Download

1 / 46

460 likes | 613 Views

MGFOA Healthcare Reform: MA vs. Federal Cheryl Ierna Kaitlyn Kenney May 7, 2010. Overview. Massachusetts – Chapter 58 Key components of reform Results to date Patient Protection and Affordable Care Act Key components of reform Comparison to MA model Timeline for Implementation Questions.

E N D

MGFOAHealthcare Reform:MA vs. FederalCheryl IernaKaitlyn KenneyMay 7, 2010

Overview • Massachusetts – Chapter 58 • Key components of reform • Results to date • Patient Protection and Affordable Care Act • Key components of reform • Comparison to MA model • Timeline for Implementation • Questions

Massachusetts: Background and Results

MA Model for National Reform • Shared Responsibility • Individual mandate • Employer contribution • Public subsidies • Insurance Market Reform • Insurance Exchange

Responsibilities for Employers 1. Fair Share Assessment Employers with 11 or more full-time equivalent employees (FTEs) must make a “fair and reasonable” contribution to employees’ health coverage or pay state a fair share assessment of up to $295 per employee per year. 2. Section 125 Plan Requirement/Free Rider Surcharge Employers with 11 or more FTEs must establish a Section 125 Plan to give employees option to paying premiums on a pre-tax basis. Penalty (“Free Rider Surcharge”) may be assessed if such a plan is not established and employee(s) use state-funded health care services.

Government’s RoleThe Role of the Health Connector • Establish and administer Commonwealth Care, subsidized coverage for low-income, uninsured adults. • Establish and administer Commonwealth Choice, a commercial insurance “exchange”: • Standardized benefit plans and • More affordable coverage options (complements small-group/non-group market merger) • Make policy decisions as authorized by Health Care Reform Law: • Definition of Minimum Creditable Coverage (MCC) • Affordability Schedule • Conduct outreach and advertising efforts to inform public of new opportunities and responsibilities.

MA Progress Report– 5 Real Facts 1. 2.7% uninsured after 3 years 2. Of newly insured, 35% private pay 3. 98% compliance (taxpayer filings) 4. Popular approval rating (59 - 75%) 5. Commonwealth Care average trend = 4.7% through FY2010

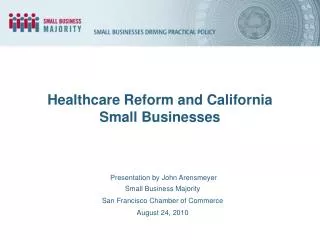

CommCare: Non-group, Employer- Premium- 46,000, 11% subsidized, paying, 96,000, 24% 52,000, 13% CommCare: MassHealth, No premium, 99,000, 24% 113,000, 28% 406,000 Newly Insured June 1, 2006 – March 31, 2009 Source: MA Division of Health Care Finance & Policy, February 2009

Improved Health • In 2007, MA saw an 8% drop in adult smokers, its largest dip in 10 years • Smoking cessation patches paid for • Visits to PCPs where smoking cessation is discussed • Statistically significant increase in age-appropriate colonoscopies • More flu shots given than ever • More people seeing a PCP, where most flu shots are administered Source: MA Department of Public Health

National Healthcare Reform: Patient Protection and Affordable Care Act (PPACA)

National Health Reform Becomes Law….. • Patient Protection and Affordable Care Act • Signed March 23, 2010 • Health Care and Education Reconciliation Act • Signed March 30, 2010 12

Implementation Has Begun • Department of Health and Human Services, headed by Secretary Kathleen Sebelius, entrusted with the responsibility for implementing many major provisions of the Act • Office of Consumer Information and Insurance Oversight, headed by Jay Angoff, responsible for ensuring compliance with the new insurance market rules such as prohibitions on rescissions, pre-existing condition exclusions, medical loss ratio rules, oversight for state-based exchanges and more 13

Major Components of PPACA • Subsidies for individuals and small employers to purchase insurance (via tax credits) • Mandate for individuals and employers • Insurance market reforms • Health insurance exchanges • Changes to Medicaid, Medicare, and many other public programs 14

Subsidies via Tax Credits: Individuals & Small Businesses

Individual Subsidies • National law provides subsidies to low and middle-income individuals to help them afford insurance through the Exchange • Amount of subsidy to be set so that premiums do not exceed a certain percentage of income 16

Individual Subsidies: Eligibility Eligibility for subsidies depends on: • Income • National reform provide subsidies up to 400% FPL (vs. 300% FPL in MA) • Availability of other coverage; not eligible if: • ESI meeting certain requirements • Medicare, Medicaid, Tricare, VA, Peace Corps, other plans TBD by Secretary, grandfathered plans, free choice voucher 17

