Download

1 / 18

190 likes | 351 Views

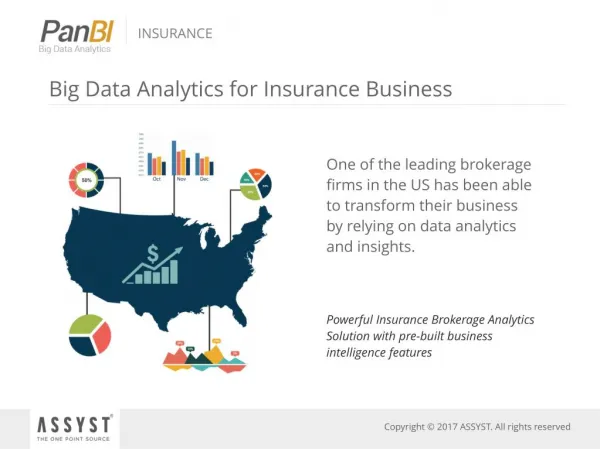

PERCEPTIONS AND MISCONCEPTIONS BIG DATA IN INSURANCE. APRIL 2013. Craig Beattie and Nicolas Michellod Senior Insurance Analysts. General observations. A recording of this presentation will be available for download to subscribers of Celent’s Insurance services at www.celent.com

E N D

PERCEPTIONS AND MISCONCEPTIONS BIG DATA IN INSURANCE APRIL 2013 Craig Beattie and Nicolas Michellod Senior Insurance Analysts

General observations • A recording of this presentation will be available for download to subscribers of Celent’s Insurance services at www.celent.com • In addition to this presentation, Celent suggest the following reading • Perceptions and Misconceptions of Big Data in Insurance, April 2013 • How Big Is Big Data?: Big Data Usage and Attitudes Among North American Financial Services Firms, April 2013 • Big Data: A Guide to Where You Should Be, Even If You Don’t Know Where You Are, February 2013 • Big Insurance Data: Drawing Lessons from Amazon, Google, and Facebook, December 2011 • You can obtain more information about subscribing from Chris Williams: cwilliams@celent.com • For questions about the content please contact: Craig Beattie cbeattie@celent.comor Nicolas Michellod nmichellod@celent.com

Webinar contents • Survey participants • Data challenges in Insurance • Current Big Data adoption • Investment in data-related technologies • Applying the Celent Big Data Adoption Maturity Model to Insurers

Survey participantsSurvey launched in February 2013 Survey participants by size and geography of insurance companies (n=276) Title and functions of in proportion of respondents (n=276) 42% of insurers active in the property & casualty line of business 24% in the lifebusiness The remaining 34% work for composite insurance firms (offering both life and property casualty products) Source: Celent survey

Data challenges in InsuranceRanking the “V” challenges The “V” challenges In your organization, please rank the following challenges in relation with data by level of difficulty? (In % of respondents; n=225) Velocity and Variety of data are the most important challenges Volume, Value and Veracity of data are less problematic Source: Celent

Current Big Data adoptionThe Celent Big Data Adoption Maturity Model MATURITY SCIENTIST INNOVATOR PRACTITIONER EXPERIMENTER SPECTATOR ACTIVITIES Focused on business priorities and only watching Big Data projects Investing in a few pilot Big Data projects Implemented tools in production but focused on pilot programs rather than broad Big Data solutions Building tools and using open source code. Approach is based on established methods Developing new algorithms, dealing with the most complex data sets PEOPLE Traditional data skill sets Curious staff, computer scientists, and data analysts Like experimenters plus experienced, business-oriented professionals and technology partners Adding a mix of advanced degree mathematicians, computer scientists, and statisticians Advanced degrees are common here, along with plenty of PhDs TOOLS Excel, simple dashboards, standard reports Free trial software and open source tools, vendor-supported pilot projects Licensed software and open source tools, vendor-supported installations Pragmatic approach to building, configuring, customizing, or buying Proprietary software, open source extensions, etc. improve existing and develop new solutions ATTITUDE TO DATA Data across the industry is mature, and data models are well established and defined Analysis of data can provide insights into internal operations and small improvements New data occasionally allows new approaches and even entrants to the market New approaches to data lead to new startups, radical changes and great benefit for first mover Actively looking for new data sources and ways of using data to help drive revenue and profit growth BENEFIT OF DATA Data is a commodity across the industry and of little intrinsic value Occasional insights Data helps the business to operate better and improve efficiency Collection, use, and productization of data is key to success Data and firms’ use of data are crucial to differentiating POSITION OF COMPETITORS The technology is untried and untested, and the business case is uncertain Firms have been slow to adopt these technologies but they are trying to better understand them Competitors are leveraging this technology to achieve demonstrable cost savings Competitors have adopted this technology and are seeking industry awards for its novel use Competitors are delivering new unique solutions and seeking ways to protect their investment CUSTOMER EXPECTATIONS The same old products, services, and offerings that they are used to Clients expect good, solid products and offerings and are pushing insurers to meet their demands Good service at a reasonable cost. Offerings that are at pace with if not ahead of competitors Market leading, offering value for money but also novel solutions Innovative use of new data sources to its own benefit and that of its customers Source: Celent

