Download

1 / 38

380 likes | 551 Views

2. 1. Acquiring Inventory:. What items to include?General rule: (1) held for sale and (2) complete and unrestricted ownership.Consignments: belong to consignor, ownership not based on physical possession.Goods in transitFOB Shipping Point: belongs to the purchaser while in transit (once invent

E N D

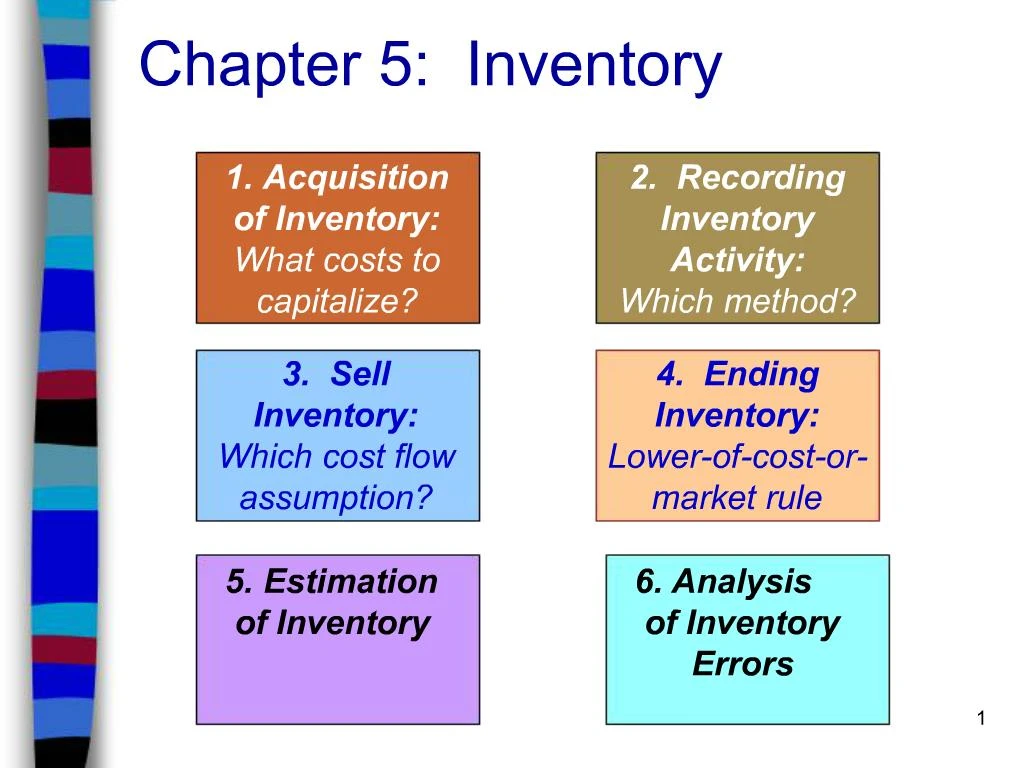

1. 1 Chapter 5: Inventory

2. 2 1. Acquiring Inventory: What items to include?

General rule: (1) held for sale and (2) complete and unrestricted ownership.

Consignments: belong to consignor, ownership not based on physical possession.

Goods in transit

FOB Shipping Point: belongs to the purchaser while in transit (once inventory leaves seller�s facilities).

FOB Destination: belongs to seller while in transit (until inventory reaches purchaser�s facilities).

Note: FOB does not indicate who pays the freight. This is indicated by �prepaid� or �collect�.

3. 3 Class Problem: Houston Corporation had the following inventory transactions in transit at 12/31/02. Indicate whether the inventory would be included in Houston�s ending inventory at December 31, 2002.

1. Purchased inventory �FOB Shipping Point�; shipped on December 30.

YES

2. Sold inventory �FOB Shipping Point�; shipped on December 30.

NO

4. 4 Class Problem - continued: Houston Corporation had the following inventory transactions in transit at 12/31/02. Indicate whether the inventory would be included in Houston�s ending inventory at December 31, 2002.

3. Sold inventory �FOB Destination�; shipped on December 30.

YES

4. Purchased inventory �FOB Destination�; shipped on December 30:

NO

5. 5 1. Acquiring inventory - contd. What costs to attach? General rule: all costs associated with purchase or manufacture.

