Download

1 / 37

420 likes | 685 Views

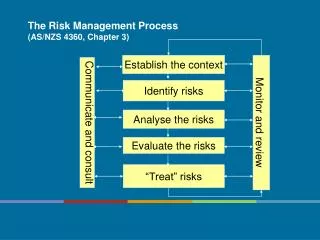

Chapter 2: The Risk Management Process. Objectives. Discuss the techniques used to identify and analyze loss exposures; Formulate options to deal with loss exposures using various methods available: Loss control; Loss financing; Loss financing transfer. Steps in the Risk Management Process.

E N D

Objectives • Discuss the techniques used to identify and analyze loss exposures; • Formulate options to deal with loss exposures using various methods available: • Loss control; • Loss financing; • Loss financing transfer.

Steps in the Risk Management Process The risk management process is used to minimize loss exposures. Steps in the Risk Management Process: • Identify and Analyze • Formulate Options • Select the Best Technique (or combination of techniques) • Implement the Plan • Monitor and Modify

Step 1: Exposure Identification and Analysis • To treat a loss exposure, it must first be identified. • Identifying loss exposures determines a client’s needs. • Using risk management techniques, a needs-based sales approach is achieved.

Methods of Exposure Identification • May involve risk manager, producer, risk inspectors and others. Teamwork produces the best results. • Both risk managers and insurance personnel may seek help from outside sources (Fire Department, Police, Lawyers, Consultants). • Commonly used methods of exposure identification: • S • F • F • I

Surveys • Checklists, survey forms and questionnaires are used to systematically search for exposures to loss. • Checklist describes subjects of insurance, highlights the perils and lists the types of insurance policies appropriate for the exposures identified. Elicits underwriting information. See Exhibit 2-1 • Contents schedule is a detailed survey form devoted to contents and legal liabilities flowing from such property. See Exhibit 2-2 • Software programs more sophisticated programs help to determine likelihood of loss and probably location. • Related survey forms – form used should be appropriate for the type of operation. Information collected must be relevant.

Flow Charts • Helps to identify exposures to loss. • Maps the sequence of business activity graphically • May be simple or complex. See Exhibit 2-3 • Reveals bottlenecks in production.

Flow Charts Moonshine Rust Remover Consumption Furniture Polish Packaging Bottling Shipping

Financial Statements • Financial statements help to identify loss exposures. • Balance sheet will show major categories of assets. • Must not be used to establish the anticipated cost of loss or insurable value. • Income statement provides information about other activities. • The clues found in financial statements must be probed to determine the full extent of loss exposures.

Inspections • No substitute for inspections – first hand information • Cost-conscious decisions must be made in every situation. Can be expensive especially if outsourcing or locations around the world. • Reserve for perceived greatest risks • Joint inspections can improve relationships. Experience is gained through observation and studying different business operations. • Everyone benefits by having standards for risks to reduce the possibility of insurance losses.

Analysis of Loss Exposures • Once exposures are identified, predictions are made on the likelihood and probable seriousness of potential losses. • Each loss exposure is analyzed considering the following: • Likelihood of the loss occurring (loss frequency); • Seriousness of the loss (loss severity); • Financial effect of all losses in any given period of time (frequency times severity); • Reliability of the predictions of frequency and severity.

Frequency and Severity • Past events, statistical data, recent judicial decisions and other trends affecting claims are studied to predict the likely frequency and severity of losses (experience lends to credibility). • Frequency and severity can be classified in non-mathematical terms using Prouty Measures developed by Richard Prouty. • Frequency – • Severity – See Pg. 12 for Prouty Measures • This method relies on judgment and common sense to estimate losses.

Statistical Probability • Statistics are used to evaluated risk and make predictions using sophisticated mathematical models (actuaries) • Predictions based on statistics are relevant only when the statistical base has sufficient numbers of exposures and losses. • Operation of Law of Large Numbers – credibility and true underlying probabilities improve as the statistical base grows. • If an event cannot occur it has a probability of %, if it is certain to occur the probability is %.

