Download

1 / 21

210 likes | 418 Views

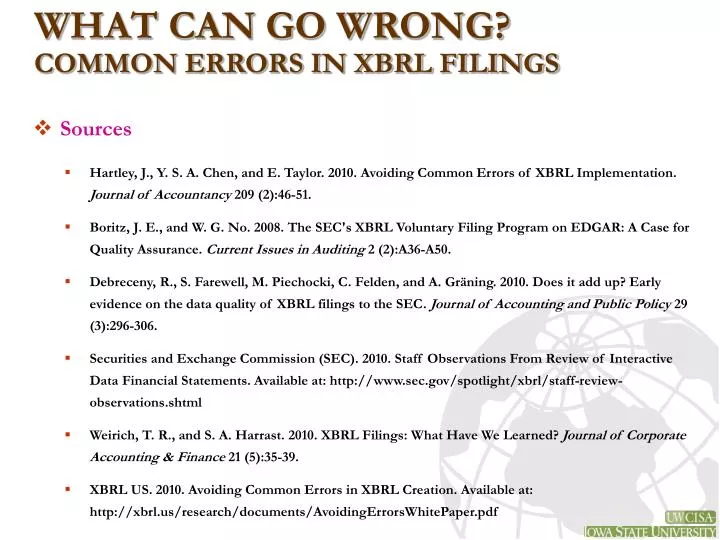

WHAT CAN GO WRONG? COMMON ERRORS IN XBRL FILINGS. Sources Hartley , J., Y. S. A. Chen, and E. Taylor. 2010. Avoiding Common Errors of XBRL Implementation. Journal of Accountancy 209 (2): 46-51.

E N D

WHAT CAN GO WRONG? COMMON ERRORS IN XBRL FILINGS • Sources • Hartley, J., Y. S. A. Chen, and E. Taylor. 2010. Avoiding Common Errors of XBRL Implementation. Journal of Accountancy 209 (2):46-51. • Boritz, J. E., and W. G. No. 2008. The SEC's XBRL Voluntary Filing Program on EDGAR: A Case for Quality Assurance. Current Issues in Auditing 2 (2):A36-A50. • Debreceny, R., S. Farewell, M. Piechocki, C. Felden, and A. Gräning. 2010. Does it add up? Early evidence on the data quality of XBRL filings to the SEC. Journal of Accounting and Public Policy 29 (3):296-306. • Securities and Exchange Commission (SEC). 2010. Staff Observations From Review of Interactive Data Financial Statements. Available at: http://www.sec.gov/spotlight/xbrl/staff-review-observations.shtml • Weirich, T. R., and S. A. Harrast. 2010. XBRL Filings: What Have We Learned? Journal of Corporate Accounting & Finance 21 (5):35-39. • XBRL US. 2010. Avoiding Common Errors in XBRL Creation. Available at: http://xbrl.us/research/documents/AvoidingErrorsWhitePaper.pdf

COMMON ERRORS IN SEC FILINGS XBRL US (2010): 1,400 Filings & 5,000 Problems

COMMON ERRORS IN SEC FILINGS • Fail to identify/propagate errors in original records or filings. c From Traditional Financial Reporting Process a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Mapping • Identify base taxonomy. • Map financial facts to XBRL elements. • Identify financials facts that do not matchto base taxonomy elements. From Traditional Financial Reporting Process • Select a less appropriate standard element when it appears a more appropriate standard element exists. a, b & d • Select a standard element when it appears a new element should have been created. d a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Select a less appropriate standard element when it appears a more appropriate standard element exists. a, b & d

COMMON ERRORS IN SEC FILINGS • Select a less appropriate standard element when it appears a more appropriate standard element exists. a, b & d Narrower definition

