Download

1 / 8

130 likes | 636 Views

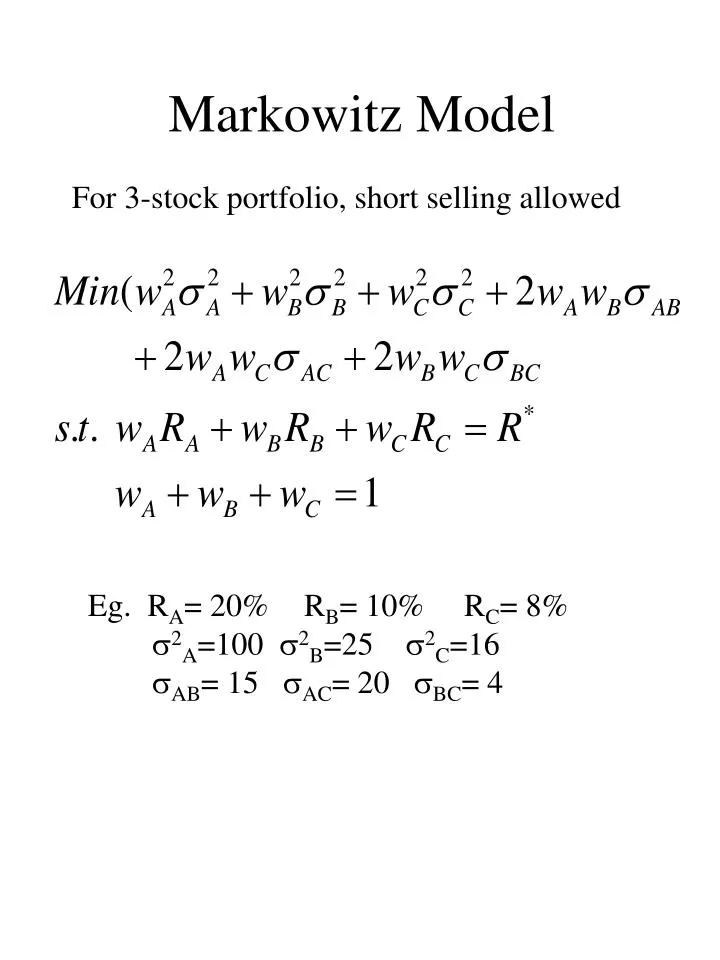

Markowitz Model. For 3-stock portfolio, short selling allowed. Eg. R A = 20% R B = 10% R C = 8% 2 A =100 2 B =25 2 C =16 AB = 15 AC = 20 BC = 4. Markowitz Model. Form the Lagrangian. Markowitz Model: Solution. For R* = 15% w A = 50.214%

E N D

Markowitz Model For 3-stock portfolio, short selling allowed Eg. RA= 20% RB= 10% RC= 8% 2A=100 2B=25 2C=16 AB= 15 AC= 20 BC= 4

Markowitz Model Form the Lagrangian

Markowitz Model: Solution For R* = 15% wA = 50.214% wB = 48.715% wC = 1.075% Standard Dev = 6.22% For R* = 20% wA = 91% wB = 56% wC = -47% (short sale) Standard Dev = 9.47%

Single Index Model Rt= A + BRmt + et E(Rt) = A + BE(Rmt) Cov(ei,ek)=0 E(ei)=0 Cov(ei,Rm)=0 2p=Pi[Ri - E(R)]2 by substitution 2=Pi[A + BRmt +ei -A - BE(Rm)]2 2=Pi{B[Rmi-E(Rm)] + ei}2 2=Pi{B2[Rmi-E(Rm)]2 +ei2+2B[Rmi-E(Rm)] ei} 2p= B2p 2m + 2e

Single Index Model (Cont’d) 2p= B2p2m + 2ep We also know that Bp= Cov(Rp, Rm)/ 2m Bp=wjBj 2ep= wj2 2ej Hence, the portfolio variance is: 2p= (xjBj )22m + xj2 2ej

Single Index Model (Cont’d) For 3-stock portfolio, short selling allowed Eg. RA= 20% RB= 10% RC= 8% 2A=20 2B=15 2C=9 A= 1.5 B= 0.75 C= 0.50

Single Index Model (Cont’d) Form the Lagrangian

Single Index Model Solution When R* = 15% wA = 0.57 wB = 0.08 wC = 0.35 Standard Deviation =