Statistical Probability • For the Law of Large numbers to work each exposure to loss must exist independently from the others (unlikely two or more units will be affected by a single occurrence). • The exposures must also be similar and share the same major characteristics. • Predict with as much certainty as possible what the probabilities are of future losses. • Predictions must consider changes. • Calculations based on the past can reliably predict the probabilities of future events only if everything else remains unchanged. • See Example Pg. 14 www.en.Wikipedia.org

Statistical Probability • It is possible to calculate average severity of loss for a given period and the probabilities for specific ranges of possibilities. • Catastrophic occurrences are difficult to predict simply because they happen so infrequently. Knowing the potential cost of losses helps when considering the financial impact these losses could have. • This aspect is a key factor in determining the risk financing method to be used. • Most risk management specialists believe that predictable high frequency, low severity loss exposures should be retained. “Cost of doing business” • Noninsurance techniques and deductibles can help free up premium dollars.

Step 2: Formulating Options to Deal with Exposures • The next step in the risk management process is to formulate the best technique or combination of techniques for dealing with each exposure. • There are two major categories used to classify these techniques: • Loss control techniques to control the exposure to prevent losses or reduce their severity. • Loss financing techniques to pay for losses which do occur.

Loss Control • Two basic approaches to loss control measures: • Domino Theory (H.W. Heinrich) – all losses are the result of unsafe acts of persons – accidents are the fault of people. • Unsafe acts begin the chain of events which ultimately lead to accidents. • Energy Release Theory (Dr. William Haddon, Jr.) – accidents result form mechanical failure. • These two approaches have been combined by many loss prevention experts.

Loss Control • In the past loss control was referred to as “engineering” and was limited in scope. • As risk management developed, the concept of loss control has expanded to include various techniques for treating losses. • Loss control techniques include: • A • L • L • S • N

Avoidance • Eliminating an exposure or by not assuming a new exposure one can avoid the risks associated with it – probability of loss is reduced to zero (no uncertainty). • Sometimes impractical or impossible to accomplish. • Avoidance seems to present a desirable technique but it is not often a viable technique. www.voiceofanxiety.com

Loss Prevention • Loss prevention is a frequently used risk management technique because it is so effective. • Examples: Driver training, … www.snipview.com

Loss Reduction • Loss reduction activities are used to lessen the severity of those losses which do occur. • Examples: Automatic sprinklers, burglar alarms, etc. • Does not alter the chance of a loss, but when one does occur it is expected to be less severe. • The total amount of loss can be reduced if damage is repaired promptly and the additional costs measured against down time are usually worth the expense.

Prevention and Reduction • Loss prevention and loss reduction measures cost money! • People resist implementing them due to cost – many implement to get insurance or a discount on insurance. • Consultants can help decide which measures can be economically implemented. Prioritize according to cost and effectiveness. • Examples: Automatic sprinklers, burglar alarms, fire extinguishers, lighting, etc. • Putting together a plan of action and a schedule for implementation can help this process.

Separation or Diversification • This may be difficult to implement due to cost • Items subject to loss can be moved to separate locations to reduce the concentration of value should a loss occur at one location. • Duplication is an economical method to separate a loss exposure and potentially save a great expense to recreate material or data. • Example:

Noninsurance Transfers • Loss control noninsurance transfers pass any financial responsibility for a loss to someone else. • The probability of loss remains the same, but the asset or activity from which the exposure to loss arises is transferred another party. • Solid rock must be removed – an independent blasting contractor is hired to perform the task.

Loss Financing • Two methods used to finance losses are: • Retention and; • Transfer www.bit.ly

Retention • Retention is absorbing all or part of the loss (sometimes the only risk management technique available) • Sometimes last resort or residual method. • War risks fall into this category because they are generally not insurable or transferrable. • Retain losses low in severity and high in frequency (each organization needs to determine these for themselves) • Active Decision is one made consciously – whether that is doing something or not. • Insurer’s often encourage insureds to choose higher deductibles – cost of doing business.

