Download

1 / 15

150 likes | 323 Views

The Enron Fallout Implications for Canada. Submission to AcSOC, May 3, 2002 Financial Executives International Canada Presented by Michael Murphy, Vice President and CFO. Enron - Front Line Failure. Simultaneous failure of management, Board and audit safeguards:

E N D

The Enron Fallout Implications for Canada Submission to AcSOC, May 3, 2002 Financial Executives International Canada Presented by Michael Murphy, Vice President and CFO .

Enron - Front Line Failure • Simultaneous failure of management, Board and audit safeguards: • Senior managers who were greedy, unscrupulous and unethical • Board that was unwilling or unable to reign in the senior management team • External auditors who were not prepared to stand up to the client or walk away

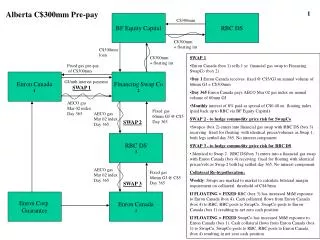

Enron - What Actually Happened? • Bad investments in “new economy” ventures • Off-balance-sheet entities created to hide losses and conceal extent of indebtedness • Many off-balance-sheet loans collateralized by Enron stock • “Form over substance” reporting

Enron - What Actually Happened? (continued) • Self –dealing by CFO and members of finance team • Corporate ego overwhelmed inadequate and ineffective control systems • Restatements, corrections and new disclosures • Ultimately a collapse of confidence in financial reports and integrity of management

Obvious Problems (in Retrospect) • Arrogant corporate culture • Docile almost somnambulant Board • Finance and accounting staff largely recruited from Andersen – independence compromised • Deceptive reporting posture with analysts, opaque reporting posture with investors

Enron Fallout:Lots of Questions • Are existing disclosure rules adequate? • How was the ethical conduct of an entire senior management team so totally compromised • Where were the inside and outside auditors? • Where was the Board and the audit committee?

Enron Fallout:Some Potential Answers • Ethical conduct • Effective Board oversight • Greater financial expertise on audit committee • Enhanced auditor independence and quality control

Enron Fallout:Some Potential Answers (continued) • More transparent and informative financial reporting • Emphasis on substance over form when applying accounting standards • A more nationally integrated securities regulation regime in Canada

FEI Canada’s Major Recommendations • Strengthen financial management and commitment to ethical conduct • Restore confidence in financial reporting and effectiveness of auditing process • Improve corporate governance and effectiveness of Board and Audit Committee • Validate Canadian process of financial reporting and standard setting

#1 Financial Management and Ethics • Adherence to code of ethical conduct • Promotion of ethical standards and effective “whistle blower” procedures • Monitoring of these initiatives should reside at Board level

#2 Financial Reporting and Audit Process • Create independent oversight body for auditing firms • Audit Committee to monitor auditor independence by vetting all non-audit service contracting • Minimum 2 year blackout on firm recruiting from its auditor

#3 Corporate Governance • Support implementation of recommendations of the Joint Committee (November 2001) • Continuing professional education for Board and Audit Committee

#4 Standard Setting and Monitoring Initiatives • Review efficacy and timeliness of standard setting process • Slippery slope of standardization • Closer integration of security regulation across Canada

Other Possible Changes • Possible high-risk companies targeted for increased review • Forensic audits • Closer integration among Canadian securities commissions • Analyst and rating agency reform

The most dynamic and effective organization for Canada’s financial executives