Download

1 / 18

180 likes | 364 Views

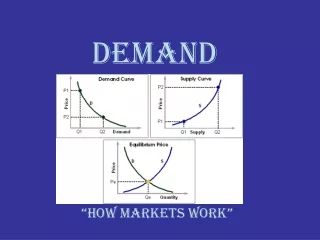

DEMAND. Demand and the Market System. Demand is our willingness and ability to buy things Varies according to price Inverse relationship – law of downward sloping demand Why? Opportunity cost less when price is low. Demand for Chocolate Cookies. Other things to consider:.

E N D

Demand and the Market System • Demand is our willingness and ability to buy things • Varies according to price • Inverse relationship – law of downward sloping demand • Why? Opportunity cost less when price is low

Other things to consider: • Change in quantity demanded = movement along the curve resulting from a change in price (memorize this!) • Price changes first (independent variable) then quantity responds • Diminishing marginal utility – the usefulness we get from something decreases as we buy more of it

Changes in Demand • What happens when other things besides price change? • (remember, price changes cause QUANTITY DEMANDED to change) • When the cause of the change is a non-price variable, the curve will shift, causing a change in demand. (memorize this!)

Example: People all get raises and can afford more cookies at every price!

What if people decide they like pretzels better than cookies? Curve will shift to the left.

Determinants of Demand • Income • Normal Goods – increase in income increases demand • Inferior Goods – increase in income decreases demand

Determinants of Demand continued • Utility – usefulness • Complementary Goods – Go together. Change in demand for one causes a change in demand for the other

Still more determinants of demand • Substitutes – increase in demand for one will decrease demand for the other • Number of buyers/size of market

Elasticity of Demand • The extent to which quantity changes in response to a new price (sensitivity to price) • Elastic Demand: • Total Expenditures (spending) on the product decrease when price increases (or vice versa) demand is elastic. • If this is $4.00, we will buy three of them (one for ourselves, one for a friend and one for our favorite teacher) 3 x $4.00 = $12.00 • If price rises to $6.00, we only buy one for ourselves. 1 x $6.00 = $6.00 Thus, total expenditures fell from $12 to $6 when price went up so demand is elastic

Inelastic Demand • When quantity responds minimally to a price change • If price is increased, total revenue (expenditures) will also increase • If gas is $2.50 a gallon, we buy 10 gallons = $25.00 • If gas goes up to $3.00 a gallon, we buy 9 gallons = $27.00

What types of good have inelastic demand? • Necessities • Goods with few substitutes • Small part of our income