Download

1 / 11

130 likes | 728 Views

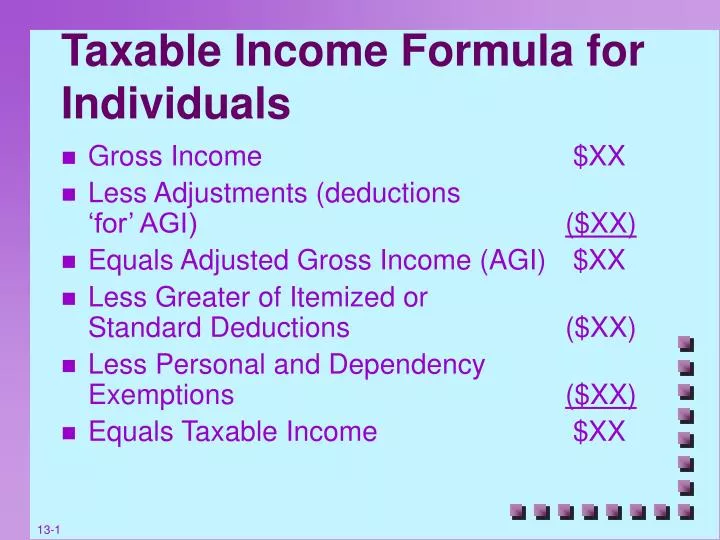

Taxable Income Formula for Individuals. Gross Income $XX Less Adjustments (deductions ‘for’ AGI) ($XX) Equals Adjusted Gross Income (AGI) $XX Less Greater of Itemized or Standard Deductions ($XX) Less Personal and Dependency Exemptions ($XX) Equals Taxable Income $XX.

E N D

Taxable Income Formula for Individuals • Gross Income $XX • Less Adjustments (deductions‘for’ AGI) ($XX) • Equals Adjusted Gross Income (AGI) $XX • Less Greater of Itemized orStandard Deductions ($XX) • Less Personal and DependencyExemptions ($XX) • Equals Taxable Income $XX

Filing Status • Married filing jointly - legally married at year end, and widows and widowers for year of death • Widows/widowers with dependents qualify as surviving spouse for 2 years following year of death of spouse, and continue to use MFJ rates and standard deduction amount • Married filing separately - married individuals choosing to file separate returns • Head-of-household - Single individual maintaining household for a dependent relative, not qualifying as a surviving spouse • Single - everyone else

Standard Deduction • Indexed for inflation • Depends on filing status – 2003 amounts • Single - $4,750 • Married filing jointly and surviving spouse - $7,950 • Married filing separately - $3,975 • Head of household - $7,000 • Additional Standard deduction if over 65 or blind • $1,150 for single and head of household • $950 for all others

Personal & Dependency Exemptions • Artificial deductions, representing an amount of income not taxed that varies with the number of persons supported by that income • 2003 exemption - $3,050 per person • exemption allowed for taxpayer, spouse (on a joint return) and supported dependents

Personal & Dependency Exemptions continued • ‘Support’ requires: • 50% of financial support provided by taxpayer • Gross income less than exemption • Waived for child who is a minor or full-time student under 24 • Family member or resident in taxpayer’s home • Phase-out for high income taxpayers • MFJ threshold AGI of $209,350 (2003) • H-of-H threshold $174,400 • Single threshold $139,500 • MFS threshold $104,625

Other Issues • Phase-out of itemized deductions • Higher income taxpayers are limited in their ability to use itemized deductions • Total deductions reduced by 3% of AGI in excess of threshold amount ($139,500 in 2003) • Medical, investment interest, gambling and personal casualty loss deductions not subject to reduction • Reduction cannot exceed 80% of total remaining itemized deductions • Motivation for phase-out? • Impact of phase-out on marginal tax rate?

Other Issues continued • Why does it matter if a deduction is ‘for’ or ‘from’ AGI? • AGI used to calculate limits such as medical expense and miscellaneous itemized deductions • If taxpayer claims the standard deduction, any benefit of a ‘for’ deduction inadvertently treated as a ‘from’ deduction is lost

Other Issues continued • Marriage penalty • Federal income tax system is not marriage neutral • Why does a marriage penalty occur? • MFJ standard deduction amount is not 2 times Single amount • MFJ rate brackets are not 2 times Single brackets • Do all married taxpayers experience a marriage penalty? Which taxpayers would receive a marriage benefit?

Computation of Tax Liability • Regular tax liability on ordinary income, calculated using rate schedules based on filing status • Special tax rates on capital gains • Individual tax credits: • Child credit - $600 per child, phased out for higher-income taxpayers • Dependent care credit • Earned income credit • Excess payroll tax withholding

Individual Alternative Minimum Tax • Basic approach similar to corporate AMT • standard deduction and exemptions are AMT adjustments • Individual AMT exemption amounts: • MFJ - $49,000 (phased out if AMTI > $150,000) • MFS - $24,500 (phased out if AMTI > $75,000) • Single - $35,750 (phased out if AMTI > $112,500) • Individual AMT rates: • 26% on AMTI up to $175,000 • 28% on excess

Payment and Filing Requirements • Most individuals meet payment requirements via payroll withholding • Estimated payments may be required for taxpayers with substantial non-payroll income • Safe harbor payment requirements: • Form 1040 required by 15th day of 4th month following close of taxable year • Automatic 4-month extension possible; can request additional 2-month extension