Download

1 / 12

120 likes | 261 Views

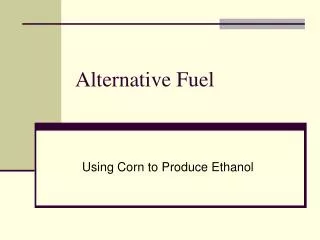

Commercial Aviation: The Quest for Sustainable and Affordable Alternative Jet Fuel. John P. Heimlich VP and Chief Economist DOT Future of Aviation Advisory Committee Meeting August 25, 2010. Airline Energy Costs Are High and Poised to Rise. Average U.S. Price per Gallon of Jet Fuel.

E N D

Commercial Aviation: The Quest for Sustainable and Affordable Alternative Jet Fuel John P. Heimlich VP and Chief Economist DOT Future of Aviation Advisory Committee Meeting August 25, 2010

Airline Energy Costs Are High and Poised to Rise Average U.S. Price per Gallon of Jet Fuel Source: Energy Information Administration

Airlines Have Opportunity to Reinvent Supply Chain, Alleviate Dependence on Traditional Refining Economics Propane|Butane|Propylene|Butylene 3.5 8% Finished Motor Gasoline(including Naphtha*) Light (52%) Distillates 19.6 44% Gallons total 44.7 due to “processing gain” Kerosene | Jet Fuel 4.1 9% Middle (35%) Distillates Heating Oil and Diesel Fuel 11.7 26% Heavy (13%) Distillates** Lubricants|Wax|Asphalt|Tar|Fuel Oils 3.3 7% Petroleum Coke and Other 2.5 6% * Feedstock for high-octane gasoline, petrochemicals and solvents ** Includes heavy oils and residuum used in industry, marine transportation and electric-power generation Sources: EIA and American Petroleum Institute 3

Quest for Alternative Fuels Aligns with FAAC Focus on Enhancing Industry Viability/Competitiveness/Workforce • Average fuel expense hit 36% of U.S. passenger airline costs in 3Q08; every penny-per-gallon means $175M-200M/year • A petroleum-dependent aviation industry is susceptible to price shocks, supply disruptions, carbon constraints, etc. • Alternative fuels can reduce CO2 and other polluting emissions (e.g., sulfur, particulate matter) • “Drop-in” fuels mean no changes to airplanes/airports/pipelines • Alternative fuels support green jobs – economic development • U.S transportation/agriculture/energy policies are key enablers • Economic and environmental aspirations aligned with FAAC mission 4

How Can Airlines Derive CO2 Emissions Benefit? Improvements Across the “Life Cycle” of the Fuel • CO2 “life cycle” analysis for jet fuel includes: • Feedstock generation (e.g., crude oil versus crops) • Transportation of feedstocks for processing • Processing of feedstocks into jet fuel • Distribution/transportation of jet fuel to airports • Combustion of jet fuel in the aircraft • Opportunities for benefit with alternatives: • Using plants (biomass) as feedstock sequesters carbon in a loop, whereas fossil fuel releases carbon sequestered long ago • New methods could be used to reduce or sequester emissions when being transported and/or processed • Higher energy density could yield CO2 decreases upon combustion 5

Partnerships and Progress The Commercial Aviation Alternative Fuels Initiative (CAAFI) • Airlines/airports/manufacturers/FAA co-founded CAAFI in 2006; includes universities, think tanks, government labs, energy start-ups and major oil companies, bankers, etc. • Collaboration between CAAFI and DOD/DOE/EPA/USDA • Secured passage of ASTM D7566 for synthetic fuels; working to ensure approvals of HRJ and other pathways • CAAFI received Joseph S. Murphy Industry Service Award from Air Transport World in Jan. 2010 for efforts to pave the way for use of sustainable biofuels in aviation • Forging deeper ties with state and local economic development authorities to facilitate projects, along with Sustainable Aviation Fuels Northwest and others

Commercial & Military Aviation in Strategic Alliance DOD Ability to Contribute to Accelerated Deployment Constrained • ATA/DLA formed strategic alliance “to explore cooperative market engagement for fuel, improve the financial prospects for alternative fuels infrastructure, accelerate fuel certification and refine methodology for determining environmental impacts” • Jointly advertise requirements to supply airports/USAF/USNA with competitively priced, environmentally preferred, reliably delivered, operationally secure jet fuel • DOD contracting authority limited to 5 years; seeking up to 20 years (supported by ATA) • DLA and PACOM partnering with ATA, Boeing, FAA and USDA in “Farm to Fly”

Commercial Off-Take Agreements Key to Progress ATA/CAAFI Key Facilitators of Airline-Supplier Discussions • ATA has facilitated one ground-fuel contract and two jet-fuel MOUs • Aug. 2009 – 8 U.S. airlines signed 5-year contract with Rentech and ASIG for renewable synthetic diesel from urban woody waste for 2012 use in LAX GSE • Dec. 2009 – 15 airlines from the U.S., Canada, Mexico and Germany announced MOUs with two suppliers supporting two refining processes • Rentech: Fischer-Tropsch jet fuel (250m gal/year) using coal or petroleum coke and biomass, with CO2 sequestration, at a plant in Natchez, Mississippi • AltAir Fuels: HRJ fuel (50m gal/year) and diesel (20m gal/year) using camelina or other non-food crops (e.g., algae, jatropha) at a West Coast refinery by 2013 July 2010 – United Airlines signed MOU with Gevo for future supply of biobutanol for flights at Chicago O’Hare; other airlines evaluating this project and others Aug. 2010 –Discussions ongoing with AltAir, Amyris, BioPure Fuels, Byogy, Gevo, JetE, LS9, NextStep Energy, Rentech, Sapphire, Sasol, Solazyme, Solena, others

Key Challenges Remain to Deployment • Price Stability and Affordability • Getting facilities built and crops grown is important, but price of resultant fuel (largely derived from cost of feedstock) must be competitive with market price of jet fuel; multiyear financial incentives (e.g., tax credits) critical to enable airline/supplier off-take agreements • Certification • Hydrotreated renewable jet (HRJ) not yet approved by ASTM (est. 1Q11); additional pathways (e.g., hydrolysis/fermentation, lignocellulosic bioconversion, pyrolysis/liquefaction) promising large, environmentally beneficial volumes could take years (and $) to approve • Feedstock Readiness • Industry working with USDA to enhance commercial quantities of sustainable, cost-competitive, flight-ready aviation biofuels

Key Challenges Remain (Cont’d) • Crediting of Environmental Benefit • Airlines typically commingle the fuel they purchase in common-carrier multiproduct pipelines and airport fuel-storage facilities, such that the purchasing airline might not actually fly with the exact fuel it purchases • Uncertainty as to whether regulatory structure will accord credit to airline that purchases the more environmentally beneficial fuel • Compatibility of International and Domestic Acceptance Criteria • Lack of consistent/compatible environmental criteria worldwide for alternative fuels in international aviation could impede deployment • Applies not only to compatibility with other countries, but also within the United States (e.g., emerging state programs for low-carbon fuel)

Alternative Energy Is Inevitable,But Aviation Must Not Be Left Behind “The Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil.” — Sheikh Zaki Yamani, former oil minister of Saudi Arabia, Oct. 23, 2003 “The Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil.” — Sheikh Zaki Yamani, former oil minister of Saudi Arabia, Oct. 23, 2003

www.airlines.org When America Flies, It Works