COMMON ERRORS IN SEC FILINGS • Mapping • Identify base taxonomy. • Map financial facts to XBRL elements. • Identify financials facts that do not matchto base taxonomy elements. From Traditional Financial Reporting Process • Extending • Create the company extension taxonomy as an extension of the base taxonomy. • Create a new element when it appears an appropriate standard element exists (e.g., create a new element ‘Salaries’ when a standard element ‘SalariesAndWages’ exists). a, d & f • Improperly represent the relationship among elements (e.g., fail to establish methodical relationship among elements in a calculation linkbase and present elements in the wrong location in a presentation linkbase). a, b & c a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Create a new element when it appears an appropriate standard element exists . a, d & f

COMMON ERRORS IN SEC FILINGS • Create a new element when it appears an appropriate standard element exists . a, d & f

COMMON ERRORS IN SEC FILINGS • Mapping • Identify base taxonomy. • Map financial facts to XBRL elements. • Identify financials facts that do not matchto base taxonomy elements. From Traditional Financial Reporting Process • Extending • Create the company extension taxonomy as an extension of the base taxonomy. • Report incorrect negative values. a, c, d, c & f • Fail to report required values. e • Use elements that have been removed from the taxonomy. e • Inappropriately use context references (e.g., roll-forward: fail to use the same instance context reference for the beginning balance as for the end of the previous period). b & d • Neglect to tag amounts appearing parenthetically in the financial statements (e.g., the allowance for doubtful accounts and shares of stock outstanding). e • Fail to tag another required value when another value is reported (e.g., a company failed to report impact on non-controlling interest (subsidiary) when it reported purchases of additional shares of a subsidiary). e • Tagging • Create an instance document by: • associating the fact values being reported in a given filing with specific elements in the taxonomies. • defining periods, units of measures, and other aspects specific to that report. a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Mapping • Identify base taxonomy. • Map financial facts to XBRL elements. • Identify financials facts that do not matchto base taxonomy elements. From Traditional Financial Reporting Process • Extending • Create the company extension taxonomy as an extension of the base taxonomy. • Report values when the values should be zero or not disclosed (e.g., report the value of new stock issued that includes a treasury stock). e • Report the value that should be zero when another value is reported (e.g., common stock and additional paid in capital: could be reported as combined amount or as separate amounts in the shareholders equity table, but not both). e • Duplicate reported values that do not match. e • Improperly tag values (i.e., data-entry errors). b & d • Rounding error and inappropriate use of decimals (e.g., report two decimal values but set the decimal attribute to 0, instead of 2). c & f • Tagging • Create an instance document by: • associating the fact values being reported in a given filing with specific elements in the taxonomies. • defining periods, units of measures, and other aspects specific to that report. a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Report incorrect negative values. a, c, d, c & f

COMMON ERRORS IN SEC FILINGS • Report incorrect negative values. a, c, d, c & f

COMMON ERRORS IN SEC FILINGS • Neglect to tag amounts appearing parenthetically in the financial statements (e.g., the allowance for doubtful accounts and shares of stock outstanding). e

COMMON ERRORS IN SEC FILINGS • Improperly tag values (i.e., data-entry errors). b & d

COMMON ERRORS IN SEC FILINGS • Rounding error and inappropriate use of decimals. c & f

COMMON ERRORS IN SEC FILINGS • Mapping • Identify base taxonomy. • Map financial facts to XBRL elements. • Identify financials facts that do not matchto base taxonomy elements. From Traditional Financial Reporting Process • Extending • Create the company extension taxonomy as an extension of the base taxonomy. • Tagging • Create an instance document by: • associating the fact values being reported in a given filing with specific elements in the taxonomies. • defining periods, units of measures, and other aspects specific to that report. • Fail to adequately validate the instance document and the company extension taxonomy both manually and with validation tools. b & d • Fail to adequately review the rendered instance document both manually and with rendering tools. d & f • Reviewing • Validate the instance document and company extension taxonomy against the XBRL specification and regulatory requirements. • Render the instance document. a: Bartley et al. (2010) b: Boritz and No (2008) c: Debreceny et al. (2010) d: SEC(2010) e: XBRL US (2010) f: Weirich and Harrast (2010)

COMMON ERRORS IN SEC FILINGS • Fail to adequately validate the instance document and the company extension taxonomy both manually and with validation tools. b & d