Download

1 / 14

140 likes | 291 Views

Financial System and Allocation of Saving. A successful economy uses its savings for investments that are likely to be the most productiveThe interest on deposits is one important reason people put savings in banksThe financial system improves the allocation of savingProvides information to saver

E N D

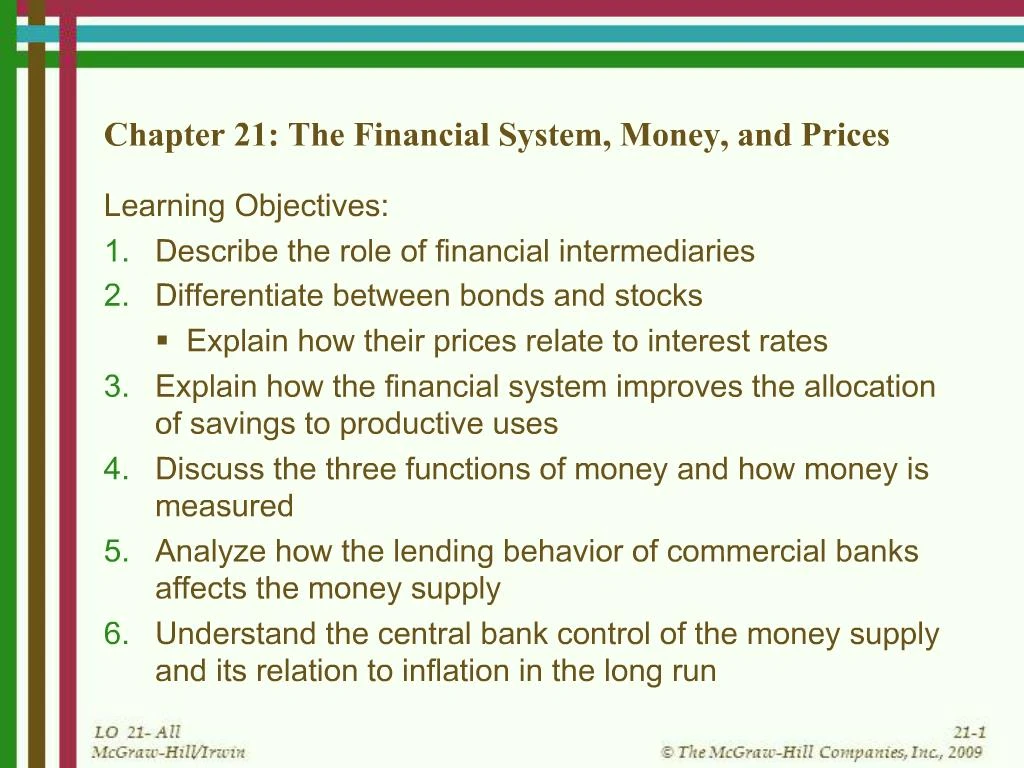

1. Chapter 21: The Financial System, Money, and Prices Learning Objectives:

Describe the role of financial intermediaries

Differentiate between bonds and stocks

Explain how their prices relate to interest rates

Explain how the financial system improves the allocation of savings to productive uses

Discuss the three functions of money and how money is measured

Analyze how the lending behavior of commercial banks affects the money supply

Understand the central bank control of the money supply and its relation to inflation in the long run

2. Financial System and Allocation of Saving A successful economy uses its savings for investments that are likely to be the most productive

The interest on deposits is one important reason people put savings in banks

The financial system improves the allocation of saving

Provides information to savers about the possible uses of their funds

Help savers share the risks of individual investment projects

Risk sharing makes funding possible for projects that are risky but potentially very productive

3. Banking System Financial intermediaries are firms that extend credit to borrowers using funds raised from savers

Thousands of commercial banks accept deposits from individuals and businesses and make loans

