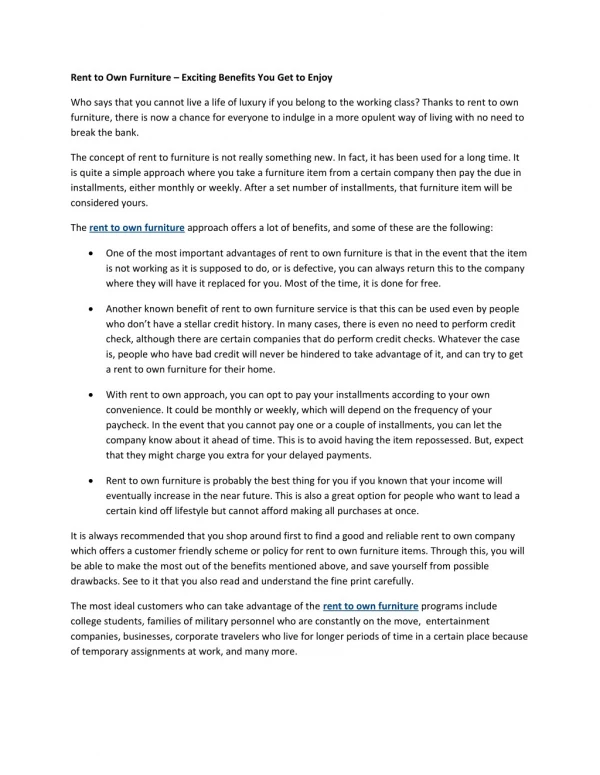

Download

1 / 13

140 likes | 336 Views

Rent to Own Auto Turn-Key Program. Presented by Arceri & Associates, Inc. PRINCIPAL RTO ADVANTAGE. Increased CASH FLOW! No UPFRONT sales tax in most states RTO down payment can be a security deposit eliminating income tax

E N D

Rent to Own Auto Turn-Key Program Presented by Arceri & Associates, Inc

PRINCIPAL RTO ADVANTAGE • Increased CASH FLOW! • No UPFRONT sales tax in most states • RTO down payment can be a security deposit eliminating income tax • No sale, therefore no “gain on sale” profit recorded, so no income tax • Build profitable business sustainable through weak demand periods. • On a typical $4,000 cost vehicle sold for $8,800, AFTER TAX CASH INCREASE > $1,300

BHPH Sale vs. RTO Cash Flow Comparison Assumptions: Acquisition Cost $4,000 Sale price / Cap Cost $8,800 RFC Discount 35.00% Down payment/security deposit $1,000 Income tax rate 40.00% Sales tax rate 7.00% ”Related Finance Company.” To reduce the income tax liability on the “gain on sale”, typically the dealer establishes a wholly owned “Related Finance Company” to which the vehicle can be sold at a loss. However, the discount rate in the sale must reflect the true market value and cannot create a tax loss.

BHPH Sale vs. RTO Cash Flow Comparison – Cont’d RTO Cash Calculations: Flow Savings Initial Sales Tax $ 616 $ 616 Sale Price to RFC $5,720 Profit on RFC Sale $1,720 Income Tax on RFC Sale $ 688 $ 688 Total After Tax Cash Savings $ 1,304 (Only 100 vehicles) x 100 $130,400 200 vehicles - $260,800 Savings 300 vehicles - $391,200 Savings

Security Deposit vs. Capitalized Cost Reduction • Capitalized cost reduction (down payment) is taxable on sales tax, and federal and state income tax • Security deposit is non-taxable on any level and can be used to reduce tax exposure and increase cash flow • Security deposit can be used for default, excess mileage/wear or for repairs/maintenance

State Sales Tax Options • Monthly on payments collected: 33 states • Upfront on Capitalized Cost (similar to sale): 9 states (CO, IL, MT, NC, SC, TX, VA, AL*, DE*) • Upfront on monthly payments: 6 states (IO, ME, ND, NY, OH, SD) • Upfront on depreciation: 2 states (NJ, VT) • * Both on cap cost and monthly payments

Acceleration of Accounting Income • Accounting rules (FASB 13) allow RTO to be treated as a • “sale” for accounting purpose even though a RTO is (not a • sale) for tax purposes. • HUGE acceleration of income • Full $4,400 mark-up is immediate income with NO TAX LIABILITY

Acceleration of Accounting Income (cont.) • BHPH sale: finance books are SAME as tax books • RTO: finance books have ACCELERATED INCOME while tax books have tax deferral from accelerated depreciation • Banks and finance companies have used this tax deferral advantage

Advantages of RTO • No loss of prepaid sales tax on defaults (in most states) • Eliminates the need for an Related Finance Company • Better control of vehicle (e.g., increased security deposit for excess mileage during the lease) • Greater flexibility in program design (e.g. early termination, collateral substitution, vehicle maintenance and repair)

Advantages of RTO (cont.) • Bankruptcy protection • Reduced customer disclosures • Reduced State and Federal regulatory requirements compared to Reg. Z and MVRISA on sales • No APR or Reg. Z disclosure • No usury limits

RTO Implementation You Receive: • Program Handbook on all policies and requirements including residual values • RTO agreement + all forms/documents • Marketing plan • Sales system, training and collateral • Insurance selection and purchase

RTO Implementation – cont’d You Receive: • Lessors Contingent Liability Insurance • Independent Insurance Tracking • Physical Damage Insurance to protect your collateral • Payment Assurance / Asset Tracking –Starter Interrupt, & Payment Reminder

Getting Started Complete, sign & return the RTO License Agreement Complete, sign & return the Contingent Insurance Application Complete, sign & return the Physical Damage Insurance Set-Up Form Arceri & Associates (504) 309-3087 www.arceri-insurance.com arceri@live.com