Freight-in (transportation-in) adds to the cost of purchases.

Purchase returns reduce the cost of purchases (contra) for returned inventory.

Purchase allowances reduce the cost of purchases (contra) for reduced prices due to damage or errors.

Purchase discounts from early cash payments (contra) reduce the cost of purchases.

Purchase discounts recorded using gross or net method.

Gross method more popular, but net method is theoretically correct way of reporting of economic events.

Illustration after discussion of periodic system.

6. 6 2. Perpetual or Periodic Method Perpetual

Up-to-date record in inventory account.

Cost of goods sold computed for each sale.

Periodic

Inventory purchases are recorded as incurred.

Inventory and cost of goods sold determined at the end of each period through physical count.

Costs and benefits

Perpetual requires more bookkeeping but provides more useful information.

General application: Periodic used for general ledger entries; perpetual used for units.

7. 7 Illustration Periodic System

Purchase of 10 units @ $8:

Inventory (or Purchases) 80

Cash 80

Sale of 7 units @ $12:

Cash 84

Sales 84

(no COGS entry until the end of the period)

December 31 to recognize EI and COGS. Note that there is no BI; EI physical count is 2 cases, valued at $8 each = $16, so COGS is for 8 cases @$8 each.:

BI + P - EI = COGS, so

0 + 80 - 16 = COGS = 64)

COGS 64

Inventory (or BI and Purch.) 64

8. 8 Periodic System Note that the periodic system is illustrated in later sections of the text, using the specific components of COGS for the journal entries.

These components include:

Purchases (+)

Freight-in (+)

Purchase discounts (-)

Purchase returns (-)

Purchase allowances (-)

Also, when these accounts are used during the period, the balance in the Inventory account remains as the beginning inventory until the AJE at the end of the period is posted.

Now work Ex. 5-24.

9. 9 Periodic System If the component accounts are used to record inventory activity during the accounting period, then the AJE at the end of the period transfers the balances in the component accounts to EI and COGS. The following formulas represent the activity:

BI + Purchases (net) - EI = COGS or

BI + Purchases (net) = EI + COGS

Note that Purchases (net) =

Purchases

+ Freight-in

- Purchase Discounts

- Purchase Returns

- Purchase Allowances

10. 10 This AJE under periodic system follows the formula for COGS: COGS xx

Ending Inventory xx

Purch. Discounts xx

Purch. Returns xx

Purch. Allowances xx

Freight-in xx

Purchases xx

Beginning inventory xx

Note that this journal entry closes out BI and Net Purchases, and transfers the balances to EI and COGS. The EI balance will go to the balance sheet, and the COGS balance will go to the income statement.

11. 11 Purchase Discounts - Gross Method Assume purchase of $100 on account on 6/1/00, terms 2/15, n/30.

GJE to record purchase on 6/1/00:

Purchases 100

Accounts Payable 100

GJE to record payment, if on or before 6/16/00:

Accounts Payable 100

Purchase Discounts 2

Cash 98

GJE to record payment, if after 6/16/00:

Accounts Payable 100

Cash 100

(Purch Disc. is contra to Purchases; part of COGS calc.)

12. 12 Purchase Discounts - Net Method Assume purchase of $100 on account on 6/1/00, terms 2/15, n/30.

GJE to record purchase on 6/1/00:

Purchases 98

Accounts Payable 98

GJE to record payment, if on or before 6/16/00:

Accounts Payable 98

Cash 98

GJE to record payment, if after 6/16/00:

Accounts Payable 98

Purchase Disc. Lost 2

Cash 100

(P.D. Lost is operating expense, like Interest Expense)

13. 13 Class Problem -Inventory Components Given the following selected information for 2001 and 2002 (in thousands):

2001 2002

Beginning inventory $ 40 $ 55

Purchases 150 160

Freight-in 6 7

Purchase discounts 3 5

Purchase returns & allowances 2 0

Cost of goods available for sale (a) (d)

Ending inventory (b) 68

Cost of goods sold (c) (e)

Note: Goods available for sale (GAS)

= BI + P(net) = EI +COGS

1. Compute the missing numbers.

2. Prepare the adjusting journal entry for 2001 and 2002, assuming the company uses the periodic system.

14. 14 Solution to Question 1: Part (a) 2001: to find GAS:

