Download

1 / 1

10 likes | 111 Views

7. Research questions. What makes the price Identify orders impacting the price Effect of order attributes Volume Timing What drives the market Depending on the “state” of the market, what are the order dynamics Identify trader “states” (motivations) Effect of exogenous events

E N D

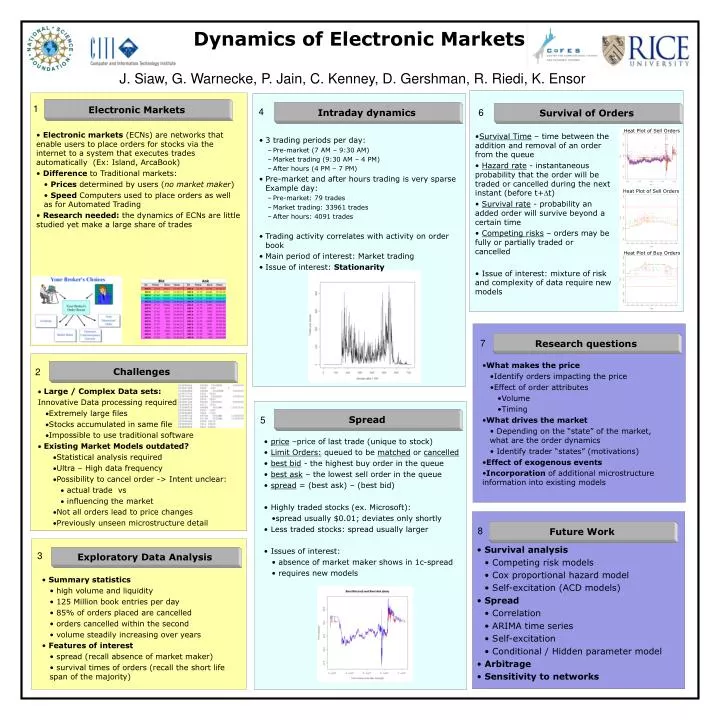

7 Research questions • What makes the price • Identify orders impacting the price • Effect of order attributes • Volume • Timing • What drives the market • Depending on the “state” of the market, what are the order dynamics • Identify trader “states” (motivations) • Effect of exogenous events • Incorporation of additional microstructure information into existing models Challenges 2 • Large / Complex Data sets: Innovative Data processing required • Extremely large files • Stocks accumulated in same file • Impossible to use traditional software • Existing Market Models outdated? • Statistical analysis required • Ultra – High data frequency • Possibility to cancel order -> Intent unclear: • actual trade vs • influencing the market • Not all orders lead to price changes • Previously unseen microstructure detail 3 Exploratory Data Analysis • Summary statistics • high volume and liquidity • 125 Million book entries per day • 85% of orders placed are cancelled • orders cancelled within the second • volume steadily increasing over years • Features of interest • spread (recall absence of market maker) • survival times of orders (recall the short life span of the majority) Dynamics of Electronic Markets J. Siaw, G. Warnecke, P. Jain, C. Kenney, D. Gershman, R. Riedi, K. Ensor 1 Electronic Markets 4 6 Intraday dynamics Survival of Orders Heat Plot of Sell Orders • Electronic markets (ECNs) are networks that enable users to place orders for stocks via the internet to a system that executes trades automatically (Ex: Island, ArcaBook) • Difference to Traditional markets: • Prices determined by users (no market maker) • Speed Computers used to place orders as well as for Automated Trading • Research needed: the dynamics of ECNs are little studied yet make a large share of trades • Survival Time – time between the addition and removal of an order from the queue • Hazard rate - instantaneous probability that the order will be traded or cancelled during the next instant (before t+t) • Survival rate - probability an added order will survive beyond a certain time • Competing risks – orders may be fully or partially traded or cancelled • Issue of interest: mixture of risk and complexity of data require new models • 3 trading periods per day: • Pre-market (7 AM – 9:30 AM) • Market trading (9:30 AM – 4 PM) • After hours (4 PM – 7 PM) • Pre-market and after hours trading is very sparse Example day: • Pre-market: 79 trades • Market trading: 33961 trades • After hours: 4091 trades • Trading activity correlates with activity on order book • Main period of interest: Market trading • Issue of interest: Stationarity Heat Plot of Sell Orders Heat Plot of Buy Orders Spread 5 • price –price of last trade (unique to stock) • Limit Orders: queued to be matched or cancelled • best bid - the highest buy order in the queue • best ask – the lowest sell order in the queue • spread = (best ask) – (best bid) • Highly traded stocks (ex. Microsoft): • spread usually $0.01; deviates only shortly • Less traded stocks: spread usually larger • Issues of interest: • absence of market maker shows in 1c-spread • requires new models 8 Future Work • Survival analysis • Competing risk models • Cox proportional hazard model • Self-excitation (ACD models) • Spread • Correlation • ARIMA time series • Self-excitation • Conditional / Hidden parameter model • Arbitrage • Sensitivity to networks