Download

1 / 12

150 likes | 422 Views

Generally Accepted Accounting Principle. A generally accepted accounting principle is one of several principles ( or concepts) that are guidelines for financial accounting. The Principle of Consistency.

E N D

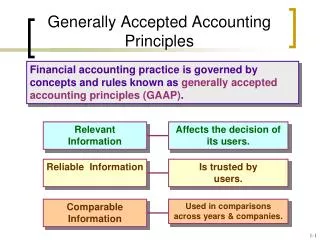

Generally Accepted Accounting Principle A generally accepted accounting principle is one of several principles (or concepts) that are guidelines for financial accounting.

The Principle of Consistency • This principle states that the consistency pertaining to the methods of accounting must be maintained in each fiscal period.

What does this mean? • This means that the same methods and procedures of accounting are to be used throughout a fiscal period and in each fiscal period.

How does this affect a business? • It prevents a business from changing its methods of accounting. • If a business decides to switch, it must be clearly indicated on the financial statements with explanations.

Why is this principle important? • A person reading financial statements has the right to assume this principle has been followed. • Without this principle being followed, it is very difficult to preform a proper analysis of a business’ financial situation.

Why is this principle important? • It allows for ease of reading and understanding when each period follows the same methods. • It makes it easier to compare financial records from different periods.

By not following this principle a business could: • Manipulate accounting methods to appear as if they are making more money. • Provide potentially misleading information to the government and the public.

Example • A company with a large amount of assets may wish to change the method of depreciation that they used to value them. (Declining balance depreciation Straight line method). • In order to change this it must be clearly indicated why this change is being made as well as the effects this change will have.

True or False • The consistency principle requires that methods and procedures are kept the same through periods. • You can change accounting methods at any time without notice. • Once you formally adopt a new method, you can change back to the old method as you please. • The consistency principle is commonly ignored when the owner of a business wants to report misleading information. TRUE FALSE FALSE TRUE

True of False • A business can only change accounting methods every four years. • Its is very difficult to preform an analysis of a business’s financial situation if the consistency principle is not followed. • If the consistency principle is followed, it is more difficult to compare financial records from different periods. • One of the jobs of an auditor is to determine whether the consistency principle has been followed. FALSE TRUE FALSE TRUE

Does this follow the consistency principle? • A small business owner decides that he does not like his old methods of accounting. He decides that he will change them when the next fiscal period starts. He does not tell anyone of this change. • A small business owner decides that he does not like his old methods of accounting. He decides that he will change them and tells his accountant

A small business owner decides that he does not like his old methods of accounting. He decides that he will change them. He asks permission from the government auditor the next time an audit is done. • A small business owner decides that he does not like his old methods of accounting. He decides that he will change them and clearly states in the financial records why the change is being made, what effects the change will have, and when the change took place.