Download

1 / 18

190 likes | 365 Views

Capital Allocation Line Part II. Improving Client’s Position. A client asks your advice about her investments. She has invested $70,000 in a Mosaic mutual fund and $10,000 in risk-free bonds. She asks you whether she should re-allocate her assets. Mosaic fund Expected return: 15%

E N D

Improving Client’s Position • A client asks your advice about her investments. She has invested $70,000 in a Mosaic mutual fund and $10,000 in risk-free bonds. She asks you whether she should re-allocate her assets. • Mosaic fund • Expected return: 15% • Standard deviation: 30%. • Vanguard Fund • Expected return: 12% • Standard deviation: 16%. • Assume now that borrowing and lending rates differ. In particular, the borrowing rate equals 11% and the lending rate equals 7%.

Improving Client’s Position • Question 1: What is the expected return and the standard deviation of her current portfolio? • The expected return is: E(r)=(7/8)*(0.15) + (1/8)*(0.07) = 14% (stat rule 1) • The standard deviation is: Stdev(r)=(7/8)*0.30 = 0.2625 (stat rule 2)

Different Borrowing and Lending Rates • Question 2 - Assuming now that borrowing and lending rates differ: • Can you find a portfolio with same total risk but higher expected return? • In this case, we can’t simply turn to the Sharpe Ratio, because there are two risk-free rates.

Different Borrowing and Lending Rates • To find a portfolio with same total risk, use stat rule 2: 0.2625=w(.16) w=1.64 (1-w)=-0.64 • Expected return • Which risk free rate do you use? • Since my weight in Vanguard is above 1, this means I am borrowing. • E[r]=1.64*0.12-0.64*0.11 = 0.1264 < 0.14

Different Borrowing and Lending Rates • Now, if we switch to Vanguard we are worse off if we create a portfolio with same total risk as the client’s current portfolio. • Your client is better of sticking with her Mosaic fund.

Different Borrowing and Lending Rates • Question 3 - Assuming now that borrowing and lending rates differ: • Can you find a portfolio with same expected return but lower total risk? • In this case, we can’t simply turn to the Sharpe Ratio, because there are two risk-free rates.

Different Borrowing and Lending Rates • To find a portfolio with same E[r], use stat rule 1: • Which risk free rate do you use? • I need to get an expected return of 14% using Vangaurd which I expect to only earn 12%. • To get a higher expected return, I must borrow.

Different Borrowing and Lending Rates • What is the total risk of this portfolio? • Use stat rule 2: • sp=3*0.16=0.48>0.2625 • Again, your client is better of sticking with her Mosaic fund.

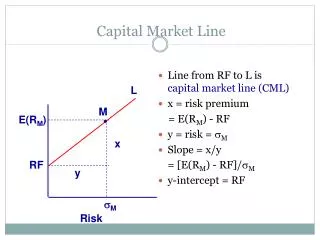

Different Borrowing and Lending Rates • What do CAL line look like when borrowing and lending rates differ? • See Excel Spreadsheet

Classifying Markets • General Types of Markets • Direct Search • Brokered • Dealer • Auction • Financial Markets • Primary • Secondary

Role of Investment Banks in Primary Markets • Advise the firm regarding the terms on which it should attempt to sell the securities • Preliminary registration statement must be filed by SEC • red herring • once approved: prospectus • When prospectus is approved, price is announced. • Banks buys securities from the issuing company at public offering price less a spread and then resell to public.

Road Shows • I-bank escorts leaders of firm around to meet big institutional investors to generate interest in the offering. • Shares are allocated according to interest • If a firm wishes to get shares, it must indicate its optimism.

Two IPO Puzzles • IPO stocks experience on average large returns on the first day of trading. • Very strong result. • IPO stocks under-perform over the next five years. • Not sure I believe this one. • Others do.

Money Left on Table Money Left on Table = (Closing Price – Opening Price)*(Shares Issued)

IPO First Day Returns • Firms depend on the road show to get information from big investors about how the market might receive the issue. • Often adjust the opening price according to the level of interest expressed during road show. • To entice big investors to truthfully reveal information • Allocate more shares to those who express stronger interest • Offer the shares at a “discount”