Download

1 / 24

240 likes | 334 Views

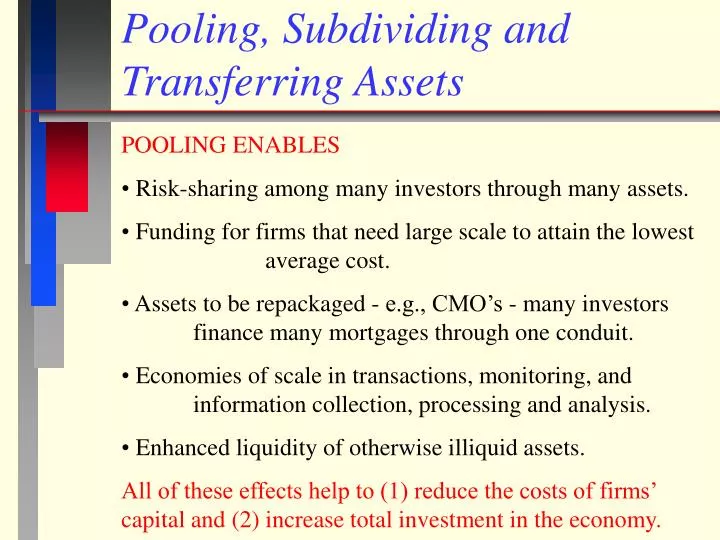

Pooling, Subdividing and Transferring Assets. POOLING ENABLES Risk-sharing among many investors through many assets. Funding for firms that need large scale to attain the lowest average cost.

E N D

Pooling, Subdividing and Transferring Assets • POOLING ENABLES • Risk-sharing among many investors through many assets. • Funding for firms that need large scale to attain the lowest average cost. • Assets to be repackaged - e.g., CMO’s - many investors finance many mortgages through one conduit. • Economies of scale in transactions, monitoring, and information collection, processing and analysis. • Enhanced liquidity of otherwise illiquid assets. • All of these effects help to (1) reduce the costs of firms’ capital and (2) increase total investment in the economy.

Good examples of the usefulness of pooling are syndicates. • Syndicates of banks often pool their funds to finance large risky loans to developing countries. • Race horse syndicates buy thoroughbreds for racing. • See horseracing.miningco.com/sports/horseracing/ and click on “partnerships”.

Evolution of Financial Products - Pooling/Subdivide Generation Security Underlying Asset 1st Stocks Net Assets of Firm 2nd Passthroughs Many Pooled Assets - MFs 3rd Collateralized Pooled Assets’ Cash Flows Obligations Stripped And Reassembled 4th Swaps Cash Flows on Notional Amounts 5th Structured Notes Indexed Partitioning of Pooled Assets’ Cash Flows 6th Credit Derivatives External Credit Enhancements

Swaps and securities facilitate transfer across time and space. Example: Mortgagee presents S&L with pay-fixed (mortgage rate, receive variable (CD rate) swap. In the past, S&L held the swap and suffered losses if interest rates increased. Now the S&L can transfer the swap to another party that naturally wants to receive fixed and pay variable, such as a European bank.

The Transactions Costs of Acquiring a 40 Stock Portfolio Household Median Investment Number of % Commission Income Net Per Shares Per Per Dollar Quintile Worth Company Company Invested -------------------------------------------------------------------------------------------------- Bottom 4,324 108.10 2.7 72 2 19,694 492.35 12.3 16 3 28,044 701.10 17.5 12 4 46,253 1,156.33 28.9 9 Top 111,770 2,794.25 68.9 5 In 1990, for all but the wealthiest income group, commissions alone cost considerably more than the fees typically charged by mutual funds. Falling transactions costs and growing incomes may make direct investing possible for more people, but the fees of mutual funds may fall as well.

Risk Costs of Buying Round Lots - Holding Fewer Stocks Household Median Number Portfolio Penalty for % Commission Income Net of Round Standard Undiversified Per Dollar Quintile Worth Lots Deviation Risk (%) Invested -------------------------------------------------------------------------------------------------- Bottom 4,324 1.1 48.0 9.26 3.9 2 19,694 4.9 28.3 2.91 4.1 3 28,044 7.0 25.8 2.11 4.1 4 46,253 11.6 23.8 1.46 4.1 Top 111,770 27.9 21.1 0.58 4.1 Here there are two costs to consider. Buying round lots reduces commission costs to about 4 percent, but there is a risk cost. A portfolio return penalty is the difference between the expected return on the given portfolio and a leveraged diversified portfolio with the same standard deviation.

