Download

1 / 24

240 likes | 579 Views

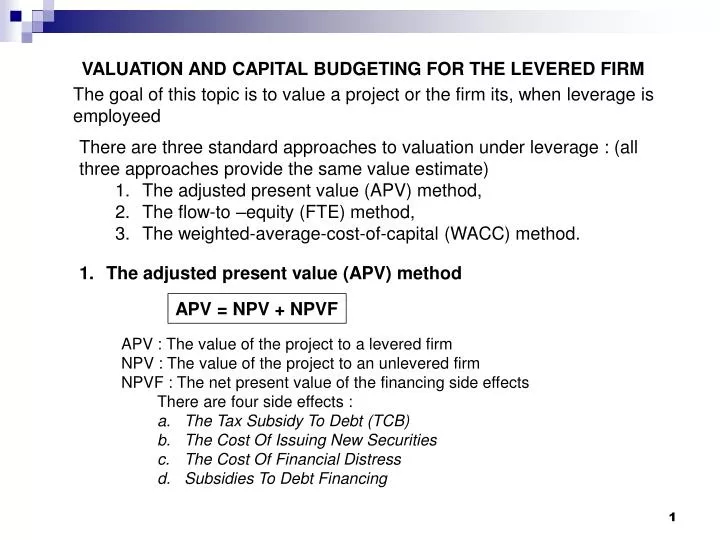

VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRM. The goal of this topic is to value a project or the firm its, when leverage is employeed. There are three standard approaches to valuation under leverage : (all three approaches provide the same value estimate)

E N D

VALUATION AND CAPITAL BUDGETING FOR THE LEVERED FIRM The goal of this topic is to value a project or the firm its, when leverage is employeed • There are three standard approaches to valuation under leverage : (all three approaches provide the same value estimate) • The adjusted present value (APV) method, • The flow-to –equity (FTE) method, • The weighted-average-cost-of-capital (WACC) method. • The adjusted present value (APV) method APV = NPV + NPVF • APV : The value of the project to a levered firm • NPV : The value of the project to an unlevered firm • NPVF : The net present value of the financing side effects • There are four side effects : • The Tax Subsidy To Debt (TCB) • The Cost Of Issuing New Securities • The Cost Of Financial Distress • Subsidies To Debt Financing

Example (considers the tax subsidy), but not the other three side effects. Assume, a Project of the P.B. Singer Co, with characteristics : Cash inflows : $500,000 per year for the indefinite future Cash costs : 72% of sales ; Initial investment : $475,000 TC : 34% ; rO : 20% (the cost of capital for all-equity firm) If both the project and the firm are financed with only equity, the project’s cash flow is Cash inflows $500,000 Cash costs -360,000 Operating income 140,000 Corporate tax (0,34 tax rate) -47,600 Unlevered cash flow (UCF) $92,400 Given a discount rate or 20%, the PV of the project is $92,400/0.20 = $462,000

The NPV of the project, that is, the value of the project to an all-equity firm, is • $462,000 - $475,000 = -$13,000 (The project would be rejected by an all-equity firm) Assume, the firm finances the project with exactly $126,229.50 in debt, so that remaining investment of $348,770.50 ($475,000 - $126,229.50) is financed with equity. APV = NPV + TCxB $29,918 = -$13,000 + 0,34 x $126,229.50 (accepted project) • Flow-To-Equity Approach (FTE) approach is an alternative capital-budgeting approach. FTE = Cash flow from project to equityholders of the levered rs (cost of equity capital)

There are three steps to the FTE approach. Step 1 : Calculating Levered Cash Flow (LCF) Assuming an interest rate of 10%, the perpetual cash flow to equityholders in our example is Cash inflows $500,000.00 Cash costs -360,000.00 Interest (10% x $126,229.50) -12,622.95 Income after interest 127,377.05 Corporate tax (0.34 tax rate) -43,308.20 Levered cash flow (LCF) $84,068.85 UCF – LCF = (1 - TC) rBB UCF- (1 - TC) rBB = LCF $92,400 – (1 -0.34)x 0.10 x $126,229.50 = $84,068.85

Step 2. Calculating rs Assume, ro =20% ; debt to value ratio of ¼ implies a target debt-to-equity ratio of 1/3. The formula for rs is rs= ro + (1- TC) ( ro - rB) rs = 0.20 + 1/3. (0.66) (0.20 – 0.10) = 0.222 Step 3. Valuation The present value of the project’s LCF is The NPV of the project is simply the difference between the PV of the project’s LCF and the investment not borrowed. So, NPV is $378,688.50 – ($475,000 - $126,229.50) = $29,918

Weighted-Average-Cost-Of-Capital Method • The WACC approach begins with the insight that projects of levered firms are simultaneously with both debt and equity. • The formula rWACC is The NPV of the project can be written is If the project is a perpetuity, the NPV is [UCF / rWACC ] – Initial investment rWACC = ¾ x 0.22 + ¼ x 0.10 (0.66) = 0.183 The NPV of the project is [$92,400/0.183] - $475,000 = $29,918

# A COMPARISON OF THE APV, FTE, AND WACC APPROACHES • The APV approaches first values the project on an all-equity basis. • The FTE approaches discounts the after-tax cash flow from a project going to the equityholders of a levered firm (LCF) • The WACC calculates the project’s after-tax cash flows assuming all- equity financing (UCF). • All three approaches perform the same task : valuation in the presence of debt financing. • APV & WACC display the greatest similarity. • The FTE approach, the future cash flows to the levered equityholders (LCF) are valued.

