Download

1 / 21

210 likes | 393 Views

IRAs: Traditional vs. Roth. November 29, 2007 Michael Ruff Danielle Nick. Outline. Intro Eligibility Income Limits Contribution Limits Tax Treatments Withdrawal Guidelines Required Distributions Rollover Conclusion. IRA Background.

E N D

IRAs:Traditional vs. Roth November 29, 2007 Michael Ruff Danielle Nick

Outline • Intro • Eligibility • Income Limits • Contribution Limits • Tax Treatments • Withdrawal Guidelines • Required Distributions • Rollover • Conclusion

IRA Background • Established 1975 as part of Employment Retirement Income Act of 1974. • Originally restricted to non-pension employees • 1982 participation extended to all workers • Structured around tax deductions (i.e. Traditional IRA) • Has made few changes since (i.e. Traditional IRA)

IRA Background Continued • Roth IRA established 1998 • Chief Sponsor: Senator William V. Roth Jr. • Tax contributions not tax deductible • Has tax-free growth

Eligibility • Traditional • Virtually all inclusive for those with earned income • No income Restrictions • Age Limit for contributions 70.5 years • Roth • More restrictive • No age restriction • Income Restriction 2007:

Contribution limit • Roth and Traditional IRAs’ max contributions are identical. • Limited to the lesser of: • 100% of MAGI or • $4,000 • Catch up provision: • Must be above 50 • Limited to $1000

Contribution deductibility for Traditional IRAs • Participants involved in employer-sponsored retirement plans have limited deductibility • Deductibility depends on MAGI and marital filing status • If you (and your spouse) are not covered, you get the full deduction. Otherwise:

Tax Treatments • Traditional • Tax deduction • Pre-tax income contributed • Earnings grow tax-deferred • Roth • No tax deduction • After-tax income contribution • Earnings grow tax-free

Tax Treatments • Professor Sinow made $90,000 in 2007 • He has 2 choices: Traditional • $4000 contribution • His taxable income for 2007 is $86,000 • Upon withdrawal, taxes due on principal and earnings Roth • $4000 contribution • His taxable income for 2007 is $90,000 • Upon withdrawal, no taxes due

Withdrawal Guidelines:Similarities • Both share these similarities: • Minimum age: 59.5 • Withdrawal before 59.5 = 10% tax penalty • Penalty is in addition to any taxes owed upon regular withdrawal • Certain exceptions for early withdrawals • First time home-buyer • Qualified education expenses • Hardship expenses

Withdrawal Guidelines:Exceptions • If first-time homebuyer, • No 10% penalty for early withdrawal • $10,000 for individuals • $20,000 for married couples • Must use funds within 120 days • Qualified expenses include: • Buying, building, re-building costs • Settlement, financing, and closing costs

Withdrawal Guidelines:Exceptions • If you have qualified higher education costs, • No penalty for early withdrawal • No $ limitations • Qualified expenses: • Used by individual, his/her spouse, child, or grandchild • Used at IRS-approved college, university, vocational, or post-secondary facility • Used for tuition, fees, books, or supplies • If enrolled at least half time, room and board, too

Withdrawal Guidelines:Exceptions • If you have qualified hardship expenses, • No penalty for early withdrawal • Qualified expenses: • Un-reimbursed medical expenses • “prolonged and expensive costs” • must exceed 7.5% of Adj. Gross Income (AGI) • Medical insurance premiums • Must be unemployed for 12 months

Withdrawal Guidelines:Special Roth Treatment • One catch for Roth IRAs • Must have held the account for at least 5 years • If so: not subject to taxes • If not: must pay taxes on the withdrawn accumulated earnings • Still no 10% penalty • Applies to the early withdrawal exceptions already mentioned

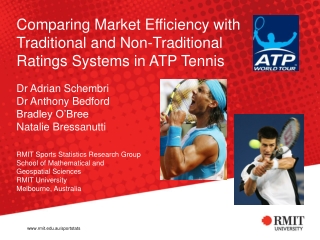

Traditional Required Distributions start at age 70.5 Can delay 1st payment until April 1 of the next year But, essentially make 2 distributions in one year IRS provides minimum distribution tables based on: Age Expected distribution period Roth NONE! If you want, you don’t ever have to make distributions Because gov’t doesn’t collect taxes on distributions, it doesn’t care when you take the money out Required DistributionDifferences

Minimum Required Distribution Table for Traditional IRA Source: Bankrate.com

Minimum Required Distribution for Traditional IRA Example: • Professor Sinow turns 70.5 on Jan. 1, 2008 • He has $100,000 in a Traditional IRA • He has a MRD: • In the amount of $3,650 • For the 2008 tax year OR • He has a MRD: • In the amount of $3,650 between 1/1/09 & 4/1/09 • In the amount of $3,636 • Both withdrawals are part of the 2009 tax year

Minimum Required Distribution for Traditional IRA • If investor does not take the MRD…penalty • Penalty equal to 50% of the difference between MRD and actual distribution • Example: • Professor Sinow’s MRD is equal to $5,000 for the year • If he only takes a $2,000 distribution • He has a penalty of $1,500 taken from IRA’s subsequent balance.

RolloverTraditional into Roth • Traditional IRA holders can convert to Roth • Single & married taxpayers: • Must have AGI of less than $100,000 to qualify for the rollover • AGI limit is for conversion year • Conversion years are not related • Pay taxes on the principal and interest rolled over into the Roth account • Rollover amount is unlimited

ConclusionWhich is better? • It depends! • Age (how long account will grow) • Tax rates • Rate when you contribute • Rate when you withdraw • Positives and negatives with both Determine which is best for you? http://www.finance.cch.com/sohoApplets/RothvsRegular.asp