Download

1 / 28

280 likes | 372 Views

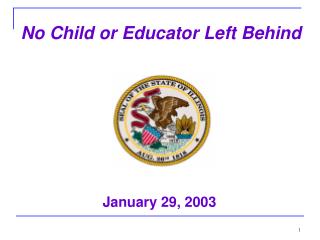

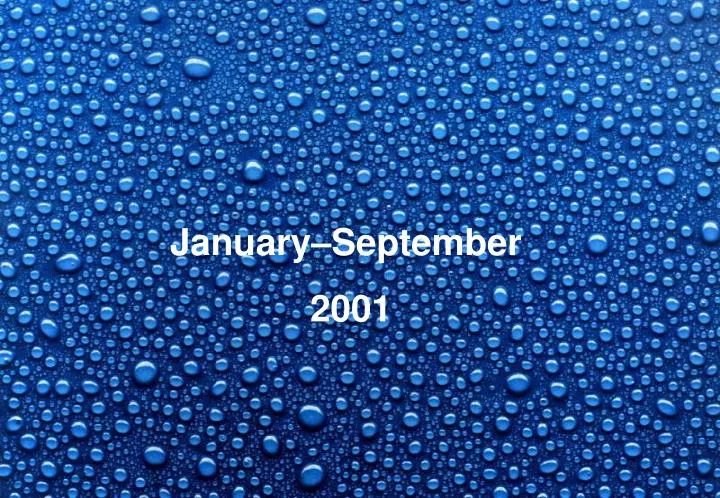

January–September 2001. Rolling four quarters. SEKm. SEKm. IPO. 4 000. 400. 3 500. 350. 3 000. 300. Order intake. 2 500. 250. EBIT. 2 000. 200. Net sales. 1 500. 150. 1 000. 100. 500. 50. 0. 0. Q4. Q1. Q2. Q3. Q4. Q1. Q2. Q3. Q4. Q1. Q2. Q4. Q1. Q2. Q3.

E N D

January–September 2001

Rolling four quarters SEKm SEKm IPO 4 000 400 3 500 350 3 000 300 Order intake 2 500 250 EBIT 2 000 200 Net sales 1 500 150 1 000 100 500 50 0 0 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 1995 1996 1997 1998 1999 2000 2001 Excluding Alecta (SPP) surplus refund of SEK 15 million in Q3, 2000.

Market Development Jan–Sept 2001 Continued good demand in “non-cyclical” industries. • Europe • Strong demand for MCS • Strong market in poultry • Soft market in general • Americas • Softening demand in general • Good development for MCS following hurricane Allison in Texas • Weak poultry market • Asia • Recession in Japan

Cyclical customers grew Others 23% MCS 33% Pharma 4% 6% 6% Electronics 6% 11% 18% After Sales Utilities Food

Pharma Food DH: 40% of Munters, 2000 Preservation Dehumidification

Dehumidification • Strong Net Sales in Americas • Gaining market shares in Americas • Soft order situation, Zeol declining as expected • Flat development in Europe

MCS: 30% of Munters, 2000 Moisture Control Services Water Damage Restoration

MCS • Hurricane Allison in Houston, Texas • Orders USD 4 M Q3 • Net Sales USD 7 M Q3 • Growth and margin improvements continue • Increased Net Sales but low margins in Australia • One acquisition in France in Q3 • Customer consolidation continues

HC: 30% of Munters 2000 HumiCool Utilities Poultry Comfort Cooling

HumiCool • Non-US AgHort business growing fast • US AgHort market very slow • Gas turbine business good • HVAC demand soft • Personnel reduction

Munters’ strategy for growth Open new geographical markets Grow the Service business Global roll-out of existing applications Integration forward Underlying growth

Global organization Net Sales SEK 3.8 billion Employees 2 600 Sales Manufacturing and Sales

Net sales by Region Net sales Jan-Sept 2000 SEK 2 247 million Net sales Jan-Sept 2001 SEK 2 830 million Asia +28% Asia 11% 10% Europe Europe +18% 52% 48% 38% 41% Americas Americas +35%

Net sales by Product Area Net sales Jan-Sept 2000 SEK 2 247 million Net sales Jan-Sept 2001 SEK 2 830 million HumiCool HumiCool +14% DH DH +21% 31% 28% 39% 38% 30% 34% MCS MCS +44%