Retention • Passive retention is when an exposure is retained because it was never identified (not good). • Sources of funds to meet the costs of retained losses: • Current expenses; • Unfunded reserves; • Funded reserves; • Borrowing; • Capital insurers.

Retention • Current Expensing of Losses – losses can just be paid. Advantage of not requiring segregated funds or any borrowing, but you must have the money available (financing retained losses). • Unfunded Reserve – an account set up on the balance sheet allocating funds for retained losses. Shows a reserve for losses on it’s financial statements, but no cash or other asset would be earmarked. • Funded Reserve – more certain method of paying for losses. Money is actually on hand in an account designated to pay for such losses (requires discipline). “Opportunity cost”. • Borrowing – go to a lender. • Captive Insurer – establish a captive insurer to finance retained losses. Purpose is to fund losses. Usually owned entirely by a parent company.

Advantages and Disadvantages • Large organizations loss costs may be reduced when losses are retained. Retention is a method to gain control of the premium dollars and improve the companies cash flow. • Large organizations can retain higher levels of risk. • Retention levels are lower for average-sized companies. The purchase of insurance for these companies is an economical and practical way to deal with potentially crippling exposures. • When companies must pay for at least part of their own losses it encourages them to actively practice loss prevention

Advantages and Disadvantages • Large retention levels must be justified by adequate loss history and financial resources to pay for losses that do occur. • Retention is best practiced for smaller, predictable losses. • There are income tax considerations in selecting retention. • Retaining losses will mean the services often available with insurance protection will be lost. • Unbundled services– this is when organizations (usually large) pick and choose the services they purchase from an insurer. Helps to reduce premium costs and customize the services they need. ****SEE PG. 24 – Advantage and Disadvantages****

Loss Financing Transfer • Two methods used to transfer responsibility for paying losses. • Transfer of loss to other entities by business contract • Transfer of loss to insurer through an insurance policy.

Noninsurance Loss Financing • Contracts often include hold-harmless agreements and indemnification clauses to transfer the financial consequences of losses. • Any type of contract may include these provisions: • A lease of premises or equipment; • C • A bailment contract; • C • Purchase order agreements; • S www.icts.uiowa.edu

Noninsurance Loss Financing • In a contract for services, the party performing the work, the indemnitor, usually agrees to accept the financial responsibility of paying certain losses for the party who is receiving the benefit of the work, the indemnitee. • It is usually the more powerful party that will insist on transferring the exposure (Cities and Governments). • NOT a loss control measure - The asset or activity remains with the organization. Frequency or severity of loss is not affected – only financial responsibility is shifted to the other contracting party for specified future losses. • Varying degrees of responsibility may be transferred by contract. In some circumstances it is not legal to contract away responsibility for negligence.

Noninsurance Loss Financing • Read contracts CAREFULLY to identify clauses that transfer risk. • Be familiar with the types of contracts used in the industry and ensure the degree of responsibility accepted is reasonable. • If clauses in a contract make highly unreasonable demands they may be unenforceable. • When hold-harmless agreements and indemnity clauses are drafted, liability insurance should be part of the contract. • Loss transfer is a private agreement between the indemnitee and indemnitor– not binding on third party. Advantages and Disadvantages – See Pg. 27

Insurance • Insurance is a mechanism by which insureds exchange or transfer, the uncertainty of future losses for the certainty of a fixed sum – the premium. • Insurance deals exclusively with transfer of financial risk. • Insurers set premiums as follows Premiums = + components for profit + + other contingencies.

Insurance • Selecting an agent or broker and insurer should be done carefully. • Considerations regarding: • The financial strength of the insurer • The willingness of the insurer to provided required coverage. • The range of additional services offered • The cost of coverage. • The producer who is dedicated to risk management principles can navigate the conflict of interest caused by insurance commissions. • Fee-for-service to avoid any conflicts may be offered.