Download

1 / 3

30 likes | 52 Views

DIFC Licensing categories are defined as the type of licenses required for the type of business that the applicant wishes to engage in.

E N D

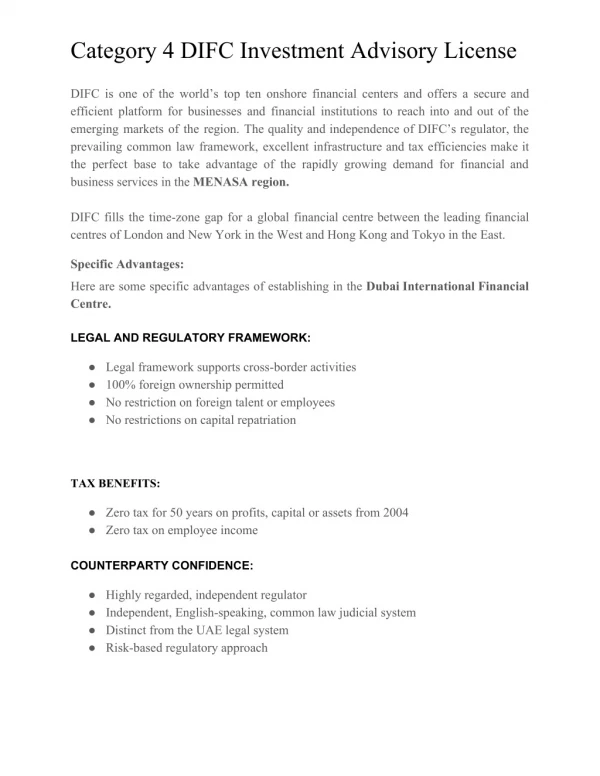

DIFC Licensing categories DIFC is one of the world’s top ten onshore financial centers and offers a secure and efficient platform for businesses and financial institutions to reach into and out of the emerging markets of the region. The quality and independence of DIFC’s regulator, the prevailing common law framework, excellent infrastructure, and tax efficiencies make it the perfect base to take advantage of the rapidly growing demand for financial and business services in the MENASA region. DIFC fills the time-zone gap for a global financial center between the leading financial centers of London and New York in the West and Hong Kong and Tokyo in the East. Why setup a financial services firm in the DIFC? The DIFC is a leading financial hub in the region. Besides offering a wide range of financial service activities, the center also provides an integrated environment and world-class standard of living. It is well regarded in the international community as well. There exist opportunities for startups as well. The recent focus on fintech led to the DIFC Fintech Hive initiative, that serves as an accelerator for fintech firms to test their products and pitch it to prospective investors. Sarwa (https://www.sarwa.co) is one such success story. Specific Advantages Here are some specific advantages of establishing in the Dubai International Financial Centre. FRAMEWORK ● The legal framework supports cross-border activities ● 100% foreign ownership permitted, no restrictions on capital repatriation ● No restriction on foreign employees TAX EFFICIENCIES ● Zero tax for 50 years on profits, capital or assets ● Zero tax on personal income

CONFIDENCE ● Highly regarded, independent regulator ● Independent, English-speaking, common law judicial system ● Distinct from the UAE civil courts ● Risk-based regulatory approach ECOSYSTEM ● High prominence in deal making in the region ● Concentration of international financial institutions ● World-class regional and international professional services ● The leading fund domicile in the region GEOGRAPHIC EPICENTRE ● GCC Management offices, holding companies and family offices are located closer to the assets they own or manage ● The UAE plays a central role in growing global trade, between Asia and Africa on one side and the West on the other ● Well-positioned to harness the potential of emerging markets. DIFC Licensing categories Firms interested in doing business in DIFC based on Financial Services are required to submit applications to the Dubai Financial Services Authority, or DFSA.The type of business that the applicant wishes to engage in defines the category of Licence that is required. For example, a firm undertaking low-risk activities such as advising or arranging will require a Category 4 Licence, while a discretionary portfolio manager will require a Category 3C Licence. An STP broker, dealing on a matched principle basis will require a Category 3A Licence, whereas a market maker or provider of credit provider will require a Category 2 Licence. Full-fledged banks, that accept deposits, will come under a Category 1 License. DIFC Capital requirements The category of the license will determine the amount of capital required. The base capital requirement for a Category 4 firm is $10,000. This rises to $500,000 for a Category 3 firm, $2 million for a Category 2 firm and $10m for a Category 1 firm.Capital waivers may be available to the DIFC branch of a regulated financial institution having its head office in a recognized regulatory jurisdiction.

Activities are grouped into 5 main categories, as below: Category 1 – Banks Base Capital – US$ 10 million Activities – Accepting Deposits, Managing a PSIAu Category 2 – Market maker, a provider of credit Base Capital – US$ 2 million Activities – Dealing in Investments as Principal, Providing Credit Category 3A – Brokerage Base Capital – US$ 500,000 Activities – Dealing in Investments as Matched Principal, Dealing in Investments as Agent Category 3B – Custodian Base Capital – US$ 4 million Activities – Providing Custody for a Fund, Acting as Trustee for a Fund Category 3C – Asset Manager, Fund Manager Base Capital – US$ 500,000 Base Capital for EF, QIF Managers – US$ 70,000 Base Capital for Operating a Crowdfunding Platform – US$ 140,000 Activities – Managing Assets, Managing a Collective Investment Fund, Providing Custody, Managing a PSIAr, Providing Trust Services Category 4 – Investment Advisor, Insurance advisor Base Capital – US$ 10,000 Activities – Arranging Deals in Investments, Arranging Credit and Advising on Credit, Advising on Financial Products, Arranging Custody, Insurance Intermediation, Insurance Management, Operating an ATS, Providing Fund Administration, Providing Trust Services, Operating a Crowdfunding Platform Category 5 – Islamic Business Base Capital – US$ 5 million Activities – Operating an Islamic Business