Download

1 / 8

110 likes | 356 Views

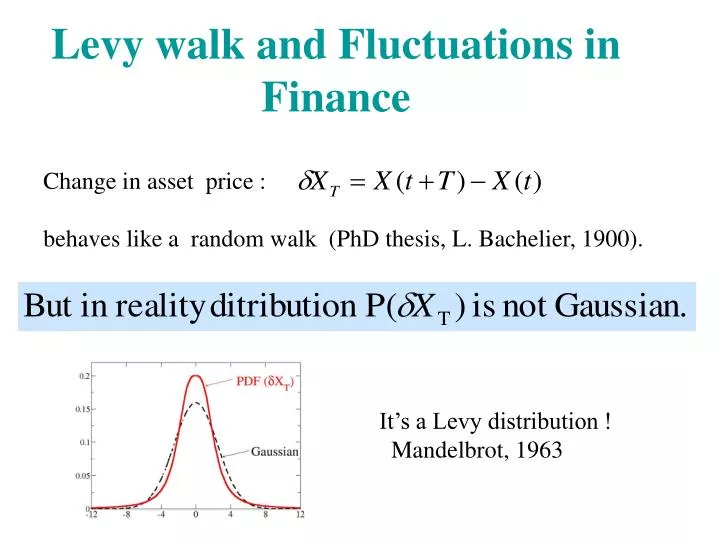

Levy walk and Fluctuations in Finance. Change in asset price : behaves like a random walk (PhD thesis, L. Bachelier, 1900). It’s a Levy distribution ! Mandelbrot, 1963. Levy distribution has fat tails ! ( Sometimes markets do crash !! )

E N D

Levy walk and Fluctuations in Finance Change in asset price : behaves like a random walk (PhD thesis, L. Bachelier, 1900). It’s a Levy distribution ! Mandelbrot, 1963

Levy distribution has fat tails! ( Sometimes markets do crash !! ) Self similar with respect to sampling time windowT . (ie, whether data is collected every five minutes or every month). Log PDF vs logX Gaussian

Market fluctuations are almost unpredictable ie, correlation time very short (Hence Markovian , like random walk ! ) Otherwise you could predict the market and easily become millionaire.

Mass Transport and DiffusionRandom Walk Diffusion( a slow process <x2> = 2Dt )Diffusion can be enhanced or slowed down by flows or potentials. Tracers in turbulent flows. <x2> ~ t 3 (Richardson’s law) drawing: Leonardo da Vinci,1500

Potential barriers can suppress diffusion. (a non-equilibrium problem) The famous Kramers formula (1940) Application: rate of chemical reactions, lifetime of weak bonds

Transport inside a cell (size ~ 10 m) Random walkers transport cargo through highways !! The cell has network of filaments (microtubules) along which the the motor proteins (random walkers) move with their cargo. But unbiased random walk cannot generate directed movement. Need help from potentials V(x,t)