Download

1 / 42

420 likes | 574 Views

A Presentation On The Salient Features Of The Companies Bill, 2009. September 26, 2009. Introduction.

E N D

A Presentation On The Salient Features Of The Companies Bill, 2009. September 26, 2009

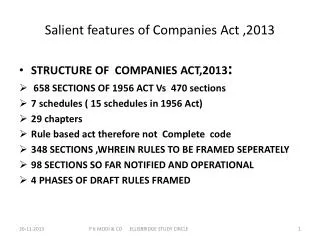

Introduction • A liberal regulatory set-up for corporate entities is on the anvil with the Cabinet approving the introduction of a new Companies Bill (“the Bill”) that will replace the existing rigid and voluminous Companies Act of 1956 (“the Act”). • The Companies Bill, 2009, has been introduced in the last session of Parliament in October and once enacted, will replace the Companies Act, 1956. • The Bill proposes to halve the Sections from 650 in the existing Act to around 426. • The Companies Bill 2009 is an effort to usher in self-regulation in corporate affairs with disclosures and accountability, and to substitute government control over internal corporate processes and decisions by shareholder control.

Salient Features of the Bill • One Person Company (OPC) allowed, more stringent regime for Not-For-Profit Firms (Section 25 companies). • Transition of Companies from private to public and vice versa to be easier. • Restrictions on number of partners in partnership firms, banking firms relaxed.( minimum 2 and no ceiling on maximum partners) • Insider trading by Company Directors/ Key Managerial Personnel (KMP) to be an offence with criminal liability. • Class action suits/ Derivative suits by shareholder associations, groups against Companies allowed. • Appointment of minimum 33% independent directors on board. • No issue of shares on discount. • Provides for a single forum approval process for M&As. • Dividend can be claimed by investors even after 7 years. • Use of technology such as tele and video conferencing, e-mail, digital signatures etc. in various situations.

Speedy Incorporation • A Majority of the recommendations made by Sir JJ Irani have been implemented; e.g; • e-governance and on line filing, • limited interfacing with ROC officials, • correct disclosure based process of incorporation, • Reduced time for response; • No requirement to obtain “COB Certificate”, • No minimum capital required for companies. • Rational Classification of Companies; small, OPCs, control based etc. • Provision of ‘printing’ of memorandum and articles dispensed with. • Process of incorporation simplified and compacted in few sections.

Incorporation Process • Clause 3:A company may be formed for any lawful purpose by any – (a) seven or more persons, where the company to be formed is to be a public company, or (b) two or more persons, where the company to be formed is to be a private company, or (c) one person, where the company to be formed is to be a One Person Company. • A company formed under sub-section (l) may be either:- (a) a company limited by shares, or (b) a company limited by guarantee, or ( c) an unlimited company.

Incorporation Process Clause 5. Memorandum of a company shall state – • name of the company; with last words as “Private Company”; Public Company; or OPC Limited; • Place of Registered Office’ • Objects; • the liability of members of the company, whether limited or unlimited . • Name of the Company not to be identical to any other company. • Not to be registered with a name giving impression that it has Govt. patronage. • Name Availability application to be made in the form to be prescribed. Registrar to reserve the name for 2 months and maximum 4 months. Memorandum to be in the form as may be prescribed.

Incorporation Process Clause 6. The articles shall also contain such matters, as may be prescribed. Company free to provide Additional matters in he Articles. -articles may contain provisions for entrenchment to the effect that specified provisions of the articles may be altered only if conditions or procedures as that are more restrictive than those applicable in the case of a special resolution, are met or complied with. • The Central Government may prescribe model articles for different types of companies . • (sections 12,13,14,20,26,27,28,29 of the 1956 Act dealing with incorporation have been reduced and clubbed into Clauses 3,5,6 and 7 of the Bill). Section 25 company has been dealt with in section 4 of the Bill.

