Download

1 / 15

150 likes | 285 Views

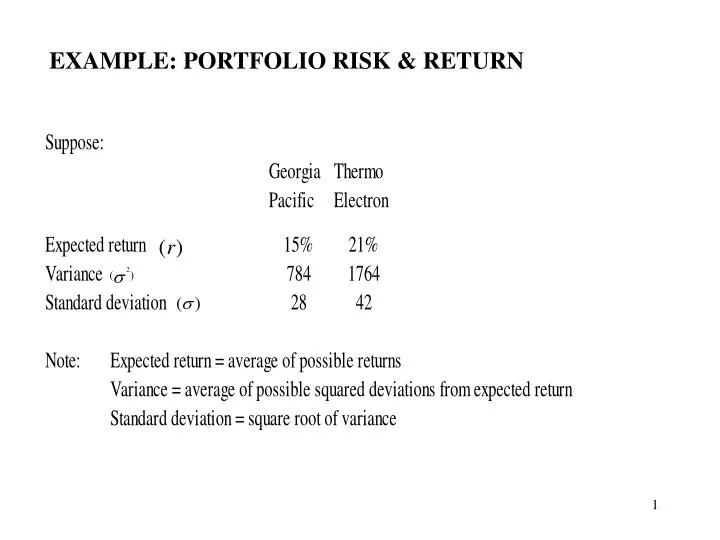

EXAMPLE: PORTFOLIO RISK & RETURN. PORTFOLIO RISK. PORTFOLIO RISK: EXAMPLE. Return and Risk for Portfolios. SUPPOSE EXPECTED RETURNS ARE AS FOLLOWS:. EXAMPLE:INTERNATIONAL PORTFOLIO SELECTION. CORRELATIONS BETWEEN RETURNS ON DIFFERENT MARKETS. EFFICIENT PORTFOLIOS.

E N D

Capital Market Line (CML) • Equilibrium relationship between E(Rp) and σp for efficient portfolios • Linear efficient set of CAPM by combining Market portfolio with risk free (rf) borrowing and lending • CML only permits to well-diversified portfolios; portfolios not employing M, the market portfolio, will plot below the CML • Equation of CML: E(Rp)=rf + [(E(RM)-Rf )/σM] σ(Rp) • Slope of CML: price of risk {E(RM) – Rf }/ σM • Price of time: Rf

Capital Asset Pricing Model (CAPM) • Developed by Sharpe, Treynor, Lintner and Mossin • An equilibrium theory of how to price and measure risk of portfolios as well as individual security • Concerning decomposition of risk into two components: systematic (market, non-diversifiable) and unsystematic (unique, diversifiable) • Stating that required return on any investment is the risk free return plus a risk premium measured by its systematic risk E(ri)=rf+[E(rm)-rf]β where β = covariance risk of security i E(rm)-rf = market risk premium

Feasible Set of Risky Portfolios Expected portfolio Return Kp B C A D Feasible, or Attainable, Set E Risk, σp

Optimal Portfolio Selection Expected portfolio Return Kp B C Optimal Portfolio Investor B A D Optimal Portfolio Investor A E Risk, σp

Efficient Frontier with Risk-Free Asset Expected portfolio Return Kp new efficient portfolio Z B KM C M Y=mx+b Ki=Krf+σi/σm(Km-Krf) b = intercept m = slope = Km-Krf/σm A D kRF E rm Risk, σp