Banks and other intermediaries specialize in evaluating the quality of borrowers

Principle of Comparative Advantage

Banks have lower cost of evaluating opportunities than an individual would

Banks pool the savings of many individuals to make large loans

4. Bonds A bond is a legal promise to repay a debt

Each bond specifies

Principal amount, the amount originally lent

Maturation date, the date when the principal amount will be repaid

The term of a bond is the length of time from issue to maturation

Coupon payments, the periodic interest payments to the bondholder

Coupon rate, the interest rate that is applied to the principal to determine the coupon payments

5. Bond Market Bonds can be sold before their maturation date

Market value at any time is the price of the bond

Price depends on the relationship between the coupon rate and the interest rate in financial markets

A two-year government bond with principal $1,000 is sold for $1,000, 1/1/09

Coupon rate is 5%

$50 will be paid 1/1/10

$1,050 will be paid 1/1/11

Bond's price on 1/1/10 depends on the prevailing interest rate

6. Stocks A share of stock is a claim to partial ownership of a firm

Receive dividends, a periodic payment determined by management

Receive capital gains if the price of the stock increases

Prices are determined in the stock market

Reflect supply and demand

7. Risk Premium Risk premium is the difference between the required rate of return to hold risky assets and the rate of return on safe assets

Suppose interest on a safe investment is 6%

FortuneCookie.com is risky, so 10% return is required

Stock will sell for $80 in 1 year; dividend will be $1

(Stock price) (1.10) = $81

Stock price = $73.64

Risk aversion increases the return required of a risky stock and lowers the selling price

8. Bond Markets and Stock Markets Channel funds from savers to borrowers with productive investment opportunities

Sale of new bonds or new stock can finance capital investment

Like banks, bond and stock markets allocate savings

Provision of information on investment projects and their risks

Provide risk sharing and diversification across projects

Diversification is spreading one's wealth over a variety of investments to reduce risk

9. Stock and Bond Markets Savers can put savings into a variety of financial assets

Diversification makes risky but potentially valuable projects possible

No individual saver bears the whole risk

Society is better off

A mutual fund is a variety of financial assets sold to the public as shares in a single financial intermediary

Diversified asset for the saver

Less costly than buying many stocks and bonds directly

10. Money Money is any asset that can be used in making purchases

Examples include coins and currency, checking account balances, and traveler's checks

Shares of stock are not money

Money has three principal uses

Medium of exchange

Unit of account

Store of value

Money makes barter unnecessary

Barter is trading goods directly

11. Bank Reserves Cash in a bank's vault is not part of the money supply

Unavailable for payments

Bank deposits available for use in transactions are part of the money supply

Depositing a $100 bill in your checking account does not change the money supply

Bankers realize that inflows and outflows from vaults leave some guilders unused

Only 10% of deposits are needed for transactions

90% can be lent to borrowers for a fee -- interest

12. The Federal Reserve System The Fed is the central bank of the US

Responsible for monetary policy and the oversight and regulation of financial markets

Monetary policy is deciding and managing the size of the nation's money supply

Money supply is controlled indirectly

Open-market purchase of government bonds from the pubic by the Fed increases bank reserves and the money supply

Open-market sale of government bonds by the Fed to the public decreases reserves and money supply

13. Open Market Operations When the Fed purchases a bond from the public

Fed pays bond holder with new money

Receipts are deposited and this leads to a multiple expansion of the money supply

When the Fed sells a bond to the public

Bondholder pays with checking funds

Bank reserves decrease and this leads to a multiple contraction of the money supply

14. Velocity of Money (V) Velocity is the speed money changes hands in transaction for final goods and services

Nominal GDP is the price level (P) times real GDP (Y)

M is the money supply

15. Money and Inflation in the Long Run Quantity equation states (M) (V) = (P) (Y)

Restatement of the velocity definition

The quantity equation relates the money supply to price levels

Suppose velocity and real GDP are constant

The quantity equation becomes

An increase in the money supply by a given percentage would increase prices by the same percentage