Download

1 / 12

150 likes | 194 Views

The Balanced Scorecard. The Balanced Scorecard. Developed by Robert Kaplan and David Norton. Introduced in the early 1990s. Motivated in part by Wall Street’s focus on quarterly earnings. Widespread adoption (hundreds of companies). Financial Performance Measures.

E N D

The Balanced Scorecard • Developed by Robert Kaplan and David Norton. • Introduced in the early 1990s. • Motivated in part by Wall Street’s focus on quarterly earnings. • Widespread adoption (hundreds of companies).

Financial Performance Measures • Financial measures are lag indicators: they report on the outcomes of past actions. • Traditional financial measures fail to accurately value intangible assets such as: • Customer relationships • Innovative products and services • Operating processes • Human capital • Information technology systems • Organizational climate

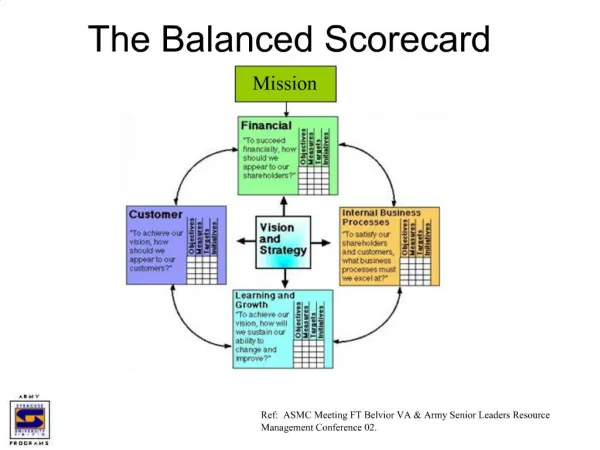

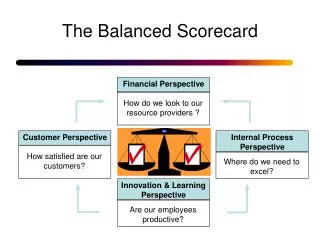

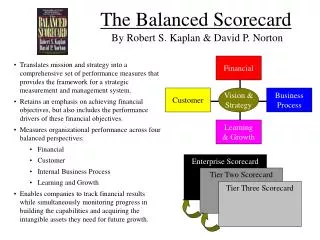

The Balanced Scorecard Identified Four Perspectives • Financial • Customer • Internal business processes • Learning and growth

The Balanced Scorecard Identified Four Perspectives • Financial • Increase shareholder value • Revenue growth • New markets, products, customers • Additional sales to existing customers • Productivity • Reduce direct and indirect expenses • Utilize assets more efficiently

The Balanced Scorecard Identified Four Perspectives • Customer • Operational excellence • Starbucks • Customer intimacy • Exceptional service • Custom products and solutions • Product leadership • Apple

The Balanced Scorecard Identified Four Perspectives • Internal business processes • Build the franchise (innovation processes) • Increase customer value (customer management processes) • Operational excellence (operations and logistics) • Good corporate citizenship (regulatory and environmental processes)

The Balanced Scorecard Identified Four Perspectives • Learning and growth • Employee capabilities and skills • Technology • Organizational climate

Balanced Scorecard “look-alikes” • Stakeholder scorecards • Shareholders • Customers • Employees • Key performance indicator scorecards • a.k.a.: KPI scorecards • A checklist approach • The Difference: Performance Measurement versus Strategic Management

The Balanced Scorecard • Step 1: Review the organization’s mission statement. • Why does the organization exist? • What are the organization’s core values? • Step 2: Develop a strategic vision. • What does the organization want to become? • Identify a clear picture of the organization’s overall goal.

The Balanced Scorecard • Step 3: Translate the strategy into operational terms. • Step 4: Align the organization to the strategy. • Align across business units • Align across staff functions • Align with outside stakeholders (suppliers, customers, etc.)

The Balanced Scorecard • Step 5: Make strategy everyone’s everyday job. • Communication and education • Incentive compensation • Step 6: Make strategy a continual process. • Link strategy to the budgeting process • Step 7: Mobilize leadership for change.