THE THREE METHODS OF CAPITAL BUDGETING WITH LEVERAGE • Adjusted-Present-Value (APV) Method UCFt = The project’s cash flow at date t to the equityholders of an unlevered firm r0 = Cost of capital for project in an unlevered firm • Flow-to-Equity (FTE) Method LCFt = The project’s cash flow at date t to the equityholders of a levered firm rs = Cost of equity capital with leverage • Weighted-Average-Cost-Of-Capital (WACC) Method rWACC = Weighted average cost of capital • Notes : • The middle term in the APV formula implies that the value of a project with leverage is greater than value of the project without leverage. Since rWACC < r0 the WACC formula implies that the value of a project with leverage is greater than the value of the project without leverage. • In the FTE method, cash flow after interest (LCF) is used. Initial investment is reduced by amount borrowed as well. • Guidelines : • Use WACC or FTE if the firm’s target debt-to-value ratio applies to the project over its life. • Use APV if the project’s lebel of debt is known over the life of the project.

# CAPITAL BUDGETING WHEN THE DISCOUNT RATE MUST BE ESTIMATED Example : WWE is a large conglomerate thinking of entering the widget business, where it plans to finance projects with a debt-to-value ratio of 25% (a debt-to-equity-ratio of 1/3). There is currently one firm in the widget industry, (AW). This firm is financed with 40% debt & 60% equity. The beta of AW’s equity is 1.5. AW has a borrowing rate of 12%, & WWE expects to borrow for its widget venture at 10%. TC is 40%, the market risk premium is 8.5%, and Rf is 8%. What is the appropriate discount rate ( ro, rs, & WACC) for WWE to use for its widget venture? The four step procedure will allow us to calculate all three discount rates. • Determining AW’s Cost of Equity Capital (using the SML) • AW’s cost of Equity Capital : • rs = RF + (RM – RF) • 20.75%= 8% + 1.5 x 8.5%

Determining AW’s Hypothetical All-Equity Cost of Capital • AW’s cost of capital if All-Equity : (MM Proposition II under taxes) • rS = rO + (1 - TC) (rO – rB ) • 20.75% = ro + (0.4/0.6) (0.60) (rO – 12%) • rO = 0.1825 • Determining rs for WWE’s Widget Venture. Using the FTE, where the discount rate for levered equity is determined from : • Cost of Equity Capital for WWE’s Widget Venture: rs = 18.25% + 1/3(0.60) (18.25% - 10%) = 19.9% < cost of equity capital for AW, 0.2075 • Determining rWACC for WWE’sWidget Venture: rWACC = (3/4) 19.9% + (1/4) (10%) (0.60) = 16.425%

Initial cost Depreciation tax shield Presentvalue of (Cash revenues – Cash expenses) # APV EXAMPLE Bicksler Enterprises is considering a $10 million project that will last five years, implying straight-line depreciation per year of $2 million. The cash revenues less cash expenses per year are $3,500,000. TC is 34%, Rf is 10%, & the cost of unlevered equity is 20%. We stated before that the APV of a project is the sum of its all-equity value plus the additional effects of debt. We examine each in turn. All-Equity Effects Value Assuming the project is financed with all equity, the value of the project is

Additional Effects of Debt Bicksler enterprises can obtain a five-year, nonamortizing loan for $7,500,000 after flotation costs at the risk-free of 10 percent. Flotation costs are fees paid when stock or debt is issued. Flotation Costs Given that flotation costs are 1 percent of the gross proceeds,we have $7,500,000 = (1 – 0.01) x Gross proceeds = 0.99 x Gross proceeds Thus, the gross proceeds are This implies flotation costs of $75,758 (1% x $7,575,758). To check the calculation, note that net proceeds are $7,500,000 ($7,575,758 - $75,758).

