Download

1 / 13

140 likes | 255 Views

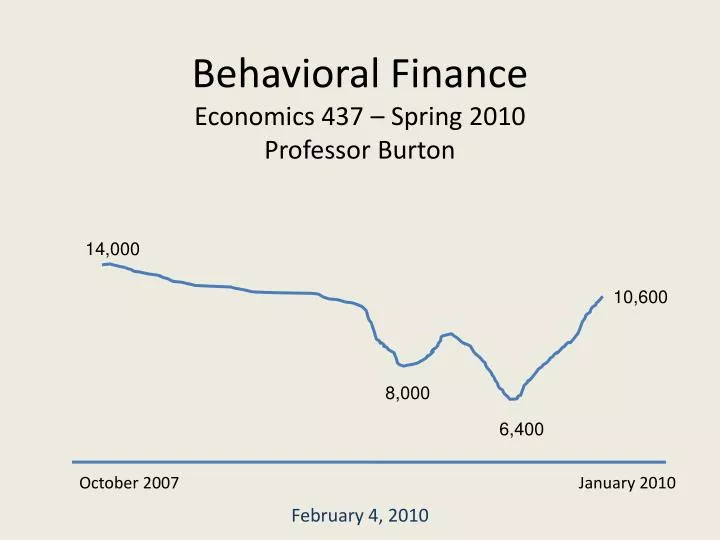

Behavioral Finance Economics 437 – Spring 2010 Professor Burton. 14,000. 10,600. 8,000. 6,400. October 2007 January 2010. Wrapping Up The Shleifer Etal Article. Agents Arbitrageurs

E N D

Behavioral FinanceEconomics 437 – Spring 2010Professor Burton 14,000 10,600 8,000 6,400 October 2007 January 2010 February 4, 2010

Wrapping Up The Shleifer Etal Article • Agents • Arbitrageurs • Noise Traders • Assets • Safe asset • Risky asset • Two Big Questions • Can price of the two assets by different? • Do the arbitrageurs always win? February 4, 2010

What is an “arbitrage trader” • Arbitrage traders “correctly” perceive the true distribution of pt. There is “systematic” error in estimation of future price, pt • But, arbitrageurs face risk unrelated to the “true” distribution of pt • If there were no “noise traders,” then there would be no variance in the price of the risky asset…..but, there are noise traders, hence the risky asset is a risky asset

The Main Issues • What happens in equilbrium • Undetermined • Some forces make pt > 1, some forces push pt < 1, result is indeterminant • Who makes more profit, arbitrageurs or noise traders? • Depends • But, it is perfectly possible for arbitrageurs to make more! • Survival?

The Price of the Risky Asset February 4, 2010

When Do Noise Traders Profit More Than Arbitrageurs? • Noise traders can earn more than arbitrageurs when ρ* is positive. (Meaning when noise traders are systematically too optimistic) • Why? • Because they relatively more of the risky asset than the arbitrageurs • But, if ρ* is too large, noise traders will not earn more than arbitrageurs • The more risk averse everyone is (higher λ in the utility function, the wider the range of values of ρ for which noise traders do better than arbitrageurs February 4, 2010

Expected Excess Total Return of Noise Traders February 4, 2010

Black on “Noise” • Black strong believer in noise and noise traders in particular • They lose money according to him (though they may make money for a short while) • Prices are “efficient” if they are within a factor of 2 of “correct” value • Actual prices should have higher volatility than values because of noise

Hirshleifer, Etal on Feedback • Three dates • Eight kinds of investors • Early and late • Informed and uninformed • Rational and irrational • Mainly rational and irrational (noise) traders • One firm with equity shares • Trades at period 1 and period 2 • Payoff in period 3

Hirshleifer Payoff Function In period 3, payoff is: F = θ + ε + δ εreally plays no role, so lets simplify to: F = θ + δ

Hirshleifer Payoff Function F = θ + δ θ is the true payoff distribution without feedback θ is the feedback parameter, which depends upon prices P1, P2

So what happens in Hirshleifer Etal • Early irrational, but informed, traders benefit because later irrational traders buy and the early traders “know it” • Sometimes early informed traders benefit as well • Late irrational traders get smashed

The End February 4, 2010