Download

1 / 24

260 likes | 607 Views

Investment Proposal for Prospective Investors By Prof. JJ Asongu US: 5382 Guilford Rd, Rockford, IL 61107, USA Cameroon: P.O. Box 189, Molyko, Buea, SW, Cameroon Email: asongu@charteredltd.com ; Website: http://www.charteredltd.com.

E N D

Investment Proposal for Prospective Investors By Prof. JJ Asongu US: 5382 Guilford Rd, Rockford, IL 61107, USA Cameroon: P.O. Box 189, Molyko, Buea, SW, Cameroon Email: asongu@charteredltd.com; Website: http://www.charteredltd.com

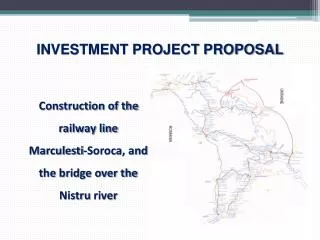

Map of Cameroon & Other CEMAC Countries – Equatorial Guinea, Gabon, Congo, Central African Republic, & Chad

Overview • Executive Summary • Business Description • Marketing • Finances • Management • Conclusion

Executive Summary • Chartered Financial Assistance (CFA), Savings & Loans Cooperative Society, Ltd, is a micro-finance institution (MFI) currently approved to operate in Cameroon • Headquartered in Buea, CFA was founded in 2009 by Prof. JJ Asongu and a few others • The company currently operates only in the Southwest Region, but it plans to open three more branches that should extend the company to three Regions including the West and Northwest • CFA has an aggressive growth strategy, with the intention of extending to all 10 Regions of Cameroon by 2012 and to all six CEMAC countries by 2015

Executive Summary (Continue) • There is a market for CFA and other similar MFIs considering that less than 5% of the Cameroonian population is served by commercial banks • There are only about 11 commercial banks in the country, and most of them do not target the rural, self-employed, & less affluent populations (these constitute our target market) • There are about 500 MFIs in the country, but many of them operate as non-profits (NGOs), have just one location, & are not professionally managed • There is a tremendous opportunity for MFIs in general and CFA in particular because it doesn’t have many of the shortcomings of other MFIs

Executive Summary (Continue) • Our marketing strategy is designed to allow us to concentrate our limited resources on the greatest opportunities to increase sales and achieve a sustainable competitive advantage • CFA’s marketing strategy focuses on customer satisfaction • We also offer a wide array of services, many of which are not offered by either commercial banks or other MFIs • CFA will provide these products and services to clients all across the country, whereas other commercial banks and MFIs tend to concentrate in particular markets

Executive Summary (Continue) • MFIs in Cameroon have a low entry threshold – unlike commercial banks that require a capital of over $20 million, MFIs need just over $100,000.00 to go operational • Sensing the opportunity to get into the market before the regulations are tightened, CFA was registered after barely raising this minimum capital • CFA is fast gaining the approval of the public and attracting savings of over $10,000.00 monthly • The company has an immediate need of over $200,000.00 to implement its strategy, otherwise it must embrace a less aggressive growth strategy • This money will be realized by the sale of 800 shares at $250.00 (about 100,000 Frs) each, making the total of $200,000.00 • CFA has a total of 2,000 shares, thus it plans to sell a 40% stake in the company

Executive Summary (Continue) • The management and staff of the company is young but well educated and fairly experienced • All employees have a business, economics, or accounting degree, with at least one year of prior MFI management experience • The current Board of Directors is well experienced in the banking/MFI industry, and the founder is a professor of economics, business, and accounting in the US, and plans to return to Cameroon to personally run the company once he raises enough capital • Considering the business opportunity here, the marketing strategy, finances, and management of CFA, the company is poised for success especially if it raises the required $200,000.00 in additional capital

Business Description • Chartered Financial Assistance (CFA) Savings and Loans Cooperative Society, Ltd, is a leading micro-financial institution (MFI) in Cameroon • Founded in 2009, it is headquartered in Buea, the English-speaking SW Region and a growing academic and commercial city • Its location is strategic, considering that it provides the needed human resources essential for our success • All savings with CFA are secured and insured by a third-party insurance company • Thanks to our state-of-the-art technology, CFA plans to offer services that are unsurpassed by any other financial institution in the country