BI + P(n) = GAS

40 + 150 + 6 - 3 - 2 = GAS = 191

Part (b) 2001 to find EI:

EI2001 = BI 2002 = 55

Part (c) 2001 to find COGS:

BI + P(n) - EI = COGS

or GAS - EI = COGS

191 - 55 = COGS = 136

15. 15 Solution to Question 1:

Part (d) 2002: to find GAS:

BI + P(n) = GAS

55 + 160 + 7 - 5 - 0 = GAS = 217

Part (e) 2002: to find COGS:

BI + P(n) - EI = COGS

or GAS - EI = COGS

217 - 68 = COGS = 149

16. 16 Solution to Question 2: 2001 AJE at end of year to transfer balances in BI and Purchase components to EI + COGS (in thousands):

Inventory (ending) 55

COGS 136

Purchase discounts 3

Purchase returns & allow. 2

Freight-in 6

Inventory (beginning) 40

Purchases 150

17. 17 Solution to Question 2: 2002 AJE at end of year to transfer balances in BI and Purchase components to EI + COGS (in thousands):

Inventory (ending) 68

COGS 149

Purchase discounts 5

Purchase returns & allow. 0

Freight-in 7

Inventory (beginning) 55

Purchases 160

Now work Ex. 5-19.

18. 18 3. Cost Flow Assumptions Given: BI + P (net) = EI + COGS

How to assign costs of inflows [BI + P(net)] to EI and COGS?

Methods:

Specific identification

Average for both COGS and EI

FIFO - (first-in, first-out) for COGS

and LISH (last-in, still here) for EI

LIFO - (last-in, first-out) for COGS

and FISH (first-in, still here) for EI

(Note that we will apply only to periodic systems this semester.)

19. 19 Class Problem - Cost Flows Given the following activity for January:

Cost Total

Units per Unit Cost

Begin Inventory 20 $ 9.00 $180

Purchase 1/10 40 10.00 400

Purchase 1/22 30 11.00 330

Total available 90 units $910

Sales 1/12 30 units

1/24 25 units

Ending inventory?

BI + P - EI = Units Sold

20 + 70 - EI = 55 so EI =

20. 20 Costs Flows- Periodic System Cost of goods sold can be calculated at each sale (perpetual system), or at the end of the period (periodic system).

The periodic system evaluates the cost layers once, at the end of the period, for all sales during the period.

In this example, the total sales of 55 units will be costed out at the end of the period, using the three cost layers for the period:

Begin Inventory 20 @ $ 9.00 $180

Purchase 1/10 40 @ 10.00 400

Purchase 1/22 30 @ 11.00 330

21. 21 FIFO (LISH)- Periodic FIFO for COGS (top down)

55 units

20 @ $9 = $180

35 @ $10 = $350

Total = $530

LISH for EI (bottom up)

35 units

30 @ $11 = $330

5 @ $10 = $ 50

Total $380

22. 22 LIFO (FISH) - Periodic LIFO for COGS (bottom up)

55 units

30 @ $11 = $330

25 @ $10 = $250

Total = $580

FISH for EI (top down)

35 units

20 @ $ 9 = $180

15 @ $10 = $150

Total = $330

23. 23 Average - Periodic First calculate average:

Goods available cost = $910

Goods available units = 90 units

Avg. = $10.11 per unit

Now COGS:

55 units x $10.11 per unit = $ 556

Now EI:

35 units x $10.11 per unit = $354

24. 24 Comparison of FIFO, LIFO, and Average In times of rising prices:

highest COGS:

lowest COGS

highest EI

lowest EI

highest Net Income

lowest Net Income

Now work Ex. 5-29.

25. 25 Additional LIFO issues: LIFO and taxes

Why use LIFO for taxes?

Why use LIFO for financial statements?

LIFO and market valuation

Should market value a company higher or lower if they use LIFO?

LIFO liquidation

What happens to net income with liquidation of an old LIFO layer?

LIFO reserve

what information is contained in this disclosure?

26. 26 4. Ending Inventory:Applying the Lower-of-Cost-or-Market Rule Based on conservatism, ending inventory is valued at cost or market value, whichever is lower.

