Download

1 / 7

70 likes | 165 Views

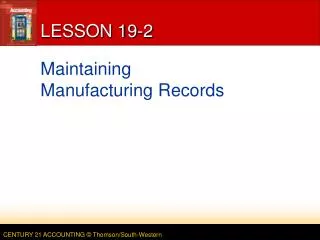

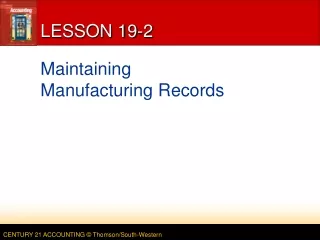

LESSON 19-2. Determining the Cost of Merchandise Inventory. FIRST-IN, FIRST-OUT INVENTORY COSTING METHOD. page 569. 3. 4. 2. 5. 1. 1. Total units on hand. 2. Units from the most recent purchase. 3. Units needed to equal the total units on hand. 4. Unit price times fifo units.

E N D

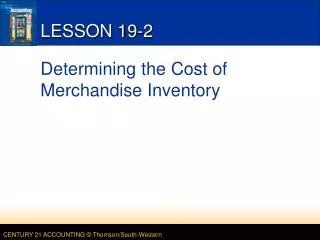

LESSON 19-2 Determining the Cost of Merchandise Inventory

FIRST-IN, FIRST-OUT INVENTORY COSTING METHOD page 569 3 4 2 5 1 1. Total units on hand 2. Units from the most recent purchase 3. Units needed to equal the total units on hand 4. Unit price times fifo units 5. Total fifo cost LESSON 19-2

3 2 4 1 LAST-IN, FIRST-OUT INVENTORY COSTING METHOD page 570 5 6 1. Total units on hand 2. Beginning inventory units 5. Unit price times lifo units 3. Units from the earliest purchase 6. Total lifo cost 4. Units needed to equal total units on hand LESSON 19-2

WEIGHTED-AVERAGE INVENTORY COSTING METHOD page 571 1. Total cost of inventory available 2. Weighted-average price per unit 1 3. Cost of ending inventory 2 3 LESSON 19-2

Cost ofMerchandiseAvailable for Sale – Fifo Cost of EndingInventory = Cost ofMerchandiseSold CALCULATING THE COST OF MERCHANDISE SOLD page 572 $1,020.00 – $386.00 = $634.00 LESSON 19-2

COMPARISON OF INVENTORY METHODS page 572 LESSON 19-2

TERMS REVIEW page 573 • first-in, first-out inventory costing method • last-in, first-out inventory costing method • weighted-average inventory costing method LESSON 19-2