Download

1 / 3

30 likes | 48 Views

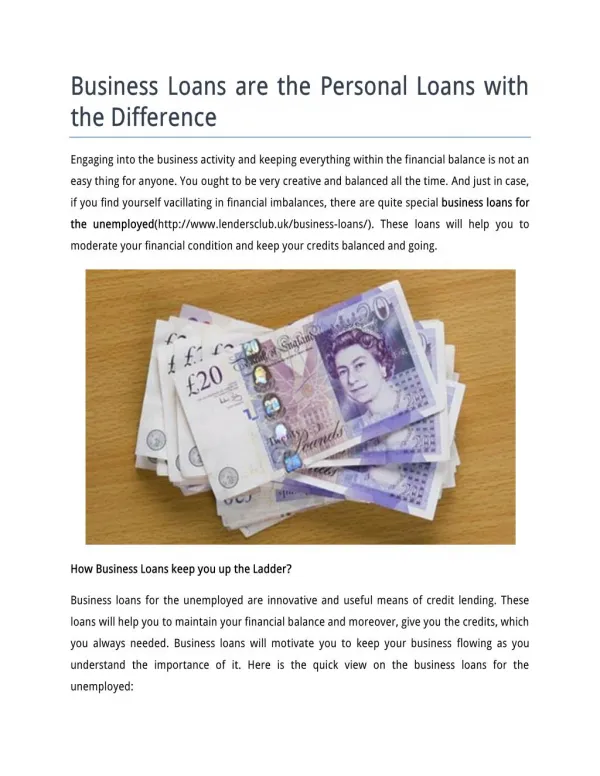

Can I take more than two personal loans at a given time? This question is not hard for you to imagine if you have a current personal loan your wedding expenses, and now you need money to renovate your home.

E N D

How Many Personal Loans Can You Have? bestpersonalloanrate.com/how-many-personal-loans-can-you-have Can I take more than two personal loans at a given time? This question is not hard for you to imagine if you have a current personal loan your wedding expenses, and now you need money to renovate your home. Often applying for a second personal loan proves to be a wise decision, especially if you have underestimated the amount of cash you need for an event or a big home improvement project. However, before you search for a lender, note that taking out more than one loan is not only expensive but risky for your financial stability as well! Can you take a second personal loan if you already have one? Yes, in most cases, you are allowed to take another personal loan if you have one in your name. However, lenders will grant you this loan only if you have paid off the initial balance in part and have a good history of repayments done on time. Experts in debt management say that though taking out a second personal loan might seem to be a practical option for you to tackle sudden financial expenses, it is generally not a good idea. You face the risks of getting caught in a vicious cycle of debt if you are not careful. Beware of too many loans & do not fall into the trap of over-borrowing There is another reason why you should think twice before applying for a second personal loan- over-borrowing. In case you borrow more than you need, your payments every month will increase, and the overall expenses of your loan will shoot up. This 1/3

makes it hard for you to repay your debt. This is the first step you take to enter into a cycle of loans, especially if it becomes your primary source of capital. To ward off the harmful effects of over-borrowing, you need to calculate precisely how much money you require before applying for the loan. When you have estimated how much money you need for the loan, ask for that amount only. Compare lenders in the market that give you multiple loans To take out more than one personal loan, you need to approach the right lender. Research and take time to compare credible lenders in the market that give you more than one personal loan. Most lenders will approve the personal loan under the following circumstances- 1. The present active loan should be in good standing 2. Credit score should be good 3. No late payments recently made 4. Other factors for eligibility that differ from lender to lender At one time, how many personal loans can you take? The number of personal loans you can take at one time depends upon your income and lender. Most lenders of personal loans will not approve your application if your debt to income ratio is about 43% or more in the USA and Canada. This implies your loan payments for every month, bills, and other expenses should not be over 43% of the income you earn before you pay your taxes. Wait before taking out another personal loan Experts in debt management suggest you should wait before taking out another personal loan for the following reasons- 1. You won’t get the best deals– If you have already taken out a personal loan, your credit score has reduced already. For the second loan application, there are hard credit checks, and the lender will view you more of a risk. 2. Your debt to income ratio will increase– Besides reduced credit scores, another loan means your debt to income ratio will become higher. This means you will face a lot of trouble getting approved for the second loan or even a credit card with an excellent competitive rate of interest in the market. 3. Borrowing in the future will be harder– Applying for a loan at times is excellent for instant credit if you do it in moderation. However, it will not give you a good record if you have several inquiries on your credit report. 4. You might not get the finance you need even after taking the loan– If you regularly take out loans to cover daily costs, this is an excellent indicator to the lender that you are in a cycle of debts. In case, you have a loan already and wish to keep debt at bay, and it makes sense to contact a credible company in debt relief for advice. 2/3

5. Your monthly payments will increase– Multiple loans indicate several repayments every month. Lenders will never approve a loan you cannot afford. In case your financial situation worsens, making these repayments will be even more challenging Still, want to apply for another personal loan? If you still want to apply for a second personal loan in a short period, shop for the best rates online. In case you are applying for a similar sum of money like in the previous loan with the same lenders, credit bureaus will identify you are attempting to search for the best rate but not trying to get a loan. These credit report agencies take all hard inquiries within a specific time, generally between 14 to 45 days, and place it under a single category. This hard inquiry will not be printed immediately on the credit report, so you still get time to search for multiple loans while keeping your first credit profile. Before you apply for the best personal loan, check your credit report first. If there are any mistakes, get them corrected before you apply for the loan. Make all your repayments for the current personal loan in time. Attempt to clear as much of the existing loan as possible. Be informed and aware of how much you can afford. When you get an accurate idea of how much you can pay on your second loan, you can find the right loan for urgent expenses that crop up over time. Make sure you invest time in extensive research online and get the best competitive rates in the market. 3/3