Retiree Reinsurance • Program to reimburse eligible employer based plans for 80% of eligible claims between $15,000 and $90,000 for retirees age 55 or older and not eligible for Medicare • Both fully and self insured plans eligible • Reimbursements must be used to lower the cost of the plan • Applications available in June from HHS 19

Individual Responsibility • Law requires individuals to carry health insurance or to pay a penalty • “Minimum essential coverage” includes: • Government plan (Medicare, Medicaid, CHIP Tricare, VA, Peace Corps, others TBD by Secretary) • Employer plan • Individual plan • Grandfathered plan 21

What is a Grandfathered Plan? • Group health plans in effect on the date of the enactment are exempt from many of the health care reforms • The most significant issue surrounding grandfathered plan status is whether changes made to the plan in the future will terminate the plan’s grandfathered status 22

Individual: Exemptions *As determined by annually updated Affordability Schedule. 23

Insurance Market Reforms: Early Reforms Applies to plan years beginning 6 months after enactment: • No lifetime limits or “unreasonable” annual limits (no annual limits at all starting 2014) • Extension of dependent coverage to age 26 • No cost-sharing for preventive services (e.g., well child care and certain immunizations) 30

Insurance Market Reforms: Early Reforms (cont.) Applies to plan years beginning 6 months after enactment: • Rebate if MLR not met (sunsets at end 2013); only fully insured plans • No pre-existing condition exclusions for children (prohibited for all starting 2014) • Must have appeals process • Requirements for access to emergency, pediatric, ob/gyn and emergency care 31

Insurance Market Reforms: Reforms for 2014 • Applies to plan years beginning 1/1/2014: • Guarantee issue and renewability • No preexisting condition exclusions for any enrollee regardless of age • No discrimination based on health status • Fully insured plans with < 100 employees must provide “essential” benefits • No waiting periods over 90 days • Deductibles limited to $2,000/$4,000 and OOP limited to HSA limits for group plans 32

Insurance Market Reforms: Reforms for 2014 (cont.) • For non-group market only: • Rating can be based only on age (3:1), geography, family structure and tobacco use (1.5:1) • States can elect to apply to large employers if they allow large employers into exchange; self-insured plans exempted • Must meet specified benefits, benefit tiers, and out-of pocket limits 33

Insurance Market Reforms: Grandfathered Plans • Provisions applying to grandfathered plans: • No lifetime or annual limits • Extension of dependent coverage (only if not eligible for ESI) • No rescission • No pre-existing condition exclusions • No waiting periods over 90 days 34

Insurance Market Reforms:Collective Bargaining Agreements • Plans that were ratified prior to March 23, 2010 are not subject to reforms until the – • later of the general effective date or • the last applicable collective bargaining agreement 35

Insurance Market Reform: Implementation Issues • MA rate band regulations are narrower than national requirements • e.g., PPACA allows no more than 3:1 age band; MA market relies on 2:1 rate bands • Young Adult Plans (YAPs) would be in violation of the prohibition of annual limits • Impact of regulations on premium prices • Prohibition of lifetime limits (not currently prohibited in MCC regulations and exist in MA marketplace) • No cost-sharing for preventive services 36

State-based Exchanges: Effective 1/1/14 • Exchange functions: • Determine eligibility and administer premium subsidies • Help consumers compare and choose plans • Select which plans are to be offered through Exchange 38

Exchange 39

Exchange Creation: Issues • Eligibility criteria for participation in Exchange • Access to ESI • Employer size (may allow larger employers to participate in Exchange) • Determining citizenship • Coordination with federal government, health plans, and individuals to calculate and pay subsidies • Challenging if eligibility determination and payments are not linked through the Exchange 41

Timeline for Implementation* 2010: • High risk pools (90 days) • Early insurance reforms, such as (6 months) • Extension of dependent coverage • No lifetime limits/no “unreasonable” annual limits • No cost-sharing for preventive care • Small business tax credits • Temporary reinsurance program for early retirees • $250 rebate for Medicare Part D enrollees in the donut hole *This is not a comprehensive list. 43

Timeline for Implementation* (cont.) 2011: • Many Medicare changes • Wellness visit • Bonus payments for primary care, general surgery • Medicare Advantage transition • Start to close the donut hole • Pharmaceutical manufacturer’s fee 2013: • Eliminate deduction for Medicare Part D employer subsidy • Payroll tax for those over $200,000 ($250,000/couple) • Excise tax on medical devices 44 *This is not a comprehensive list.

Timeline for Implementation* (cont.) 2014: • Exchanges up and running • Additional insurance market reforms, such as: • No annual or lifetime limits • No pre-existing condition exclusions • Benefit mandates • Rating rules • Guaranteed issue and renewability • Subsidies available • Penalties implemented • Medicaid expanded to 133% • Health insurer fee 45 *This is not a comprehensive list.

Questions? Cheryl Ierna The Health Connector 617.933.3094 cheryl.ierna@state.ma.us 46