Download

1 / 25

250 likes | 389 Views

Forest Offsets in the Regional Greenhouse Gas Initiative. Carbon Finance 2009: Developing a Forest Carbon Market in the U.S. - A Look at the Regional Greenhouse Gas Initiative Center for Business and the Environment at Yale New Haven, CT November 5 th , 2008 Ellen Hawes

E N D

Forest Offsets in the Regional Greenhouse Gas Initiative Carbon Finance 2009: Developing a Forest Carbon Market in the U.S. - A Look at the Regional Greenhouse Gas Initiative Center for Business and the Environment at Yale New Haven, CT November 5th, 2008 Ellen Hawes Policy Analyst - Forestry

Environment Northeast • Environmental Policy, Research, and Advocacy • Offices in Maine, Massachusetts, Rhode Island, Connecticut and Prince Edward’s Island • RGGI Stakeholder • Program Areas • Energy Policy • Climate Change Solutions • Diesel Pollution • Forests and Bioenergy Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Presentation Outline • RGGI Overview • RGGI Structure • Cap Level • Offsets • What is being done to change this framework with respect to forest based offsets? Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Regional Greenhouse Gas Initiative • 10 States involved in RGGI • ME, MA, NH, VT, RI, CT, NY, NJ, DE and MD • First regional mandatory cap-and-trade program for carbon dioxide in the US • Applies to all fossil fuel-fired electricity generating units with nameplate capacity of 25 MW or greater Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Status of RGGI Implementation • Regulations complete in 10 states (with some issues to resolve in NJ) • Program commences Jan 1, 2009 • The 1st auction occurred Sept. 25th, 2008 • Details on the use of auction revenues are still being discussed in several states Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI State Plans for Implementation October 29, 2008 Regional Greenhouse Gas Initiative Summary/Status of States’ Plans for Implementation October 29, 2008 State Allocation Regulations Dec. % to be Proceeds Earmarked Net Program Auctioned for EE Funding for EE CT 10,695,036 Complete Yes 77% 69.5% 53.5% up to $5.002 DE 7,559,787 Complete Yes 60% up to 65% 39% in 2009, increasing to 65% in 2014 (increasing to 100% by 2014) ME 5,984,902 Complete Yes 100% up to 88% up to 88% up to $5.002 MD 37,503,983 Complete Yes 85% 46% 39% MA 26,660,204 Complete Yes 98% not less than 80% not less than 78.4% NH 8,620,460 Complete Yes at least 71% through 2011 , up to 90% up to 63% through 2011, at least 83% thereafter up to 75% thereafter NJ 22,892,730 Pending Yes Up to 99% up to 80% up to 80% (with $2 allowances set aside for CHP and direct allocation to co-generation) NY 64,310,805 Complete Yes 97% up to 100%* up to 97%* RI 2,659,239 Complete Yes 99% 95% less $550,000 up to 94% less $550,000 VT 1,225,830 Complete Yes 99% 100% 99% Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Two-Phase Cap • Two-phase cap: • Stabilization at “current” levels for 2009-2014. • State budgets are reduced 2.5% per year 2015-2018 for a total reduction of 10% • The initial regional cap is set at 188 million tons CO2 for the 10 states • Each state has an allocation of the total cap to sell, but the regional cap is the most important as RGGI is a regional market with trading Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Use of Auction Proceeds in RGGI – Energy Efficiency First IPM Forecasts of Wholesale Electric Power Prices Changes Reference Case vs. RGGI Policy Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI Auction • 1st Auction 9/25/2008 • Sealed Bid, Uniform • 12,565,387 allowances sold • 2009 vintage only • CT, ME, MD, MA, RI, VT • Allowances sold for $3.07 a ton • Next Auction 12/17/2008 • 31,505,898 tons offered • All ten states participating Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI Trading • 2009 RGGI contracts trading ~ $4.15 on the secondary market (10/31/08) • Chicago Climate Exchange’s CFI’s ↓, while RGGI allowances ↑ • RGGI allowances are part of a mandatory regulatory regime and may have a greater chance of being fungible under a federal cap-and-trade system [Point Carbon - Carbon Market North America Vol 3 • Issue 22• 31 October 2008] Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI and Offsets • Offsets from other sectors can be used to cover 3.3% of a RGGI unit’s compliance obligation. • Offsets must be real, additional, permanent, quantifiable, enforceable • Standards approach ––uses predefined protocols for determining eligibility • Example: Afforestation – all land non-forested for past 10 years eligible – does not require project-specific analysis of additionality • Initial geographic location: 1) within the RGGI states, 2) states with a comparable cap & trade program, 3) states that sign an Offsets Memorandum of Understanding • “Offset Triggers” at $7 per ton/allowance (increase offset to 5%) • “Safety Value” at $10 (increase offsets to 10%, expands geographic scope, 4 yr compliance period) Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI Offsets • Initial offset categories: • Landfill methane capture & combustion • Sulfur hexafluoride (SF6) capture & recycling at electricity transmission facilities • Sequestration though afforestation (tree planting) • End-use fossil fuel (natural gas, propane, and heating oil) energy efficiency • Methane capture from agricultural operations Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Offset Requirements: Five point test – “R.S.V.P.(E)” • Real: able to quantify an actual and measurable reduction in emissions. • Surplus (additional): additional or surplus to reductions in emissions that would occur under business as usual activities, above and beyond what would have occurred absent any funding for the offset project. • Verifiable: sufficient measurement and documentation to allow independent auditors to assess and confirm project eligibility and performance • Permanent: be lasting, ensuring that a reduction in emissions is not capable of being reversed at some future point in time. • Enforceable: able to enforce compliance or require a return of the offset credit if other requirements are not met. Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Proposal to Supplement Qualifying RGGI Offset Types • RGGI rules allow for supplementation of offset categories • Must meet Five Part Test • Maine Forest Service initiated lead with RGGI states to propose new additions to initially qualified RGGI offset types • Maine Forest Service working with Maine DEP, ENE and Manomet to develop project protocols for new forest offset types • Incorporating feedback from stakeholders Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

