Download

1 / 18

180 likes | 190 Views

This session will provide guidance on handling stock, restricted stock, and stock options in divorce settlement agreements, including calculating community property, support on separate property, and tax implications. Expert speakers will discuss strategies for drafting tax provisions, engaging CPAs and CDFA, and calculating support based on income from equity compensation.

E N D

SCMA 2019 Family Mediation Institute Stock, Restricted Stock, and Stock Options in Settlement Agreements Addressing the Challenges of Property Division, Income Available for Support, and Taxation

Speakers Laurie Itkin Jennifer Kinnard Partner and Certified Public Accountant (CPA) Leaf & Cole Your clients can each engage a CPA to review draft tax provisions in the MSA and propose an annual or semi-annual “true-up” process to prevent under- or over-payment of support Financial Advisor and Certified Divorce Financial Analyst (CDFA) The Options Lady Your clients can engage a neutral CDFA to gather and review vesting schedule of equity compensation and calculate community property and separate property portions

Agenda • Employer-Provided Equity Compensation • Restricted Stock Units (RSU’s) • Calculating and dividing community property • Calculating support on separate property • Non-Qualified Stock Options (NSO’s) • Calculating and dividing community property • Calculating support on separate property • Suggested provisions to include in MSA • Employee Stock Purchase Program (ESPP) • Stocks/Mutual Funds/ETF’s in a Brokerage Account

The Basics • Restricted Stock Units (RSU’s) • Non-Qualified Stock Options (NSO’s)* • Employee Stock Purchase Plan (ESPP) • Stock in a brokerage account *Incentive Stock Options (ISO’s) are treated differently

Case Study Mary is a senior executive at XYZ, a publicly-traded company. She receives RSU’s and NSO’s and also participates in the company’s ESPP. When she and Greg begin mediation the majority of her vested NSO’s are “underwater.” Greg is a stay-at-home father. They have two children. The couple also owns a brokerage account containing Amazon and GE stock.

How to Calculate Marital Portion Nelson Formula Hug Formula NSOs/RSUs primarily intended to attract the employee to the job or reward past services DOH – DOS ----------------- = Community Property % DOH - DOV (DOH = Date of Hire; DOS = Date of Separation; DOV = Date of Vesting) NSOs/RSUs primarily intended as compensation for future performance and an incentive to stay with the company DOG – DOS ----------------- = Community Property % DOG - DOV (DOG = Date of Grant; DOS = Date of Separation; DOV = Date of Vesting)

RSU’s: How to Calculate Community Property Portion (DOS is 5/8/18) XYZ stock price $65.07

Tax Issues When RSU’s VestWhat happens on 11/17/18? • Mary will receive “net” shares after employer withholds shares to pay taxes • Mary can transfer half of the vested net community property shares to Greg • What if her employer under- or over-withholds? • Why does Greg have to pay Mary’s employment/FICA taxes? • What if Greg is in a lower tax bracket than Mary?

Income Available for Support Mary receives an annual cash bonus. She and Greg agree that 7% of the gross bonus will be allocated as child support and 16% as spousal support (the divorce was final in 2018 so spousal support is tax-deductible to Mary and taxable to Greg). It is the intent of the parties that the same percentages be applied to Mary’s income attributable to RSUs and NSOs. Over the next few years, when RSU’s and NSO’s vest some will be divided as property (the community property portion) and some will be considered income for support (the separate property portion).

How Much Does Greg Get From Mary? XYZ trades at $68.88 on vest date “Gross Income” is defined as fair market value of stock on vesting date and is what shows up on employee’s W-2

NSO’s: How to Calculate Community Property Portion (DOS is 5/8/18) XYZ stock price $65.07 11 months later these were worth over $400K!