Pooled Investors Still Need to Monitor the Asset Manager Measuring Asset Manager Performance - Mutual Funds Alpha Measures - use regression 1. Jensen’s model based on CAPM -> Rp = Rf + B[Rm -Rf] - Run the regression [Rp - Rf ] = a + B[Rm -Rf] + e where the funds’ portfolio return is Rp, the risk-free return is Rf, the expected market return is Rm, alpha is a, beta is B, and e is the regression error term. 2. Treynor/Mazuy version of this model includes a squared term to account for nonlinear effects. - Run [Rp - Rf ] = a + B1[Rm -Rf] + B2[Rm -Rf]2 + e

More Performance Measures Other alpha-type performance models add other indexes to control for other systematic return factors. 3. Fama-French Model - adds small stock (SMB) and book-to-market factors (HML) to Jensen’s model. SMB is the difference in return between a portfolio of the smallest stocks and a portfolio of the largest stocks. HML is the difference in return between a portfolio of the high book value-to-market value stocks and a portfolio of low book value-to-market value stocks. [Rp - Rf ] = a + B1[Rm -Rf] + B2[SMB] + B2[HML] + e

For the alpha models, one regresses the fund’s return minus the risk free rate on the factors. Significant positive (negative) performance is indicated if the intercept (the alpha coefficient) is positive (negative) and statistically significant (t-statistic greater than 1.65). Example: For fund 1 in the Excel data [Rp1 - Rf ] = 0.58 +1.02[Rm -Rf] + 0.30[SMB] - 0.05[HML] (0.7) (50.0) (9.7) (15.95) Here, alpha = 0.58 with a t-statistic of 0.7 which means that performance is not statistically significant.

Another Approach to Performance Measurement Newer methods of performance measurement try to determine whether an asset manager tends to buy assets whose prices go up more (down less) than the assets they sell. 1. Graham-Harvey, Grinblatt-Titman Measure (D #shares of stock i)t = b0 + b1(D stock i price + div.)t+1 + e 2. My Measure (D # shares of stock i)t = b0 + b1(Dstock i price + dividend)t+1 + b2(D stock i price)t + e My measure controls for stock price change at time t. Performance is positive if b1 is positive and significant.

Range of Methods to Accomplish Pooling • Financial Firms <--------------------------------> Markets • Venture Closed-End Securitization • Capital Fund Mutual Fund DRIPS • Typically, both financial firms and markets are involved in a financial product but financial firms are more involved when • Monitoring is costly. • Information is costly or selectively available (analysts). • Firms can produce claim unavailable in a market, e.g., Uplan, life-cycle funds, portfolio insurance, swaps.

Markets are more likely when • Assets to be pooled are relatively homogeneous. • Assets don’t require ongoing monitoring. • Asset liquidity is sufficiently enhanced by pooling through liquidity stripping.

Securitization Three Steps for Securitization 1. Underwriter or originator collects assets. 2. Segregates assets in a trust. 3. Writes new claims against the trust. Once these steps are performed, the originator has a minimal role, perhaps some servicing. Security-holders bear the full risk of the assets in the trust. Three Forms of Securitization - Any Asset - Most Mortgages 1. GNMA Pass-throughs - cash flows shared pro-rata. 2. CMOs - cash flows in tranches - toxic waste. 3. MBBs - bank holds mortgages - bonds sold to finance mortgages and used as collateral.

The Process of Securitization for GNMA Pass-Throughs After obtaining credit and timing insurance, the bank takes mortgages off its balance sheet and sells them as GNMA bonds through a trust to investors such as insurance companies. FHA/FMHA Credit Insurance GNMA Timing Insurance Bank Creates Mortgages Mortgages Placed in Trust GNMA Bonds Created Investors Buy Bonds

Collateralized Mortgage Obligations (CMOs) Instead of just passing along the mortgage cash flows in pro-rata portions to security-holders, CMOs have different tranches or classes of security-holders, each with a different cut of the cash flows from the underlying mortgages. The initial steps are the same as for pass-throughs. Larger total value for three classes - chicken parts. Class A - Prepay First Banks buy them GNMA Bonds GNMA Bonds Placed in Trust Class B - Prepay Second Mutual Funds buy them Class C - Prepay Last Insurance companies