Incorporation Process • Clause 7(1) file with the Registrar within whose jurisdiction the registered office of a company is proposed to be situated, following documents and information for registration, namely:- (i) memorandum and articles of the company duly signed by all the subscribers to the memorandum in such manner as may be prescribed; (ii) declaration by an advocate, a Chartered Accountant, Cost Accountant or Company Secretary, engaged in the formation of the company, or by a person named in the articles as a director, manager or Secretary that all provisions have been complied with; (iii) an affidavit from each of the subscribers to the memorandum and from persons named as first directors that no conviction of any offence in connection with the promotion, formation or management of any company, or that he has not been found guilty of any breach of duty to any company under this Act .

Incorporation Process Affidavit to state that that all the documents filed with the Registrar for registration of the company contain information that is correct and complete and true to the best of his knowledge and belief; (iv) the particulars of name, including surname or family name, residential address, nationality and such other particulars of every subscriber to the memorandum along with proof of identity, as may be prescribed, and in the case of a subscriber being a company, such particulars as may be prescribed; (v) the particulars of the persons mentioned in the articles as first directors of the company, their names, including surnames or family names, the Director Identification Number, residential address, nationality and such other particulars including proof of identity as may be prescribed;

Incorporation Process (vi) the particulars of the interests of the persons mentioned in the articles as first directors of the company in other firms or bodies corporate along with their consent to act as directors of the company in such form and manner as may be prescribed. • Upon satisfaction of the above conditions, Registrar to issue certificate of incorporation and CIN. • Submission of false information or making of false declarations for incorporating company made punishable with a imprisonment of one year and a minimum fine of Rs.25,000 and maximum of Rs. One lakh. Promoters, first directors and other persons making false declarations are liable to be punished. (Clause 7(5)) • Without prejudice to above, Tribunal has ben given sweeping powers to pass orders of managing company by directing changes in M/A, making liability unlimited, removal of name and winding up.

Incorporation…. • Clause 8: Effect of Registration • Clause 9: Effect of M/A &A/A. • Clause 10: Commencement of Business-No certificate required; However, a company once formed cannot do business unless a declaration by a director or subscriber that every subscriber has paid full value of shares and verification of the Registered Office has been filed in the prescribed manner with the Registrar. • Clause 11: Registered off ice of the Company including shifting thereof; • Clause 12 & 13: Alteration of M/A and A/A including change of name. • Clause 15: Rectification of name of Company (section 21/22).

One Person Company (OPC) • Currently, minimum number of persons required to incorporate a Company is 2 in the case of a Private Company and 7 in the case of a Public Company. • Clause 3 read with 2(zzk) of the Bill provides for a new entity in the form of a One-Person Company (OPC). This is with the intention of encouraging individual entrepreneurs to operate and contribute effectively in the economic domain. • The J.J. Irani Report proposes for an OPC with the following characteristics:- a) OPC may be registered as a Private Company with one member and may also have at least one director; b) Adequate safeguards in case of death/disability of the sole person should be provided through appointment of another individual as Nominee Director. On the demise of the original director, the nominee director will manage the affairs of the Company till the date of transmission of shares to legal heirs of the demised member. c) Letters ‘OPC’ to be suffixed with the name of One Person Companies to distinguish it from other Companies.

One Person Company-Background & Concept • increasing use of information technology emergence of the service sector; • the entrepreneurial capabilities of the people are given an outlet for participation in economic activity; • Such economic activity may take place through the creation of an economic person in the form of a company called OPC; • OPC is an enterprise that runs with extremely few human, financial and infrastructural resources while offering products or services to a large customer base;

Back to Saloman vs. Saloman • Classic OPC=Salomon v. Salomon & Co. was decided by the House of Lords in 1897. It was basically the first case to uphold the concept that a corporation is an independent legal entity. • Mr Solomon was a Victorian bootmaker. He sold the assets of his business to a company Solomon & Co Ltd. of which he was the sole (or virtually the sole shareholder). He continued to trade as a bootmaker in his own name and went bust. His creditors tried to sieze the assets of the business (now owned by Solomon & Co Ltd. The decision of the court was that Solomon & Co Ltd formed a separate legal entity from Mr Solomon. Mr Solomon's debts were not the debts of Solomon & Co. Ltd. The rule is that a properly formed limited liability company is a legal entity in its own right.

