Download

1 / 6

110 likes | 552 Views

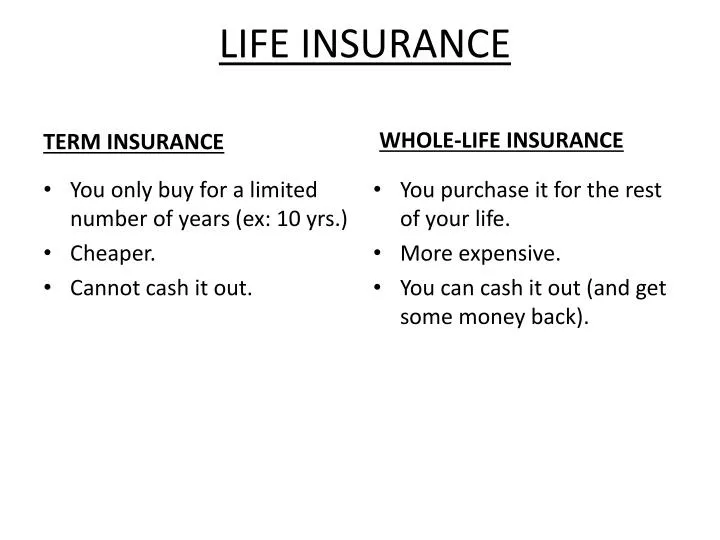

LIFE INSURANCE. TERM INSURANCE. WHOLE-LIFE INSURANCE. You purchase it for the rest of your life. More expensive. You can cash it out (and get some money back). You only buy for a limited number of years (ex: 10 yrs.) Cheaper. Cannot cash it out. What the family receives….

E N D

LIFE INSURANCE TERM INSURANCE WHOLE-LIFE INSURANCE You purchase it for the rest of your life. More expensive. You can cash it out (and get some money back). • You only buy for a limited number of years (ex: 10 yrs.) • Cheaper. • Cannot cash it out.

What the family receives… *If the person passes away during a contract, the “beneficiaries” get the whole contract amount. (Ex: $300 000 or even $1 000 000.) But, if the person passes away after a term contract is over, the family gets nothing. The amount the family gets is: -“All or nothing!” -It does not matter how many payments you made or how old you are or if you are male or female, etc. -It is a flat rate. -It is not a calculation! -It is not related to how much you paid each year.

Steps: These steps are the same for both charts: • Find chart number • X $000’s • +75 Ex: $200 000 policy: COST PER YEAR=$200 X chart + 75 = ? Payment Plans (Note: Monthly = x 0.09) (NOT ÷ 12) (Note: Semi-annual = x 0.52) (Note: Do this extra step using your full year amount after the $75.) ***Note: Payments plans are more affordable but cost more overall!

‘Cash Surrender’aka ‘Cash Out’ (Note: This offer only applies to WHOLE LIFE.) How to use the chart: • ‘Policy Year’ (middle column) = # of yrs you had the contract = your age when you want to cash out MINUS the age when you started the contract. • ‘Issue Age’ (top heading) = your age when you started contract. • Cash back amount = chart x $000’s (same steps as usual!)

‘Cash Surrender’aka ‘Cash Out’ • You may get more or less than you paid into the contract so far. • The longer you have had the contract the more you will get! • Note: There is no $75 fee or monthly calculations at the bottom of this chart!

Answers: #6.a) $222.20 b) $2265 c) $2919 d) $873 #7.a) $507 b) $1521 c) $300000 d) 0! Contract is over. #8.a) $287.80 b) $25.90 c) $23 #9.a) $588 b) $1065 c) $477 #10.a) $591 b) $2035 c) $1444 #11.a) $1465.80 b) $762.22 twice a yr ($1524.44 total) c)$43320 #12.a) $1497 b) $15600 c) $54400 d) $38800 e) $14970