Download

1 / 18

180 likes | 279 Views

Some Financial Ratios Used in BRR. Financial Condition of Owner (FCO). Answers the question: What is owner’s capacity to put in more money when needed by the business? Personal networth will exclude: Investment in the borrowing enterprise Personal assets mortgaged or used as

E N D

Financial Condition of Owner (FCO) Answers the question: What is owner’s capacity to put in more money when needed by the business? Personal networth will exclude: • Investment in the borrowing enterprise • Personal assets mortgaged or used as collateral for loan/s

FCO for Corporations • With more than 1 major stockholder, get the total networth of all the major stockholders. • The guidelines for single proprietorships shall thereafter apply. • Divide the net networth by the firm’s total loans payable.

Exercises to Compute FCO For single proprietor Mr. Santos: • Personal networth P4,000,000 • 2 vehicles mortgaged to SB P 850,000 • Investment in enterprise P1,250,000 • Total Liabilities P 750,000 Compute for the Financial Condition of the Owner.

Answer: Personal NW – Mortgaged Assets – Investment in the Enterprise divided by total loans payable = 4,000,000 – 850,000 – 1,250,000 750,000 = 1,900,000 divided by 750,000 = 2.53 = Score of 4 points

Additional Information: Personal Liabilities: Dario - P750,000 Robert – P500,000 Rowena - none Amount of Loan Applied w/SB: P 1Mn

Answers to the Exercise: 1. Major stockholders: Dario (30%), Robert (30%) & Rowena (34%): 2. Computation of individual networth for FCO : Dario: 2 Mn – 750,000 – 300,000 = 950,000 Robert: 2Mn – 500,000 – 300,000 =1,200,000 Rowena: 2 Mn – 340,000 = 1,660,000 Total 3,810,000 3. FCO for the corporation = 3,810,000 divided by the sum total of the liabilities of the firm (1,000,000) = 3.81 Score: 4 points

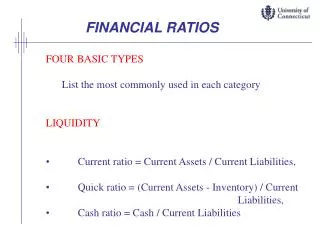

Ratios to Determine Financial Condition • Expressions of relationships between items in the F/S. • When properly interpreted, are useful indicators of financial condition and performance • Could indicate the liquidity, solvency, stability or profitability of a business.

Some Ratios used in BRR Current Ratio: Current Assets Current Liabilities Excl. long overdue ARs and obsolete Inv. Debt-Equity Ratio: Debt (TL/TA) Equity (TC/TA) Debt + Equity is always equal to 100%

Some Ratios Used in BRR • Debt Servicing Capacity: Net Income – Drawings/Dividends+ Interest + Depreciation divided by the principal and interest amortizations of LT and ST loans for one year • Accounts Receivable Level: AR/Sales x 360 days = AR level

Assets Cash 150,000 AR* 200,000 Inventory 100,000 Other Assets 550,000 Total 1,000,000 *P20,000 is long overdue Liabilities & Capital Accts. Pay. 75,000 Notes Payable 250,000 Capital 675,000 Total 1,000,000 Exercise: Santos Enterprise

Additional Information Sales P2,500,000 Net Income P450,000 Interest Expense P50,000 Depreciation P50,000 Business Location Baguio City Family of three (has 1 child)

Compute the ratios and the equivalent scores under BRR: • Current Ratio • Debt-Equity Ratio • Debt Servicing Capacity • Accounts Receivable Level

Computation of Current Ratio: Cash 150,000 AR* (200,000-20,000) 180,000 Inventory 100,000 Total Current Assets 430,000 Total Current Liabilities 325,000 CR = 430,000 = 1.32 325,000 Score = 3 points

Computation of Debt Equity Ratio: Total Liabilities divided by Total Capital Total Assets Total Assets = 325,000 divided by 675,000 1,000,000 1,000,000 = 32.5:67.5 Score = 7.5

Computation of DSC DSC = NI – Drawings/Dividends+Int.+Depn Prin. & Int. Amort. (1 yr) LT & ST Loans DSC = 450,000-200,000+50,000+50,000 250,000+50,000 = 350,000/300,000 = 1.16 Score = 10 pts.

AR level 2.5Mn divided by 360 days = 6,944.44 200,000 divided by 6,944.44 = 29 days Score = 5 points 200,000/2,500,000 x 360 = 28.8 or 29 days Score = 5 points