What Occurs When NSOs are Exercised Greg and Mary’s divorce is final. XYZ stock’s price has skyrocketed. Greg wants to exercise his share of vested NSO Grant #9632. “Exercise and sell to cover” vs. “Exercise and sell” XYZ trading at $94.28 “Gross Income” is defined as difference between exercise price and fair market value of stock when option is exercised

Tax Provisions to Consider for MSA 1. Taxes occasioned by either the exercise of stock options or the sale of stock received as a result of the exercise of stock options shall be allocated between the parties as follows: (a) A party who receives any share of stock or the proceeds from sale of the stock shall be solely liable for, shall forever hold the other party free and harmless from any liability for, and shall fully indemnify the other party from any federal or state taxes that are attributable to that party’s exercise of options or sale of stock. (b) Any tax liability assessed against Wife that is solely attributable to the exercise of stock options or sale of stock on Husband’s behalf shall be paid by Husband to Wife upon receipt by Husband of a written tax accounting, prepared by a qualified CPA, reflecting the actual tax liability incurred by Wife as a result of the exercise of the stock options awarded to Husband under this Agreement or the sale of stock received by Husband as a result of the exercise of the options. 2. If there has been any withholding of income tax due to the exercise of the Husband’s options or sale of the stock received therefore, Husband shall be entitled to a credit for the withholding to the extent that Wife is legally able to and does transfer the taxable transaction and resulting tax liability from her tax return to Husband’s tax return. In the event that the withholding occurs and it cannot be transferred, Wife shall pay Husband, on or before April 15th of the year following the taxable exercise or sale, the amount withheld or deposited due to the exercise of the stock options or sale of stock on Husband’s behalf (together with one-half of any penalties and interest assessed against Husband for his failure to withhold).

Continued… 3. In the event the tax liability arising from the exercise of the Husband’s stock options or the sale of stock received therefore cannot be transferred by Wife to Husband, Husband shall immediately, on receipt of the written tax accounting, pay to Wife the entire tax attributable to the transaction on his stock options or sale of stock, less any taxes actually withheld and paid on her behalf or for her benefit. 4. Should additional taxes be owed as a result of the exercise of the options awarded to Husband under this Agreement at any time after the taxes have originally been paid, and if these taxes are assessed to the employee spouse, Husband shall immediately transfer to Wife the amount necessary to pay the additional taxes. If the withholding attributable to Husband is in excess of his taxes owed, Wife will refund him the difference. 5. If insufficient funds are available to pay these taxes, Husband shall allocate to Wife some of his unexercised options or unsold stock to satisfy the tax obligations. The options/stock reallocated to Wife shall cover the taxes owed as well as all taxes that will be triggered by the necessity of having to sell those options or stocks to meet the tax obligation. The number of options or stock that shall be reallocated to Wife shall be determined by an accountant or other expert of Wife’s choice, subject to Husband’s right to verify the accuracy of the calculations. If no options or stocks are available, the Court may order payment by Husband from any source the Court deems appropriate.

Other Provisions to Consider Including • Nonemployee spouse entitled to additional options granted as a result of stock split or stock dividend in same ratio as community interest. • Nonemployee spouse entitled to all benefits resulting from repricing of any options that are now or in the future may be under water. • Employee spouse information-sharing requirement for plan changes or time frame changes. • Requirement for Beneficiary Designation Form and any other appropriate form designating nonemployee spouse as the beneficiary of the unexercised options to the extent of community property interest, should employee spouse die before exercise of vested (but not exercised) community property stock.

Employee Stock Purchase Plan (ESPP) • Every month $2,000 is deducted from Mary’s paycheck which is set aside to purchase XYZ stock at a 15% discount • Every six months her employer purchases XYZ stock with the accumulated funds • The last stock purchase was Jan 1, 2018 • Greg and Mary separated on May 8, 2018 which is approximately two months before the next stock purchase date of July 1, 2018 • Mary discloses on her FL-142 the value of the stock at DOS as $40K since that is the value on the account statement • Would Greg be receiving half the community property if Mary were to transfer $20K worth of stock to him? NO, UNLESS YOU ALSO ACCOUNT FOR PAYROLL DEDUCTIONS • Tax issues related to qualifying and disqualifying dispositions create challenges when dividing these accounts

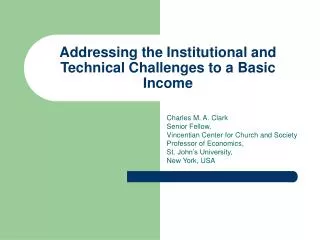

Dividing Stock in a Brokerage Account 5-Year Stock Chart Amazon 5-Year Stock Chart GE Source: Yahoo Finance Mary and Greg own a brokerage account that holds 28 shares of Amazon worth $49,702 and 5,296 shares of GE worth $49,994. Both stocks were purchased five years ago. Greg proposes taking the GE stock and Mary likes that idea because she loves Amazon and thinks the stock will continue to rise. Is this a fair division of the nearly $100K worth of community property?