Current Big Data adoptionPeople and tools to look at data (1) Which of the following best describes the teams currently looking at data in your organization and which sort of tools are they using? (Multiple answers possible) (n=218) Which of the following best describes the teams currently looking at data in your organization and which sort of tools are they using? (team only view) (Multiple answers possible) (n=218) Source: Celent survey

Current Big Data adoptionPeople and tools to look at data (2) Which of the following best describes the teams currently looking at data in your organization and which sort of tools are they using? (tools view) (Multiple answers possible) (n=218) The use of proprietary tools is almost as popular as Excel as a type of tool utilized Use of open source tools and proprietary extensions is higher than one might expect in the insurance industry Source: Celent survey

Current Big Data adoptionAttitude to and benefits of data In your opinion, how important will the following sources of data be in the insurance industry in the near future (2–3 years)? (In % of respondents; n=202) How would you prefer to integrate to open data sources? (n=195) Source: Celent survey

Current Big Data adoptionPerceived position of competitors What best summarizes your view of the adoption of big data technologies in your industry and by your competitors on the market? (In % of respondents; n=200) More than half of them think the sector has been slow to adopt Big Data technologies and is still trying to better understand these technologies An additional 16% of respondents feel the technology is untried, untested and therefore the business case remains uncertain Only less than one insurer over five thinks their competitors are already leveraging Big Data to make demonstrable savings Only 8% feel that competitors were delivering new solutions and propositions to the market Source: Celent survey

Current Big Data adoptionPerceived customer’s expectations In terms of customer expectations as a result of big data initiatives, what statements best describe your opinion? (In % of respondents; multiple answers possible; n=199) • Half of insurers considers customers to be relatively traditional and basing their choice on the quality of the insurance product proposed and the perceived quality of the related services and tariffs • Less than a third of respondents think customers’ expectations have changed • A bit less than 6% of insurers think they are perceived by customers as a leading industry in their use of data, novel use of new data sources and in their ability to leverage that to their own benefit and that of their customers Source: Celent survey

Investment in data-related technologiesCurrent situation What is your current situation with regard to investment in these technologies? (in % of respondents; n=178) Insurers leverage data analysis technologies to improve their business basics Big Data-related technologies are still unknown for many insurers Growing interest in cloud based analytics Source: Celent survey

Investment in Data-Related technologiesInvestment in Big Data and priorities If you have invested or plan to invest in Big Data capabilities, how do you want to do this investment? (in % of respondents and with multiple answers possible; n=151) What would be the top 5 priority analysis to do using Big Data infrastructure (rank by priority)? (Number of respondents; n=171) Source: Celent survey

Applying the Celent Big Data Adoption Maturity Model to InsurersCurrent versus desired situation MATURITY = where insurers are today SCIENTIST INNOVATOR = where insurers should be PRACTITIONER EXPERIMENTER SPECTATOR ACTIVITIES PEOPLE TOOLS ATTITUDE TO DATA BENEFIT OF DATA POSITION OF COMPETITORS CUSTOMER EXPECTATIONS

Applying the Celent Big Data Adoption Maturity Model to InsurersFilling in the gaps To fill in the gaps • Don’t believe competitors are laggards • The insurance industry is set for a step change in customer engagement • Treat data as a critical raw material If you are planning or have already invested in Big Data capabilities, could you rank by order of priority what you consider to be the building blocks for success? (In % of respondents; n=151) Priority 1 Priority 2 Priority 3 Priority 4 Source: Celent survey

General observations • A recording of this presentation will be available for download to subscribers of Celent’s Insurance services at www.celent.com • In addition to this presentation, Celent suggest the following reading • Perceptions and Misconceptions of Big Data in Insurance, April 2013 • How Big Is Big Data?: Big Data Usage and Attitudes Among North American Financial Services Firms, April 2013 • Big Data: A Guide to Where You Should Be, Even If You Don’t Know Where You Are, February 2013 • Big Insurance Data: Drawing Lessons from Amazon, Google, and Facebook, December 2011 • You can obtain more information about subscribing from Chris Williams: cwilliams@celent.com • For questions about the content please contact: Craig Beattie cbeattie@celent.comor Nicolas Michellod nmichellod@celent.com