Business Description (Continue) CFA History • CFA was founded in 2009 by Prof. JJ Asongu and a few others including its current managers • The company is headquartered in Buea, Southwest Region • There are plans to open more branches in the Northwest, Southwest, and the French-speaking West Regions • It is projected that by December 2010, CFA will be operational in three Regions out of the 10 Regions in Cameroon • It intends to spread to all 10 Regions of Cameroon by 2012 and to begin going international to the central African (CEMAC) countries in 2013 and to be established in all by 2015 • It also plans to meet the conditions for becoming a commercial bank by 2015

Business Description (Continue) Mission Statement • To provide the highest level of personal financial services in a friendly and professional manner • To encourage thrift, savings, and the wise use of credit • To increase the knowledge and ability of our members to manage and control their financial well-being • To provide sound financial management in order to maintain earnings for our continued growth • To provide our employees with a challenging and rewarding career

Business Description (Continue) Vision Statement • To achieve sustainable growth, we have established a vision with clear goals: • Profit: Maximizing return to members while being mindful of our overall responsibilities. • People: Being a great place to work where people are inspired to be the best they can be. • Portfolio: Bringing to our members a portfolio of services that anticipate and satisfy their desires and needs. • Partners: Nurturing a winning network of partners and building mutual loyalty. • Planet: Being a responsible global citizen that makes a difference.

Marketing Marketing Research • There are only about 11 banks in Cameroon, serving a population of about 19 million, and the situation is even worse in other CEMAC countries – Gabon, Equatorial Guinea, Chad, Central African Republic, and Congo • According to a World Bank study, these 11 commercial banks serve less than 5% of the Cameroonian population and in some CEMAC countries it is as low as 2% • The threshold for becoming a commercial bank was recently raised and by 2014, both new and existing commercial banks will need a capital of over $20 million to be in business • These 11 commercial banks in Cameroon charge very high deposits just to open an account, with the most affordable requiring over $100.00 • Most Cameroonians are therefore not able to open a bank account and worse still these banks are located exclusively in the urban areas, with most of them operating in less than five of the country’s 10 Regions

Marketing (Continue) Marketing Research (Continue) • Most of the banks do not target the rural, self-employed, & less affluent populations • With very few commercial banks in the CEMAC region, MFIs have recently been flourishing and some of the current commercial banks started as MFIs • Cameroon has many MFIs, about 500, but most of them have only a single location and there is hardly any one with a national presence • Many of the MFIs operate as non-profits (NGOs) and as such do not apply market strategies in their operations • Many MFIs are also run by inexperienced staff with little or no training in the areas of banking and finance • There is a tremendous opportunity for MFIs in general and CFA in particular because it doesn’t have many of the shortcomings of other MFIs

Marketing (Continue) Marketing Strategy • Our marketing strategy is designed to allow us to concentrate our limited resources on the greatest opportunities to increase sales and achieve a sustainable competitive advantage • CFA’s marketing strategy focuses on customer satisfaction; with an important aspect of it being convenience • We plan to be conveniently located in all 10 Regions of Cameroon and enhance our presence through mobile banking, as well as other services such as online banking, ATMs, etc. • We also offer a wide array of services, many of which are not offered by either commercial banks or other MFIs • An example of such unique offering will be Individual Retirement Accounts (IRA) • CFA will provide these products and services to clients all across the country, whereas other commercial banks and MFIs tend to concentrate in particular markets

Marketing (Continue) CFA SWOT Analysis

Marketing (Continue) Target Market • Young people looking for state of the art products and services e.g. ATMs, online banking, debit cards, etc. • Travelers looking for convenient way of carrying money locally and internationally • Corporate and organizational clients • Individuals, including civil servants, private sector employees, and the self-employed • Small business owners, including real estate investors, contractors, etc • Those who have been ignored by the traditional banking sector in the country

