Download

1 / 39

390 likes | 402 Views

Combining Supply and Demand. In this lesson, students will be able to identify factors which lead to equilibrium or disequilibrium in a market. Students will be able to identify and/or define the following terms: Equilibrium Disequilibrium Excess Demand Excess Supply Price Ceiling

E N D

Combining Supply and Demand In this lesson, students will be able to identify factors which lead to equilibrium or disequilibrium in a market. Students will be able to identify and/or define the following terms: Equilibrium Disequilibrium Excess Demand Excess Supply Price Ceiling Price Floor E. Napp

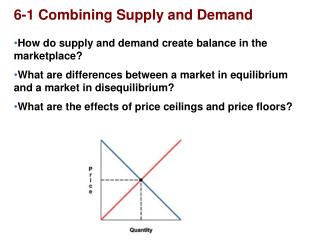

Essential Question EQ: How are supply and demand linked, and how do these factors shape modern free market economies? E. Napp

Do you notice the point where supply and demand intersect? E. Napp

Equilibrium • When creating a demand curve and a supply curve, there is a point where the curves intersect. This point is the equilibrium point. • Equilibrium occurs when the quantity demanded equals the quantity supplied. • A market is stable at equilibrium. E. Napp

If a seller has seven donuts on the shelf at $1 per donut, and consumers only want seven donuts at that price, then the market is at equilibrium. E. Napp

Disequilibrium • A market is at disequilibrium when the quantity demanded does not equal the quantity supplied. • If quantity demanded is greater than quantity supplied, excess demand occurs. • If quantity supplied is greater than quantity demanded, excess supply occurs. E. Napp

Low prices encourage consumers. Low prices can create excess demand. E. Napp

Excess Demand • Excess demand occurs when the actual price is lower than the equilibrium price. • Low prices encourage demand. • To fix this problem, prices must be raised. E. Napp

If every parent wants to purchase this toy for the holidays, excess demand can occur. E. Napp

However, if no one is buying, then excess supply occurs. E. Napp

Excess Supply • Excess supply occurs when quantity supplied is greater than quantity demanded. • The actual price is higher than the equilibrium price. • To fix this problem, prices must be lowered. E. Napp

The day after Valentine’s Day, consumers will not pay high prices for Valentine’s candy. E. Napp

Price Ceiling • A price ceiling is the maximum price that can be legally charged for a good or service. • The government interferes with market equilibrium when it creates a price ceiling. • Rent control is an example of a price ceiling. E. Napp

Rent control is an example of a price ceiling. E. Napp

Price Floor • A price floor is the minimum price that can be legally charged for a good or service. • The government interferes with market equilibrium when it creates a price floor. • Minimum wage is an example of a price floor. E. Napp

The minimum wage is an example of a price floor. E. Napp

If there are lots of apples in the market and little demand for apples, market disequilibrium occurs.

Let’s Review Equilibrium! • Equilibrium occurs when quantity supplied equals quantity demanded. • Economists state that a market will tend toward equilibrium. • This means that price and quantity will gradually move towards their equilibrium levels.

Equilibrium is the point where the supply curve intersects the demand curve.

Let’s Review Disequilibrium! • Disequilibrium occurs when the quantity supplied does not equal the quantity demanded. • Disequilibrium occurs when the price is not right. • If the price is too high or too low for that particular market, disequilibrium occurs.

The original equilibrium price does not work when the supply curve shifts.

Surplus • A surplus occurs when quantity supplied is greater than quantity demanded. • Another term for surplus is excess supply. • When a surplus occurs, the price must be lowered to restore the market to equilibrium.

Too many cookies and not enough consumers creates a surplus.

Shortage • A shortage is a situation in which quantity demanded is greater than quantity supplied. • Another term for shortage is excess demand. • When a shortage occurs, prices must be raised to restore the market to equilibrium.

When quantity demanded is created than quantity supplied, a shortage occurs.

Prices • Market disequilibrium occurs when the price is not right for that particular market. • If the price is too low for that particular market, demand is encouraged and shortage occurs. • If the price is too high for that particular market, demand is discouraged and surplus occurs.

Prices are like the lights on a traffic light. Prices are signals for buyers and sellers.

High Prices • High prices send different signals to consumers and suppliers. • Consumers view high prices as a red light. • Suppliers view high prices as a green light.

Consumers view high prices as a red light because when prices are high, money buys less.

However, suppliers view high prices as a green light because high prices signify greater profits.

Low Prices • Low prices also send different signals to consumers and suppliers. • Consumers love low prices. • Suppliers are discouraged by low prices.

Low prices encourage consumers. Low prices allow consumers to increase their purchases. Money buys more at lower prices.

Low prices discourage suppliers. Low prices lead to decreased profits.

The Flexibility of Price • Fortunately, price is flexible and can be easily changed. • Market equilibrium can be restored by changing the price of a good or service. • The flexibility of price allows for market equilibrium to be restored easily.

Rationing • Rationing is a system where the government allocates all goods and services. • People do not buy goods and services. • Rationing is not based on price. • Centrally planned economies use rationing.

During World War II, the United States’ government used rationing of some products.

Rationing is costly to administer because it requires government planning.

Questions for Reflection: • When does equilibrium occur in a market? • Why does excess demand create disequilibrium in the market? • Define excess supply. • Why does the government place a price ceiling on rent? • How does rent control help some but hurt others? • Provide an example of a price floor. E. Napp