July - September 2001 • Order intake growth 25% • Currency adjusted 13% • Net sales growth 28% • Currency adjusted 16% • Operating earnings growth 31% • Operating margin 9.8% • Strong development in MCS in all regions • One acquisition, MCS Europe • Low margin in Europe. New line control system DH and very good L.Y. HumiCool • Strong L.Y. Japan

Financial overview July-Sept 2001 2000 2001 SEK m Q1 Q2 Q3 Q4 Q1 Q2 Q3 Growth 784 982 25% Order intake 791 884 863 960 974 799 1 020 28% Net sales 707 741 932 851 960 76 100 31% EBIT 51 65 114 72 92 1) 9.6 9,8 Margin % 7.3 8.7 12.2 8.5 9.6 42 59 41% Net earnings 29 37 66 41 55 1) 19 72 277% Op. cash flow 63 77 103 47 105 1) Excluding Alecta (SPP) surplus refund of SEK 15 million in Q3, 2000.

Regional analysis July-Sept 2001 Net sales Growth EBIT margin Europe 476 17% 6.7% Americas 449 44% 13.3% Asia 109 15% 12.1% Total Group 1 020 28% 9.8%

January–September 2001 • Order intake growth 19% • Currency adjusted 8% • Net sales growth 26% • Currency adjusted 15% • Operating earnings growth 38% • Operating margin 9.4% • Four small acquisitions

Financial overview Jan-Sept 2001 Growth January-Sept 1997 1998 1999 2000 2001 01/00 01/97 SEK m 2 459 2 916 Order intake 1 709 1 763 1 916 19% 15% 2 247 2 830 Net sales 1 594 1 745 1 863 26% 15% 192 265 EBIT 121 132 154 38% 22% 1) 8.6 9.4 Margin % 7.6 7.6 8.3 107 155 Net earnings 69 77 93 44% 21% 1) 160 225 Op. cash flow 97 107 181 41% 23% 1) Excluding Alecta (SPP) surplus refund of SEK 15 million in Q3, 2000.

Regional analysis Jan–Sept 2001 Net sales Growth EBIT margin Europe 1 388 18% 7.7% Americas 1 180 35% 12.1% Asia 304 28% 11.8% Total Group 2 830 26% 9.4%

Currency and Acquisition Effects Currency effect Net Sales - Jan-Sept 2000: 2 247 + 222 +10% Net Sales from acquired units +41 +2% Organic Growth +320 +14% Net Sales - Jan-Sept 2001: 2 830 +26%

Key ratios Jan–Sept 2001 2001 2000 Return on Capital Employed (%) 1)32.8 31.4 Interest coverage ratio (times) 15.7 11.7 Net debt (SEK m) 322 349 Net debt/Equity ratio 0.36 0.48 Earnings per share (SEK) 2)6.19 4.35 1) Rolling 12 month 2) Before dilution effects on full exercise of warrants corresponding to maximum 1.8% of the share capital

Orders are up again, currency effect is significant SEK m +25% +10% +21% 1 000 1994 +25% 1995 900 1996 1997 800 1998 1999 700 2000 2001 600 500 400 300 200 100 0 Q1 Q2 Q3 Q4

Net sales SEK m 1 100 +28% 1994 +30% 1 000 1995 +27% 1996 +20% 900 1997 800 1998 1999 700 2000 600 2001 500 400 300 200 100 0 Q1 Q2 Q3 Q4

Backlog SEK m 700 +14% +45% 1994 +5% 650 +56% 1995 600 1996 550 1997 +43% 500 1998 1999 450 2000 400 2001 350 300 250 200 150 100 50 0 Q1 Q2 Q3 Q4

EBIT improvements SEK m 120 +37% 1994 110 1995 +32% 100 1996 +42% 1997 90 1998 80 +41% 1999 70 2000 2001 60 50 40 30 20 10 0 Q1 Q2 Q3 Q4

Summary • One Strong brand – Munters • Strong organic growth • Technical leadership • Global presence • Large service operations • Large installed base • High market share in defined niches • Customers in growing and non-cyclical areas • Capital light