Download

1 / 12

120 likes | 315 Views

Aviso 2 New Import Export Procedures. Who Benefits? December 5 th, 2006 CTA - PELOURO DA INDUSTRIA. Introduction.

E N D

Aviso 2New Import Export Procedures Who Benefits? December 5th, 2006 CTA - PELOURO DA INDUSTRIA

Introduction • On May 29th the Central Bank (BoM) issued Notice 2/GGBM/2006 (Aviso 2), bringing some major changes in the governing rules (Notice 6/GGBM/2005) for import and export transactions. • These new rules are scheduled to come into effect on January 1st, 2007.

Forms of Payment Before Aviso 2 • Before Notice 2 they were three (3) eligible methods of payment for imported goods: • 1. Wire Transfer or Telegraphic Transfer: the importer orders the goods and agrees on credit terms directly with his supplier. Further to their agreement the supplier couriers the documents to the importer and delivers the goods. The importer at the due date of payment instruct one of his banks to pay via a wire transfer the supplier and submits the necessary documentation that confirms the import of the goods. • 2. Advance Payment: The importer contacts his supplier and gets a proforma invoice. Then he instructs his bank to pay before the arrival of goods. After goods have arrived, the importer informs the bank that goods have arrived and provides them with the respective documentation. • 3. Letter of Credit: The importer contacts the supplier and receives a proforma invoice. Then requests his Bank to open a Letter of Credit for the amount involved and the terms agreed for the transaction. Exporter’s bank is informed that L/C is open and passes on the information to the supplier who then delivers the goods.

What is to Change With Notice 02/GGBM/06? • Article 1- gives the commercial banks an active role in the process aiming to examine the transactions and refrain from executing it, if they suspect of being an illicit operation. • Article 3 – eliminates the most common way of payment within importers in Mozambique (i.e. wire transfer), separates forms of payment for goods and services and establishes letter of collection and letter of credit as payment methods for goods.

Why BoM Changes the Rules? • Not all importers ensured that goods actually entered Mozambique; • If goods were delivered in some cases there were discrepancies between actual and those declared in the Docs; • Importers used more than one commercial bank to pay for the same goods and only one bank would have the originals docs. Others remained with an incomplete import process.

How BoM Envisages Aviso 2 to Stop illicit Transactions ? • Aviso 2 eliminates the wire transfer payment • In the advance payment method requires the supplier to issue a bank guarantee • If supplier is unwilling to use a bank guarantee Importer should use either the Letter of Collection (Cobrança Documental) or Letter of Credit as payment methods.

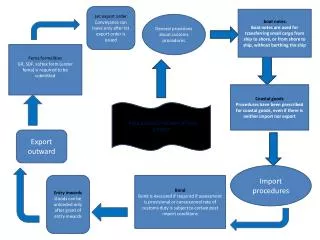

5 Importer’s Bank Exporter’s Bank The New Proposed System Mozambique World 4 5’ 3 3’ 4’ 1 Exporter Importer 2 6 6 Customs 1.Importer’ Enquiry/Order 4. Bank contacts Importer 2.Suppliers send P.I. 5. Payment acceptance 3.Establish terms with Bank (L/C,C/D) 6. Goods delivery/Customs

Issues Arising With the Proposed Solution: • Non-bank unconditional credit arrangements between suppliers and importers are no longer possible. • Suppliers may not be willing to issue a guarantee because Mozambique is a marginal importer in the International Trade or because the value of the goods can not justify such guarantee. In this case no imports can take place from the selected source. This may have cost and other serious implications for the importers/ industrialists; • If suppliers decides to issue such guarantee, the related cost would be passed on to importers, increasing forex outflow and domestic prices as well; This increases the costs of imports and will seriously affect the local firm’s competitiveness.

Issues Arising With the Proposed Solution (cont.): • Banks require cash upfront. They rarely issue a true letter of credit. This penalizes SMEs as they may not import capital goods and may face liquidity problems. This arrests country’s development. • Domestic banks may take advantage of their position in forex rates. Once the bank is assigned to handle the imports, the importer has little negotiating power. There is also doubts if Banks are in a position to handle in terms of human capacity as well as liquidity so many transactions simultaneously. • Docs may take longer to get to importers bank than the goods particularly when road transport is used. Companies while waiting for Docs would bear the storage cost at the customs.

Other Related Issues • Banks do not issue real letter of credit because have no means of assessing companies financial strength in the absence of audited accounts and there are no alternative securities due to government bureaucracy. • Bank charges are coming down but still are high by international standards and penalizes local businesses. • It is surprising why BoM does not require from commercial banks to publish their rates (interests and forex) on press so as to increase competition and cut down business costs. • Transfer of company funds between different banks may experience delays in the process, eliminating the firm’s opportunity to seize more favorable forex rates.

Conclusion • While CTA shares BoM’s concerns with regard to forex outflows, the new rules to address the problem raise a number of issues that may impact negatively on genuine businesses and may have unintended effects on the overall economy. • As these issues have been identified in advance, it is desirable to review them before Aviso 2 comes into effect and see how to accommodate the private sector concerns while preventing capital flight.

Wishes Merry Christmas and…Happy New Year (Subject to Review of Aviso 2 !!!)

![READ [PDF] Export/Import Procedures and Documentation](https://cdn7.slideserve.com/12623254/read-pdf-export-import-procedures-dt.jpg)