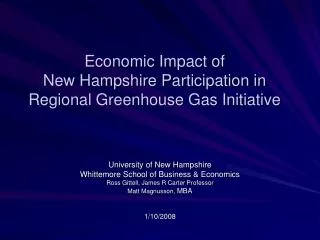

Proposal to Supplement Qualifying RGGI Offset Types: Forest Management • Forest Management • Baseline • Measure existing carbon stocks • Additionality • Credits depend on where you are compared to average stocking levels in the region • Permanence • Commit to maintain increased stocking for 99 years • Aggregators of small landowners may be able to have rolling enrollment. • Leakage • Timber management is required, pending leakage research • Either maintain average levels, or be certified by FSC, SFI, Tree Farm Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

A. If starting with carbon stocks below FIA meanfor region • B. If starting with carbon stocks above FIA mean forregion • carbon 100% for new carbon Starting carbon 100% credit for new carbon 75% for existing carbon FIA mean FIA mean 50% credit for new carbon Starting carbon • Figure 1. Recommended carbon credit for projects that start (A) below the FIA mean carbon stocking level for the forest type and region, and (B) above the FIA mean. Proposal to Supplement Qualifying RGGI Offset Types: Forest Management Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Data Stratification • What is the best way to calculate mean carbon levels per acre? • State boundaries, ecoregions, forest types • Balance between accuracy and variability Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Proposal to Supplement Qualifying RGGI Offset Types: RID and UCF • Reduced Impact Development • Reducing the amount of forest loss per housing unit by clustering development and protecting forested areas with easements • There may be only a few large developments where this would be attractive as an offset project • Urban and Community Forestry • Increasing inventory of street and park trees • Total carbon levels are small and would probably require significant additional funding Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Proposal to Supplement Qualifying Offset Types: Avoided Deforestation • Avoided deforestation • Our RGGI proposal initially included a category for forest conservation, credit based on likelihood of development threat • Based on further assessment and stakeholder feedback, we are no longer proposing this as a priority offset category Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Proposal to Supplement Qualifying Offset Types: Avoided Deforestation • Challenges • Leakage – how do you prove that you are not simply displacing demand for housing elsewhere • Timing and location of development threat – data on forest loss to development is very uneven, past trends may not accurately reflect future threats ►A non-offset approach may work better and result in a more certain income stream Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Alternative Approaches for Conservation • Programmatic Approach • Outside of cap • Funding Sources: • Auction Revenues (Lieberman-Warner) • Carbon Neutral Growth Fund • Real Estate Fund • Other tax incentives Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

RGGI Offset Market • Total RGGI market opportunity • 188 million allowances a year in first period • Maximum of 3.3% offsets • At $3/ton, maximum offsets market of $18.6 million a year • Forest offsets will have to compete with other offsets for a share of this market • If allowances are cheap, there will be less overall demand for offsets • Internationally, forestry and ag credits represent only 1% of traded offsets, mainly because they are not eligible in the EU market • Industrial projects dominate Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Example of Opportunity for Individual Landowner • 500 acres spruce-fir forest • Currently 30 tons CO2/acre over the FIA mean • Sell 30 tons/acre upfront, 75%, $3/ton • $33,750.00 upfront, with the possibility of receiving more money over time • In exchange for 99-yr. commitment and monitoring costs Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008

Ellen B. Hawes Policy Analyst – Forestry and Biofuels (207) 761-4566 ehawes@env-ne.org Environment Northeast Rockport, ME / Portland, ME / Boston, MA Providence, RI / Hartford, CT / New Haven, CT Charlottetown, PEI, Canada www.env-ne.org Contact Information Carbon Finance 2009 Speaker Series Center for Business and the Environment at Yale, Nov. 5th, 2008