Relaxation of limit to have Number of Partners • Section 11 of the 1956 Act provides for a maximum of 20 partners in general business and 10 partners in case of banking business. Section 11 is proposed to be deleted in the 2008 Bill as per JJI committee recommendation. • New Section 422 added. Provides for a maximum of 100 persons or association of persons or a partnership who can come together and do business only by forming a company under the Bill. Exceptions are HUF and professional partnership under special Acts. • It has been provided in the Bill, with the intention to promote the setting up of specialized firms or businesses, to relax the restrictions limiting the number of partners in partnership firms, banking Companies etc. with no ceiling as to professions regulated by Special Acts. • Clause 6 of the LLP Bill provides that Every limited liability partnership shall have at least two partners.

Relaxation of limit to have Number of Partners • If at any time the number of partners of a limited liability partnership is reduced below two and the limited liability partnership carries on business for more than six months while the number is so reduced, the person, who is the only partner of the limited liability partnership during the time that it so carries on business after those six months and has the knowledge of the fact that it is carrying on business with him alone, shall be liable personally for the obligations of the limited liability partnership incurred during that period.

Duties of Directors • To act in accordance with Articles; • To act in good faith and promote objects of the Company; • To exercise duties with reasonable care, skill & diligence, • Avoid conflict of interest situations; • Not to attempt or achieve undue gain or advantage for himself or relatives or partners; • Not to assign his office. In case the duties are violated not only there is a levy of fine but also “class action/Derivative action” can be launched.

Class Action/ Derivative Suits • Under the 1956 Act, no shareholder’s association can take legal action against fraudulent action by Companies. • The Bill enables Shareholders Associations/ a Group of shareholders to take legal action in case of any fraudulent action on the part of the Company and to take part in Investor Protection Activities and Class Action Suits. • In case of fraud on the minority by wrongdoers, who are in control and prevent the Company itself bringing an action in its own name, derivative actions in respect of such wrong non-ratifiable decisions, have been allowed by courts. Such derivative actions are brought out by shareholder /(s) on behalf of the company, and not in their personal capacity /(ies), in respect of wrong done to the Company. • Similarly the principle of “Class/Representative Action” by one shareholder on behalf of one or more of the shareholders of the same kind have been allowed by courts on the grounds of persons having same locus standi.

Class Action-Understanding the Meaning of: • class action was developed in the 20th century as a way of managing complex, multiparty litigation. It may be traced to the “bill of peace,” a proceeding that originated in England's equity courts in the 17th century. The bill of peace was used when the parties to a dispute were too numerous to be easily managed and when all parties shared a common interest in the issues. • It is a lawsuit brought by one or more plaintiffs on behalf of a large group of others who have a common interest. • An action where an individual represents a group in a court claim. The judgment from the suit is for all the members of the group (class). • If the court permits the class action, all members must receive notice of the action and must be given an opportunity to exclude themselves. Members who do not exclude themselves are bound by the Judgment, whether favorable or not. • often done when shareholders launch a lawsuit, mainly because it would be too expensive for each individual shareholder to launch their own law suit. • a way to resolve multiparty disputes quickly and effectively.

Understanding a Class Action.. • Clause 216 enables shareholders/creditors to seek an injunctive/declaratory relief against wrongdoer directors-form of “Equitable Remedy only”. • Who can file: Any one or more members or class of members or one or more creditors or any class of creditors. • When can file: if they are of the opinion that the management or control of the affairs of the company are being conducted in a manner prejudicial to the interests of the company or its members or creditors.

