Download

1 / 22

220 likes | 370 Views

Market Structure. The Nordic Association of Marine Insurers. Business model A. Scandinavian. Cover Claim information Claim payment. Ship owner/ Management company (Assured). Claims leader. Broker. Co-insurers. Business model B. Non-Scandinavian. Cover Claim information

E N D

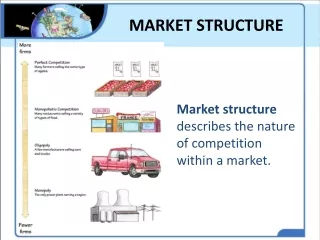

Market Structure The Nordic Association of Marine Insurers

Business modelA. Scandinavian Cover Claim information Claim payment Ship owner/ Management company (Assured) Claims leader Broker Co-insurers

Business modelB. Non-Scandinavian Cover Claim information Claim payment Ship owner/ Management company (Assured) Broker Claim leader Co-insurers

Business modelB. Non-Scandinavian Cover Claim information Claim payment Ship owner/ Management company (Assured) Survey Claims Leader Co-insurers Adjuster

Business modelB. Non-Scandinavian Cover Claim information Claim payment Ship owner/ Management company (Assured) Adjuster Claims Leader Co-insurers Broker

Distribution of risk Ship owner Insurer Capital / assets Broker Foreign capital Reinsurance

Market structure - overview Ship owner Broker Insurer Reinsurer

Market structure - overview Ship owner Risk information Broker Insurer Premium and claim payment Reinsurer

Terms • Syndicated risks – • Two or more underwriters / insurers subscribe to the same risk against their portion of the premium, risk and claims = Spread of risk • Used in • Marine, energy, transport and aviation insurance • Reinsurance • Larger non-marine risks The Nordic Association of Marine Insurers

Syndicated risks • Co-insurance • Two or more insurers each have part of the risk under a single insurance • In practice, the insurer with the largest line acts as «lead», but the co-insurers is not obligated to follow a «lead» if they not want to • Chapter 9 in the Plan regulates relationship between the claims leader and the co-insurers The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Premium Volume 2011 (USD billions)– • Marine liability (non-P&I Clubs) 1.8 ( 5.7%) • Offshore / energy 4.5 (14.2%) • Hull & Machinery 8.4 (26.2%) • Cargo / transport 17.2(54.0%) • Total 31.9 • Mutual P&I Clubs 3.4 • Estimated global premium volum USD 34 billion • (IUMI Sep 2012) The Nordic Association of Marine Insurers

The Global Marine Insurance Market The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Premium Volume 2011 (USD million) – Hull & Machinery • Nordic / Cefor 933 11% • UK ILU/IUA 294 4% • UK Lloyd’s 1243* 15% • China 932 11% • Japan 697 8% • France 512 6% • Italy / US / Netherlands 361 each 4% each • Korea / Spain 300 each 3% each • Rest 2,167 26% • 8,400 • *incl fac reinsurance premium The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Premium Volume 2011 (USD million) – Cargo / transport • Japan 1.961 11% • China 1.548 9% • Germany 1.204 7% • UK Lloyd’s 1.170 7% • France 860 5% • US 774 5% • Brasil 688 4% • - - - • Nordic 378 2% • Rest 8.600 50% • 17.200 The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Results – Gross ultimate loss ratios % • (Technical break even is achieved when the gross loss ratio does not exceed 100% minus expense ratio, usually 20 – 30%) • (IUMI Sep 2012 – Net premium vs. net claims) The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Premium Volume 2011 (USD million) – Offshore Energy • UK Lloyd’s 2.615 58% • US / Brasil / Nigeria / Malaysia 210 4 – 5% each • Nordic 135 3% • Rest 945 21% • (4.500) The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Claim trends (by policy years) – • H&M • 2007 Starts at high loss ration level, - expected to produce technical loss, premium increases do not balance cost inflation • 2008 Fewer major claims, but uncertainty iro the effect of change in market conditions and repair cost • 2009 Continued improvement on major losses (i.e. fewer) • 2010 Claim costs and loss ratio stabilize at high level • 2011 Impact of major claims • Cargo / transport • 2002 – 2007 Overall stable results • 2005 Slightly worse than average – Katrina • 2007 Signs of worsening trend • 2008 Worsening trend confirmed • 2009 Impact of catastrophe losses • 2010 Worsening trend confirmed, loss ratio stabilize at high level • 2011 Impact of natural catastrophes and increased GA claims The Nordic Association of Marine Insurers

The Global Marine Insurance Market • Claim trends – • Offshore • Volatile business • Rates, terms and conditions improved after 2000 • Long time lag between accident and claim payment • No regular claims patterns • Increasing effect of single loss events • Events with high liability cost in 2009 and 2010 The Nordic Association of Marine Insurers

Market conditions mid 2013 • Important issues – • Flat world / global market place • Financial crisis: Most insurance buyers are influnced by reduced financial activity, - rebounced 2009/10 and then to cool off again, - light at the end of the tunnel? • Amount of cargo transported is increasing but values are diminishing • Vessel values are reduced • Offshore Energy proceeds at high pace and with new risk challenges (more advanced tecnologies) • Capital crunch and reduced (lack of) financial income increases focus on technical results for underwriters • Regulatory issues / moral hazards • (Subjective views of the lecturer) The Nordic Association of Marine Insurers

Market conditions going forward from mid 2013 • Important issues listed will influence the insurance market • Survival based on long term sustained profitable underwriting • Financial income important but not to be relied upon • Service providers vs. capital providers • Distribution • (Subjective views of the lecturer) The Nordic Association of Marine Insurers