Download

1 / 12

140 likes | 459 Views

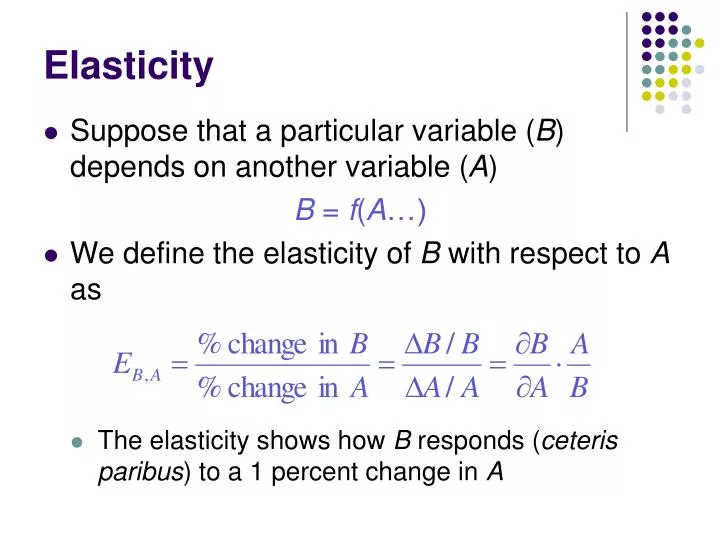

Elasticity. Suppose that a particular variable ( B ) depends on another variable ( A ) B = f ( A …) We define the elasticity of B with respect to A as. The elasticity shows how B responds ( ceteris paribus ) to a 1 percent change in A. Price Elasticity of Demand.

E N D

Elasticity • Suppose that a particular variable (B) depends on another variable (A) B = f(A…) • We define the elasticity of B with respect to A as • The elasticity shows how B responds (ceteris paribus) to a 1 percent change in A

Price Elasticity of Demand • The most important elasticity is the price elasticity of demand • measures the change in quantity demanded caused by a change in the price of the good • EP will generally be negative • except in cases of Giffen’s paradox

Price Elasticity and Total Expenditure • Total expenditure on any good is equal to Total Expenditure = PQ • Using elasticity, we can determine how total expenditure changes when the price of a good changes

Income Elasticity of Demand • The income elasticity of demand (EI) measures the relationship between income changes and quantity changes • Normal goods EI > 0 • Luxury goods EI > 1 • Inferior goods EI < 0

Cross-Price Elasticity of Demand • The cross-price elasticity of demand (EQ,P’) measures the relationship between changes in the price of one good and and quantity changes in another • Gross substitutes EQ,P’ > 0 • Gross complements EQ,P’ < 0

Linear Demand Q = a + bP + cI + dP’ where: Q = quantity demanded P = price of the good I = income P’ = price of other goods a, b, c, d = various demand parameters

Linear Demand Q = a + bP + cI + dP’ • Assume that: • Q/P = b 0 (no Giffen’s paradox) • Q/I = c 0 (the good is a normal good) • Q/P’ = d ⋛ 0 (depending on whether the other good is a gross substitute or gross complement)

Linear Demand • If I and P’ are held constant at I* and P’*, the demand function can be written Q = a’ + bP where a’ = a + cI* + dP’* • Note that this implies a linear demand curve • Changes in I or P’ will alter a’ and shift the demand curve

Linear Demand • Along a linear demand curve, the slope (Q/P) is constant • the price elasticity of demand will not be constant along the demand curve • As price rises and quantity falls, the elasticity will become a larger negative number (b < 0)

EP < -1 EP = -1 EP > -1 Linear Demand Demand becomes more elastic at higher prices P -a’/b Q a’