The relevant cash flows from flotation costs are in boldface. When discounting at 10 percent, the tax shield has a net present value of $5,152 x A50.05 = $19,530 This implies a net cost of flotation of -$75,758 + $19,530 = -$56,228 The net present value of the project after the flotation costs of debt but before the benefits of debt is -$513,951 - $56,228 = $570,179 Interest cost after tax is $500.000 [$757.576 x (1 – 0.34)]. Because the loan is nonamortizing, the entire debt of $7,575,758 is repaid at date 5. These terms are indicated below:

Present value of after-tax interest payments Amount borrowed Present value of loan repayments NPV (Loan) = + - - The calculation for this example are

The NPV (Loan) is positive, reflecting the interest tax shield. • The adjusted present value of the project with this financing is • APV = All-equity value – flotation costs of debt + NPV (Loan) • $406,236 = -$513,951 - $56,228 + $976,415 • Though we previously saw that an all-equity firm would reject the project, a firm would accept the project if a $7,500,000 (net) loan could be obtained. Non-Market-Rate Financing A number of companies are fortunate enough to obtain subsidized financing from a governmental authority. Suppose that the project of Bicksler Enterprises is deemed socially beneficial and the state of New Jersey. Grants the firm a $7,500,000 loan at 8-percent interest. In addition, all flotation costs are absorbed by the state. Clearly, the company will choose this loan over the one we previously calculate. The cash flows from the loan are

The relevant cash flows are listed in boldface in the preceeding table. Using equation (17.1), the NPV (Loan) is APV = All-equity value – Floatation costs of debt + NPV (Loan) +$827,988 = -$513,951 - 0 + $1.341,939

# BETA AND LEVERAGE The No-Tax Case (The relationship between the beta of the common stock and leverage of the firm in a world without taxes : Assumption that the beta of debt is zero. Equity = Asset (1 + Debt/Equity) The corporate-Tax Case: (The relationship between the beta of the unlevered firm and beta of the leverage equity) is Equity = (1 + (1- TC )Debt/Equity)Unlevered firm

EXAMPLE C.F. Lee Incorporated is considering a scale-enhancing project. The market value of the firm’s equity is $200 million. The debt is considered riskless. The corporate tax rate is 34 percent. Regression analysis indicates that the beta of the firm’s equity is 2. the risk-free rate is 10 percent, and the expected market premium is 8.5 percent. What would the project’s discount rate be in the hypothetical case that C.F. Lee, Inc., is all-equity? We can answer this question in two steps. • Determining Beta of Hypothetical All-Equity Firm. Rearranging equation (17.4), we have Unlevered Beta

Determining Discount Rate. We calculate the discount rate from the security market line (SML) as Discount Rate: EXAMPLE The J. Lowes Corporation, which currently manufactures staples, is considering a $1 million investment in a project in the aircraft adhesives industry. The corporation estimates unlevered after-tax cash flows (UCF) of $300,000 per year into per-perpetuity from the project. The firm will finance the project with a debt-to-value ratio of (or, equivalently a debt-to-equity ratio of 1:1). The three competitors in this new industry are currently unlevered, with betas of 1.2, 1.3, and 1.4. Assuming a risk-free rate of 5 percent, a market-risk premium of 9 percent, and a corporate tax rate of 34 percent, what is the net present value of the project?

We can answer this question in five steps. • Calculating the Average Unlevered Beta in the Industry. The average unlevered beta across all three existing competitors in the aircraft adhesives industry is • Calculating the Levered Beta for J. Lower’s New Project. Assuming the same unlevered beta for this new project as for the existing competitors, we have, from equation (17.4), Levered Beta:

Calculating the Cost of Levered Equity for the New Project. We can calculate the discount rate from the security market line (SML) as Discount Rate: • Calculating the WACC for the New Project. The formula for determining the weighted average cost of capital, rWACC is • Determining the Project’s Value. Because the cash flows are perpetual, the NPV of the project is

DIVIDEND POLICY • The term dividend usually refers to a cash distribution of earnings. • Public companies usually pay regular cash dividends four times a year. • The amount of the dividend is expressed as dollars per share (dividend per share), as a percentage of the market price (dividend yield), or as a percentage of earnings per share (dividend payout).

Days Thursday, January 15 Wednesday, January 28 Friday, January 30 Monday, February 16 Declaration date Ex-dividend date Record date Payment date • Standard Method of Cash Dividend Payment • FIGURE 18.1 Example of Procedure for Dividend Payment • Declaration Date: The board or directors declares a payment of dividends. • Record Date: A share of stock becomes ex-dividend on the date the seller is entitled to keep the dividends are distributable to shareholders of record on a specific date. • Ex-dividend Date: A share of stock becomes ex-dividend on the date the seller is entitled to keep the dividend; under NYSE rules, shares are traded ex-dividend on and after the second business day before the record date. • Payment Date: The dividend checks are mailed to shareholders of record.

Price = $(P+1) -t -2 -1 0 +1 +2 t $1 is the ex-dividend price drop Price = $P FIGURE 18.2 Price Behavior around the Ex-dividend Date for a $1 Cash Dividend Perfect-world case Ex-date The stock price will fall by the amount of the dividend on the ex-date (time 0). If the dividend is $1 per share, the price will be equal to P on the ex-date. Before ex-date (-1) Price = $(P + 1) Ex-date (0) Price = $P