Understanding a Class Action.. • For what orders:for seeking all or any of the following orders: (i) to restrain the company from committing an act which is ultra vires the articles or memorandum of the company; (ii)to restrain the company from committing breach of any provision of the company’s memorandum or articles; (iii)to declare a resolution altering the memorandum or articles of the company as void if the resolution was passed by suppression of material facts or obtained by misstatement to the members or creditors; (iv) to restrain the company and its directors from acting on such resolution;

Understanding a Class Action.. (v) to restrain the company from doing an act which is contrary to the provisions of this Act or any other law for the time being in force; (vi) to restrain the company from taking action contrary to any resolution passed by the members. • Any order passed by the Tribunal shall be binding on the company and all its members and creditors. • Fine: Max 25 Lakhs for Company and OinD 3 years + Fine. • Examples of Class Actions in US: civil rights cases, antitrust cases to combat consumer fraud, price fixing, and other commercial abuses, mass tort cases, where numerous plaintiffs are injured at the hands of a single defendant;

Understanding a Class Action.. • eg; Union carbide caseor Bhopal Gas, Dalkon shield (an intrauterine device); Agent Orange (a herbicide used as a defoliant in the Vietnam War), and of asbestos insulation has involved class action suits. • Principle:" all persons materially interested, either as plaintiffs or defendants in the subject matter of a bill ought to be made parties to the suit, however numerous they may be," so that the court could "make a complete decree between the parties [and] prevent future litigation by taking away the necessity of a multiplicity of suits" (West v. Randall, 29 F. Cas. 718, 2 (C.C.R.I. Mason) 181 [1820] [No. 17, 424]). “ • Idea: Common issues that could have similar outcomes did not have to be tried piecemeal in separate actions, thus saving the courts and the litigants time and money.

Understanding a Class Action.. • Requirement: must be met, e.g., the class must be so large or dispersed that actual joinder of all individuals would be impractical; there must be questions of law and fact common to all members, and these must outweigh any individual questions; and the named parties must adequately represent the interests of their class. Certain forms of notice to members of the class, e.g., by newspaper or broadcast publication or by mail, are also required.

Shareholder Derivative Actions-Foss v Harbottle Rule • Majority rule in company law is a long established principle. It provides an equitable solution to determining many disputes, and culminated in the Foss v Harbottle rule. • It states that damage done to the company by outsiders may only be remedied by corporate action. As the court’s are reluctant to interfere in internal management. • The Courts have used this to justify not interfering in a company’s internal affairs, giving the majority power to prevent a member litigating when a breach of the articles has occurred. This helps prevent “futile actions” and “companies being torn apart by litigation”. • Majorities can also ratify acts that are Intra Vires by ordinary resolution, a power capable of abuse, but this may be beneficial to the company.

Shareholder Derivative Actions-Foss v Harbottle Rule • These rules are generally termed the “exceptions” to the Foss v Harbottle doctrine. • any act that is Ultra Vires the company, either as prohibited by the memorandum or statute, or illegal, is incapable of being ratified by any majority. • a “fraud on the minority” would relax the rule that a majority must approve litigation because, without this, the fraudulent parties could possibly prevent an action. This would apply, especially, to shareholder directors who abused their power and then ratify their acts. • “special minorities” exception. The automatic barrier to suit has been set at the level of an ordinary majority of the general meeting. It will thus have no application when the rules of company law require some higher majority, or where the matter is such that it is inappropriate to refer it to an ordinary majority.

Shareholder Derivative Actions-Foss v Harbottle Rule • remedy of minority shareholders, allowing any member to petition the court on the grounds that the company’s affairs are being run in an unfairly prejudicial manner. Such actions do not need to be oppressive1, and the court is empowered to make whatever order it thinks fit to remedy the matter. Thus, so long as a petition is well founded, this can be used without the consent of the majority to allow relief. • A shareholder derivative suit is a lawsuit instigated by a shareholder of a corporation, not on the shareholder's own behalf, but on behalf of the corporation. The shareholder brings an action in the name of the corporation against the parties allegedly causing harm to the corporation. Often derivative suits are brought against officers or directors of a corporation for violations of fiduciary duties owed to the shareholders vis-a-vis the corporation. Any proceeds of a successful action are awarded to the corporation. • In the U.K., an action brought by a minority shareholder is liable to be defeated by the Foss v. Harbottle principle. But exceptions have been evolved to the principle laid down in that case primary among them being "the ultra vires exception" and the "fraud on minority" exception.