Problem: can create hidden reserves

Recognizes price decreases immediately

Defers price increase recognition until sold

Sunbeam (in 1996) wrote inventories down to zero, then (in 1997) sold the inventory for about half the original value; all of the revenue in 1997 was income because COGS = 0!

27. 27 5. Inventory Estimation (omit Retail Method) Gross Profit (gross margin) Method

Used to estimate cost of EI and COGS

for interim financial reporting (so no physical count is required).

for lost or damaged inventory (where no physical count is possible).

Can use available information from the general ledger (Sales, BI, Purchases).

Based on history of gross margin to sales and the formula:

Sales - COGS = GM

If GM is 40% of sales then COGS = 60% of sales.

Still use BI + P(net) - EI = COGS

28. 28 Class Problem, Inventory Estimation Given the following information from the general ledger:

Sales, January-March $600,000

Inventory, January 1 50,000

Purchases, January-March 450,000

If the gross margin has historically been 30 percent of sales, calculate the estimated ending inventory at March 31.

29. 29 Solution First, estimate COGS:

If GM% = 30%, then COGS = 70%

So Sales x 70% = COGS

Then, estimate EI:

BI + P (net) - EI = COGS

Now work Ex. 5-30 and 5-42.

30. 30 6. Inventory Errors Inventory errors are unique in financial reporting because they involve multiple accounts and multiple periods.

Because of the carryover nature of inventory, some inventory errors reverse out by the end of the second year involved.

To analyze, use basic inventory formula.

31. 31 Class Problem: Assume that, at the end of 2001, Xeron Corporation neglected to include $1,000 of goods in transit to the company when it performed the annual inventory count. This error went undetected through 2002. What effect would this error have on the financial statements for 2001 and 2002?

To analyze, use the inventory formula and the balance sheet formula.

32. 32 Class Problem:

BI + P - EI = COGS | NI | A = L + SE

(EI) (RE)

Note that the asset account in inventory error analysis is ending inventory, and the equity effect is retained earnings, specifically the effect on net income.

33. 33 Class Problem: Analysis (ignore the amount, it is the same throughout the analysis):

BI + P - EI = COGS | NI | A = L + SE

34. Ex. 5-24 Periodic System (assume BI = 3 dozen @ $2 per dozen)

Purchase of 15 dozen @ $2:

Purchases 30

Cash 30

Sale of 14 dozen @ $3:

Cash 42

Sales 42

December 31 AJE to transfer BI and Purchases to EI and COGS. Since EI = $2 x 3 dozen (physical count) = $6,

COGS must be: BI + P - EI = COGS

$6 + $30 - $6 = $30

AJE: COGS 30

EI 6

Purchases 30

BI 6

35. Ex. 5-19 First, you may need the following additional formulas:

(1)Sales - COGS = Gross Margin

(or Gross Profit)

S - COGS = GP

(note that net sales = S - SD - SR - SA =

Sales - Sales Disc. - Sales Returns - Sales Allow.)

(2) S- COGS - Operating Expenses = NI

S - COGS - Op.Ex. = NI

36. Ex. 5-19 To find Sales, you first need to find COGS:

BI + P(net) - EI = COGS

10,350 + 50,200 - 9,350 = COGS

51,200 = COGS

Now:

S - COGS - Op.Ex. = NI

S - 51,200 - 9,300 - 1,500 - 700 = 12,000

S = 74,700

37. Ex. 5-29 (a) Highest COGS: LIFO

(b) Highest NI: FIFO

(c) Since first year, no difference.

BI = 0 and Purchases = same.

(d) Decreasing prices reverse the

relationship, so part (a) is FIFO and

part (b) is LIFO.

38. Ex. 5-30 First, estimate COGS:

If GM% = 20%, then COGS = 80%

So Sales x 80% = COGS

100,000 x .8 = COGS = 80,000

Then, estimate EI:

BI + P (net) - EI = COGS

20,000 + 90,000 - EI = 80,000

30,000 = EI

39. Ex. 5-42 First, estimate COGS:

If GM% = 34%, then COGS = 66%

So Sales (net) x 66% = COGS

(50,000 - 6,000) x .66 = COGS = 29,040

Then, estimate EI:

BI + P (net) - EI = COGS

32,700 + 24,000 + 575 - 900 - 200 - EI = 29,040

27,135 = EI