm or close personal friends, holds a direct financial interest or material indirect financial interest in the audit client • A firm’s retirement benefit plan holds a direct financial interest or material indirect financial interest in an audit client • A firm, a member of the audit team, or immediate family member, has a financial interest in an entity and a director, officer or controlling owner of the audit client is also known to have a financial interest in that entity

Public Interest Entities Loans and Guarantees • Audit clients that are banks or similar institutions • A firm, a member of the audit team, or immediate family member, may not have a loan or guarantee of a loan provided it is made under normal lending procedures, terms and conditions. • If a loan to a firm is permitted under the above and is material to the audit client or the firm, it may be possible to apply safeguards to reduce the threat to an acceptable level. • Audit clients that are not banks or similar institutions • A firm, a member of the audit team, or immediate family member, may have a loan or guarantee of a loan unless it is immaterial to the firm or member of the audit team and the immediate family member, and the client.

Public Interest Entities Loans and Guarantees A firm, a member of the audit team, or an immediate family member, shall not make or guarantee a loan to an audit client unless the loan or guarantee is immaterial to both the firm or member of the audit team and the immediate family member, and the client.

Public Interest Entities Business Relationships A firm shall not have a business relationship with an audit client or its management unless any financial interest is immaterial and the business relationship is insignificant to the firm and the client or its management. If any financial interest from a business relationship between a member of the audit team and the audit client or its management is material or the relationship is significant to that member, the individual should be removed from the audit team. If the business relationship is between an immediate family member of a member of the audit team and the audit client or its managements, any threat shall be evaluated and safeguards applied when necessary.

Public Interest Entities Business Relationships • The purchase of goods and services from an audit client by the firm, or a member of the audit team or an immediate family member, does not generally create threats to independence if the transaction is in the normal course of business and at arm’s length. • If the nature or magnitude of the transactions is such that a self-interest threat is created, safeguards shall be applied when necessary.

Public Interest Entities Family and Personal Relationships • An individual who has an immediate family member in one of the following positions at an audit client, or who was in the position during any period covered by the engagement or financial statements, shall not be a member of the audit team: • A director or officer; or • An employee in a position to exert significant influence over the preparation of the accounting records or the financial statements.

Public Interest Entities Family and Personal Relationships • Threats to independence are created when a member of the audit team has an immediate family member who is an employee in a position to exert significant influence over the client’s financial position, financial performance or cash flows. • The significance of the threats shall be evaluated and safeguards applied when necessary.

Public Interest Entities Family and Personal Relationships – cont’d • Threats to independence are created when a member of the audit team has a close family member in one of the following positions at an audit client: • A director or officer; or • An employee in a position to exert significant influence over the preparation of the accounting records of the financial statements. • The significance of the threats shall be evaluated and safeguards applied when necessary.

Public Interest Entities Family and Personal Relationships • Threats to independence are created if a member of the audit team has a close relationship with other persons in one of the following positions at an audit client: • A director or officer; or • An employee in a position to exert significant influence over the preparation of the accounting records of the financial statements. • A member of the audit team who has such a relationship shall consult in accordance with firm policies and procedures. • The significance of the threats shall be evaluated and safeguards applied when necessary.

Public Interest Entities Employment with an Audit Client • A former member of audit team or partner of the firm shall not join an audit client as director or officer or an employee in a position to exert significant influence over the accounting records or financial statements unless: • The individual is not entitled to any benefits or payments from the firm, unless made in accordance with fixed pre-determined arrangements and any amount owed to the individual is not material to the firm; and • The individual does not continue to participate, or appear to participate, in the firm’s business or professional activities.

Public Interest Entities Employment with an Audit Client – cont’d • If no significant connection remains between the firm and the former member of the audit team or partner, the significance of the threats shall be evaluated and safeguards applied when necessary. • Firm policies and procedures shall require members of the audit team to notify the firm when entering employment negotiations with an audit client. Safeguards shall be applied when necessary.

Public Interest Entities Employment with an Audit Client– cont’d Independence is compromised if a key audit partner or the firm’s Senior or Managing Partner joins the audit client as a director or officer or an employee in a position to exert significant influence over the accounting records or financial statements unless a specified period has passed. An exception exists if a former key audit partner or the firm’s Senior or Managing Partner is in such a position as a result of a business combination, provided certain criteria are satisfied.

Public Interest Entities Employment with an Audit Client – cont’d • Key audit partners include the: • Engagement partner; • Individual responsible for the engagement quality control review; and • Other audit partners on the engagement team who make key decisions or judgments on significant matters with respect to the audit. • Specified period • In the case of key audit partners, the client has issued audited financial statements covering a period of not less than twelve months and the partner was not a member of the audit team with respect to the audit of those financial statements. • In the case of the former Senior or Managing Partner, twelve months have passed since the individual held that role.

Public Interest Entities Temporary Staff Assignments • Such assistance may be given only for a short period of time. • Firm personnel shall not: • Provide a non-assurance service that would not be permitted under section 290; or • Assume a management responsibility. • In all cases the audit client shall be responsible for directing and supervising the activities of the loaned staff. • The significance of any threats shall be evaluated and safeguards applied when necessary.

Public Interest Entities Serving as a Director or Officer • A partner or employee of the firm shall not serve as a director or officer of an audit client. • A partner or employee may serve as Company Secretary if: • The practice is specifically permitted under local laws and professional rules of practice; • Management makes all relevant decision; • The duties are routine and administrative; and • The significance of the threats are evaluated and safeguards applied when necessary.

Public Interest Entities Long Associationof Senior Personnel Using the same senior personnel on an audit engagement over a long period of time creates threats to independence, which should be evaluated and safeguards applied when necessary. Key audit partners shall rotate after seven years and shall not be a member of the engagement team or a key audit partner for the client for two years.

Public Interest Entities Long Association of Senior Personnel • Where continuity is especially important to audit quality, key audit partners may, in rare cases due to unforeseen circumstances outside of the firm’s control, be permitted one additional year as long as threats to independence can be eliminated or reduced to an acceptable level by applying safeguards. • The time served as a key audit partner is taken into account when the audit client becomes a public interest entity. • An additional year is permitted only when the individual has served as a key audit partner for six or more years when the audit client becomes a public interest entity.

Public Interest Entities Long Association of Senior Personnel – cont’d • During the two year “time out” period, the individual shall not: • Participate in the audit of the entity; • Provide quality control for the engagement; • Consult with the engagement team or the client regarding technical or industry-specific issues, transactions or events; or • Otherwise directly influence the outcome of the engagement.

Public Interest Entities Long Association of Senior Personnel • Rotation is not required if: • The firm has only a few people with the necessary knowledge and experience to serve as a key audit partner; • An independent regulator has provided an exemption from rotation in such circumstances; • The independent regulator has specified alternative safeguards; and • The alternative safeguards are applied.