Shareholder Derivative Action • Typical Requirements: • (a) Shareholder must have standing to sue, or they must own the shares at the time the act or omission occurred. • (b) Shareholder must make a written demand on the corporation so that they may take action. • (c) Burden of proof is on the shareholder unless a majority of the directors have a personal stake in the dispute. • (d) the alleged wrong or breach of duty is one that is incapable of being ratified by a simple majority of the embers;and • (e) the alleged wrondoers are in control of the company,so that the company,which is the “proper Claimant” cannot claim by itself.

Single Forum For M&As • Section 390 to 396 (Chapter V) of the Act deals with compromise, arrangements and reconstructions which include mergers and acquisitions which requires approval of High Court and other regulatory authorities like RBI, BIFR etc. • The Bill provides for a single forum for approval of mergers and acquisitions along with the concept of deemed approval in certain situations. • This would reduce the time period involved in mergers and acquisitions.

Mergers & Aquisitions • Clause 201– this clause corresponds to section 391; • powers to Tribunal to make order on the application of the company or any creditor or member or in case of winding-up, of liquidator for the proposed compromise or arrangements including debt restructuring, etc., between company, its creditors and members ; • application by affidavit shall disclose all material facts relating to company, reduction of share capital scheme of corporate debt restructuring; • arrangement includes a reorganization of the company’s share capital by the consolidation of shares of different class or by the division of shares into shares of different classes, or by both of those methods.

Mergers & Aquisitions • An application made under sub-section (1) shall disclose to the Tribunal by affidavit – (a) all material facts relating to the company, such as the latest financial position of the company, the latest auditor’s report on the accounts of the company and the pendency of any investigation oro proceedings against the company; (b) reduction of share capital of the company, if any, included in the compromise or arrangement; (c) any scheme of corporate debt restructuring consented to by not less than seventy-five percent of the secured creditors in value, including – (i) a creditor’s responsibility statement, (ii) safeguards for the protection of other secured and unsecured creditors,

Mergers & Aquisitions (iii) report by the auditor that the fund requirements of the company after the corporate debt restructuring as approved shall conform to the liquidity test based upon the estimates provided to them by the Board, (iv) where the company proposes to adopt the corporate debt restructuring guidelines specified by the Reserve Bank of India, a statement to that effect, and (v) a valuation report in respect of the shares and the property and all assets, tangible and intangible, movable and immovable, of the company by a registered valuer.

Mergers & Aquisitions • a notice of such meeting shall be sent to all the creditors or class of creditors and to all the members or class of members and the debenture holders of the company, either individually or by an advertisement, which shall be accompanied by a statement disclosing the details of the compromise or arrangement, the valuation report, if any, and explaining their effect on creditors, members and the debenture holders and the effect of the compromise or arrangement on any material interests of the directors of the company or the debenture trustees, and such other matters as may be prescribed. • A notice under sub-section (3) shall also indicate that the persons to whom the notice is sent shall intimate in writing their consent to the adoption of the compromise or arrangement within one month from the date of receipt of such notice:

Mergers & Aquisitions • Provided that any objection to the compromise or arrangement shall be made only by persons holding not less than ten per cent of the shareholding or having outstanding debt amounting to not less than five per cent of the total outstanding debt as per the latest audited financial statement. • A notice under sub-section (3) along with all the documents in such form as may be prescribed shall also be sent to the Central Government, the Reserve Bank of India, the Securities and Exchange Board, the Registrar, the respective stock exchanges, the Official Liquidator, the Competition Commission of India established under sub-section (1) of section of the Competition Act, 2002, if necessary. • Such Notice shall require that representations, if any, to be made by them shall be made within one month from the date of receipt of such notice, failing which, it shall be presumed that they have no representations to make on the proposals.