Mortgage-Backed Bonds (MBBs) The bank originates $20 mortgages and holds them on its balance sheet. It issues $18 AAA-rated bonds paying a low coupon rate because they are over-collateralized by these mortgages. The rate paid on the mortgages is considerably higher so the bank earns the spread. The bank benefits from FDIC deposit insurance covering $2. Bank Earns 2% Spread Bank Creates $20 Mortgages Paying 10% Bank Issues $18 AAA MBBs Paying 8% Bondholders Get Mortgages If Bank Defaults

Why Do Banks Like to Securitize Mortgages 1. Geographic Diversification - banks sell local mortgages and buy mortgage securities from banks in other locations. 2. Liquidity - securities are easier to sell than the mortgages. 3. They earn on investment because there are no capital requirements on GNMAs but significant requirements on mortgages. Example: Suppose a bank originates mortgages paying 10%. How much does the bank earn on net? Costs: 1. Must place 10% of demand deposits used to fund mortgages on reserve at the FED earning no interest. Cost to bank: 10% of the 10% earned on mortgages equals 1%.

Example continued 2. Must pay 0.27% for FDIC deposit insurance on demand deposits. Costs bank 0.27%. 3. Capital requirements require the bank to raise equity of 4% of mortgage value to back mortgages. Assuming a 12% cost of bank equity, cost to bank is 0.5%. Overall Net Return = 10% - 1% - 0.27% - .5% = 8.23%

Assume Bank Issues GNMA Pass-Throughs 1. Bank originates mortgages at 10%. 2. Bank places mortgages in trust to sell GNMA securities that pay 9.5% coupon. 2. Bank earns 0.44% for servicing the mortgages. GNMA holders pay this and 0.06% to GNMA for its guarantee. 3. Bank buys GNMA securities earning 9.5%. 4. Bank places 10% of demand deposits funding GNMAs with FED earning no interest - Cost to bank - 0.95%. 5. Bank must pay 0.27% for FDIC deposit insurance on demand deposits. Cost to bank 0.27%. Net Return = 9.5% - 0.95% - 0.27% + 0.44% = 8.72%

Resource Transfer from Savers to Borrowers • Primary Transfers • Transfer between old (savers) and young (borrowers). • Transfer across space - e.g., London savers financed U.S. Railroads. • Question: Does the U.S. Social Security System satisfy the transfer function? How about the proposed accounts? • Other things equal, lenders often prefer lending short-term and locally in order to monitor the borrower and avoid currency risk and other risks. • Study of S&Ls 1918-1931 showed loan defaults increased from 3.8% to 7.1% to 10% as you move away from home office city by two-city increments.

Methods that Facilitate Transfer • Start with the Value of a Risky Loan • Value of = Value of - Default • Risky Loan Risk-Free Loan Insurance • The risk-free return is compensation for time transfer. • Usually, the lender provides the default insurance implicitly and charges a higher rate for more risk. • Now, third parties like insurance companies, AAA-rated banks and government agencies (FHA, FNMA, FMAC) provide some insurance which facilitates more lending.

Reasons Insurance is Widely Available for Mortgage Loans • 1. Standard Loan Applications. • 2. Standard Credit Reports - Credit Scoring. • 3. Standard Appraisal Process - Comparables. • 4. Standard Down Payments. • Better communications and financial analysis technology have made these steps cheaper to implement than in the early 1900’s when loan rates could differ by 2 - 3% across the U.S. • Loan rates still differ considerably between countries e.g., U.S. rates of 8% and Japanese rates of 3%. • Loans to small and medium-size companies are still local because of the importance of monitoring these companies.

Other Ways to Handle Default Risk • Collateral - widely used in transportation - firms like GE Capital specialize in lending on collateral. • Leasing assets - again GE Capital. • Debt ratings - specialized agencies (S&P, Moody’s) monitor large companies and issue debt ratings. Allows large firms to issue securities directly to savers. Bank’s ability to distribute debt more useful. • AAA-rated conduits sell securitized credit card and other receivables and combine over-collateralizing with credit guarantees for 10% of the security pool.