Download

1 / 19

200 likes | 420 Views

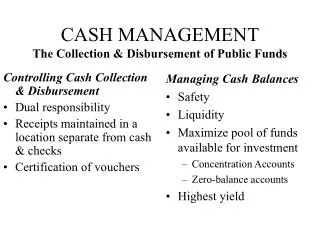

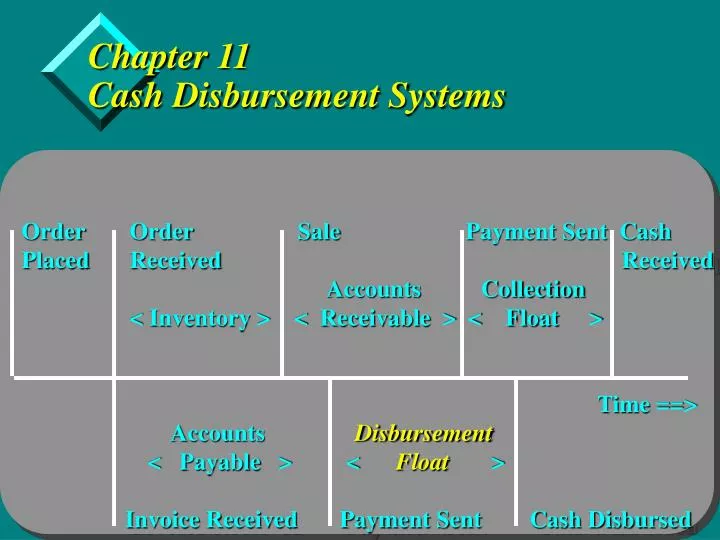

Chapter 11 Cash Disbursement Systems. Order Order Sale Payment Sent Cash Placed Received Received Accounts Collection

E N D

Chapter 11Cash Disbursement Systems • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

Learning Objectives • Identify the environmental variables influencing disbursement decisions. • Identify the major disbursement mechanisms, relevant institutional aspects, and major implementation variations. • Specify the major funding alternatives for disbursement accounts. • Conduct valuation of payment mechanism decisions. • State the contribution of and steps involved in disbursement location model applications.

Disbursement Policy: 4 Principles • Maximize value through payment timing • Optimize the accuracy and timeliness of information • Minimize balances in disbursement accounts • Prevent fraud

Cash Disbursements and the Cash Flow Timeline • Payment system • Changing rapidly due to technological innovation and interstate banking. • Ethics and organizational policies • See chart on p. 375 • Decentralized v.s. centralized disbursements • Generally, smaller, local companies use a centralized system • Organizational structure • Overlap of authority may result in inefficiencies and increased costs

Cash Disbursements and the Cash Flow Timeline - continued • Banking system • A change in the choice of bank may have the greatest impact on costs. • Treasury information system • Companies are more highly automated in payables than any other area. Systems are expensive, but may result in substantial savings. • Cash flow characteristics • Companies with predictable cash flows do not need to invest in cash management systems

Cash Flow Timeline Disbursement Float Mail Processing Clearing Float Float Float Availability Slippage Float Bank debits payor’s accnt Payee receives good funds Payee deposits check at bank Payee receives check Payor puts check in the mail

Organizational Structure • Functional areas impacting disbursements • Treasury department • Accounts payable department • Production • Purchasing department • Personnel department

Simple Systems • Manual and paper-based • Demand deposit accounts • Payroll services • Drafts • Account reconciliation

Complex Systems • Paper-based systems • Account funding • Electronic disbursing systems • Electronic data interchange

Complex Systems • Paper-based systems • Multiple-drawee checks (more than one bank listed on face) • Drawback is large number of checks (increased costs) • Overcome with Purchase Order with Payment Voucher Attached. Voucher may be deposited after goods are shipped, and act like a draft on the disbursing company’s account. • Disbursement account is funded either through a controlled disbursement account or a zero balance account

Complex Systems – continued • Controlled disbursement account • Special case of zero balance account • Bank notifies firm of that days presentments early in the morning • Bank will not pay presentments after a set time, usually 8:00 A.M. • Firm will transfer only enough funds to cover that days presentments

Complex Systems – continued • Zero Balance Accounts • Requires no notification of days presentments • Bank automatically drafts concentration account for that days presentments • Pseudo-ZBA: Maintains average daily disbursements • May require company to maintain a Money Market account and/or credit line at bank

Complex Systems – continued • Electronic disbursing systems • Most common is payroll deposit • Disbursement bank is provided with necessary data and funds are transferred via ACH • Electronic data interchange • Comprehensive system whereby all information related to a purchase is transmitted electronically

Disbursement System Trends • Comprehensive payables • Payables are subcontracted usually to a bank • Purchasing cards • Eliminates a multitude of checks • Payables security/fraud prevention • Positive pay: firm sends daily check issue file to disbursement bank, bank checks file before paying • Reverse positive pay: bank sends daily presentment file to firm, firm checks file before authorizing payment • Use of Internet for ordering and payment • Less expensive than EDI

Global Disbursing Systems • System differences • Business interest-bearing checking accounts with overdraft protection • Disbursement float increased due to currency differences and geographic location (no central settlement bank) • Postal system clearing and value dating • International disbursing risks • Country (Political) and exchange risk • Intra-company payments • Bilateral and Multilateral netting systems • Reinvoicing Centers – Major advantage is centralized foreign exchange exposure

Optimizing the System Four major decisions • Selecting the optimal disbursing mechanism • Establishing a disbursement network • Selection of the disbursement bank(s) • Selection of the funding mechanism(s) for the disbursing accounts

Selecting the optimal disbursing mechanism • Paper vs. electrons • Choose lesser of two • Where: A =Average payment amount cE = clearing period for electrons cC = clearing period for checks nE = credit period for electrons nC = credit period for checks

A Model for Selecting Bank(s) and Location(s) Based on the Lockbox Cost Function • Max:Net Profit = N [(F x D x i) - VC] - FCwhere: • N = number of checks • F = Average Face Value • D = number of days to clear check • i = Daily Opportunity Rate • VC = Per Item Processing Cost • FC = Fixed Cost

Summary • Objective of a disbursement system: pay with the right method, at the right time, in an efficient manner. • Disbursement systems are simple and complex. • Simple systems tend to be paper based and use basic funding mechanisms. • Complex or sophisticated systems are prone to use electronic payments, controlled disbursement accounts and ZBAs with electronic funding of the accounts. • Disbursement systems should be well coordinated with cash collection and cash concentration systems.