Mergers & Aquisitions • at a meeting held in pursuance of this section, a majority representing three-fourths in value of the creditors, or class of creditors or members or class of members, as the case may be, present and voting in person or by proxy or by postal ballot, agree to any compromise or arrangement and if such compromise or arrangement is sanctioned by the Tribunal by an order, the same shall be binding on the company, all the creditors, or class thereof. • order made by the Tribunal shall provide for all or any of the following matters, namely:- (i) conversion of preferential shares into equity shares: such preference shareholders shall be given an option to either obtain arrears of dividend in cash or accept equity shares equal to the value of the dividend payable ; • the protection of any class of creditors;

Mergers & Aquisitions • If the compromise or arrangement is agreed to by the creditors, any proceedings pending before the BIFR shall abate; • No compromise or arrangement under this section shall include any buy-back of securities as is provided under section 61; • Any compromise or arrangement may include takeover offer made in such manner as may be prescribed. “takeover offer” means an offer to acquire all the shares in a company . • Clause 202 –corresponds to section 392 of 1956 Act; provide powers to Tribunal to enforce compromise or arrangements with creditors and members;

Mergers & Aquisitions • Clause 203. – This clause corresponds to section 394 of the 1956 Act; provides powers to Tribunal to order for holding meeting of the creditors or the members and to make orders on the proposed reconstruction, merger and amalgamation of companies ; • manner and procedure in which the meeting so ordered by the Tribunal be held ; • Orders for transfer of any property or liability, that property or liability shall be transferred to and become the liabilities of the transferee company and any arrangement. • Clause 204. –new clause provides for merger between two small companies or between a holding company and its wholly owned subsidiary company by giving a notice of the proposed scheme inviting comments or objections by both the transferor and the transferee company.

Mergers & Aquisitions • The scheme to be approved by the members at a general meeting by passing a special resolution and by three-fourths in value of the creditors of respective companies ; • Transferee Company to file a copy of the approved scheme with the Registrar and the Official Liquidator; • If Registrar is of the opinion that such a scheme not in public interest or in interest of the creditors, he may file an application before the Tribunal stating his objections and requesting to consider the scheme for reconstruction merger or amalgamation, etc., under clause 203. • The Tribunal may direct accordingly or it may confirm the scheme by passing such order as it deem fit.

Mergers & Aquisitions • The transferor company shall be deemed to be dissolved on registration of the scheme. • Clause 205. –new clause provides the mode of merger between registered companies and companies incorporated in the jurisdictions of such countries as notified from time to time by the Central Government by mutual agreement. • a foreign company may merge or amalgamate into a company or vice versa and the terms and conditions of the scheme of merger. • may provide for the payment of consideration to the shareholders of the merging company in cash or partly in cash or partly in Indian Depository Receipts.

Mergers & Acquisitions • Clause 207. –corresponds to section 395 of the 1956 Act provides the procedure and manner in which the registered holder of at least 90 per cent shares of a company shall notify the company of their intention to buy the remaining equity shares of minority shareholders, by virtue of an amalgamation, share exchange, conversion of securities, etc., provision for valuation of shares have been provided by a registered valuer. • Clause 208. amalgamation of two or more companies in public interest by passing an order to be notified in the Official Gazette. • Clause 210. –corresponds to section 396A of 1956 Act, provides that no company which has been amalgamated or whose shares has been acquired by another company to dispose of its books of accounts and papers without the prior permission of the Central Government. The Government may appoint a person to examine books and papers to ascertain whether they contain any evidence of commission of offence in connection with promotion, formation, management, etc., of the company.

Conclusion Apart from the above discussed salient features, the Companies Bill, 2009 contains other novel and path-breaking provisions which when passed, would apart from streamlining the current legislation and procedure, also enable the corporate sector in India to operate in a much liberalized regulatory environment that fosters entrepreneurship, investment and growth.

Thank You For Viewing The End