Marketing (Continue) Why CFA Will Succeed: • The strengths of CFA far outweigh its weaknesses • The greatest weakness is its lack of sufficient capital at the moment, but when we raise the $200,000.00, we’ll overcome the other weaknesses • There are many opportunities, which the company can capitalize on to become a highly successful financial institution • With more capital, CFA will be able to implement its aggressive growth strategy and it’s nationwide presence in Cameroon will help it implement its money transfer business • Countries like Equatorial Guinea and Chad have very few MFIs and we should take advantage of it • The banking sector in the six CEMAC countries has been harmonized and we can function in all of them, providing us a further incentive for growth

Finances Current Situation • The start a fully licensed Category One MFI in Cameroon, one needs a capital of over $100,000.00 (50 million Frs) • However, with proof of about $35,000.00, a company will be licensed and they have one year to raise the remainder • Commercial banks require a capital of over $20 million to go operational and there have been rumors about raising the threshold for MFIs • Sensing the opportunity to get into the market before the regulations are tightened, CFA was registered after barely raising this minimum capital • More than half of this capital has since been spent on items like lease, salaries, computers and software, office equipment, utility bills etc

Finances (Continue) Immediate Capital Needs • The company has an immediate need of at least $200,000.00 to implement its strategy • This money will be realized by the sale of 800 shares at $250.00 (about 100,000 Frs) each, making the total of $200,000.00 • CFA has a total of 2,000 shares, thus it plans to sell a 40% stake in the company • CFA is fast gaining the approval of the public and attracting savings of over $10,000.00 monthly • Without this capital infusion, the company will continue to survive and grow, but it will be forced to embrace a less aggressive growth strategy

Management Board of Directors • Chair: Prof. JJ Asongu, PhD, DBA, CIO Cert, FABPP (President/CEO of IRGB, Rockford, IL, USA) • Vice Chair: Mr. Callistus Fonkem (Vice President of Bomaka Credit Union, Buea, Cameroon) • Secretary: Ms. Hannah Mokoko, BA, MA, Vice Principal of GHS Bokwango, Buea, Cameroon • Treasurer: Mr. Stanley A. Fomenky, BSc Management (General Manager of CFA) • Mr. George Y. Wirnkar, BPhil (Former Manager, Amity Bank, Limbe, Cameroon) • Mr. George Fontom, BSc Accounting (Credit & Risk Manager, Union Bank of Cameroon, Douala, Cameroon) • Mr. Nicholas Asongu Jingwa, BA, MA (President, Lewoh Village Bank, Lewoh, Cameroon) • Mr. Louis N. Nkembi, MSc (President/CEO, ERUDEF, Buea, Cameroon)

Management (Continue) Managers & Staff • Chief Executive Officer: Prof. JJ Asongu (US-based Professor of Economics, Business, & Accounting; Will relocate to Cameroon once he raises the $200,000.00) • General Manager: Mr. Stanley A. Fomenky, BSc Mgmt (3 years experience in banking & finance; founded a credit union) • Manager Buea Branch: Mr. John Chabajong, BSc Econs (1 year experience) • Manager Kumba Branch: Mr. James O. Eyambe, BSc Econs (4 years, Former Credit Union Manager) • Manager Muyuka Branch: Mr. Lionel Mesumbe (2 years experience) • CFA has seven other employees, all of which have at least a Bachelor of Science degree and some experience

Conclusion • The management and staff of the company is young but well educated and fairly experienced • All managers have a business, economics, or accounting degree, with at least one year of prior MFI management experience • The current Board of Directors is well experienced in the banking/MFI industry, and the founder is a professor of economics, business, and accounting in the US, and plans to return to Cameroon to personally run the company once he raises enough capital • Considering the business opportunity here, the marketing strategy, finances, and management of CFA, the company is poised for success especially if it raises the required $200,000.00 in additional capital

Conclusion (Continue) What’s In It For You? • Opportunity to invest in a new, but growing company, as the window of opportunity will close once we raise the needed capital • Opportunity to be a player in a highly profitable and growing industry • With the Cameroon economy growing at over 4%, it makes sense to invest here as opposed to the US where there is still a recession • CFA projects that it will begin to make a profit as early as next year, thus investors can begin seeing a return on their investment • Africa presents many opportunities and this is a golden opportunity to become a major African player