Download

1 / 2

20 likes | 156 Views

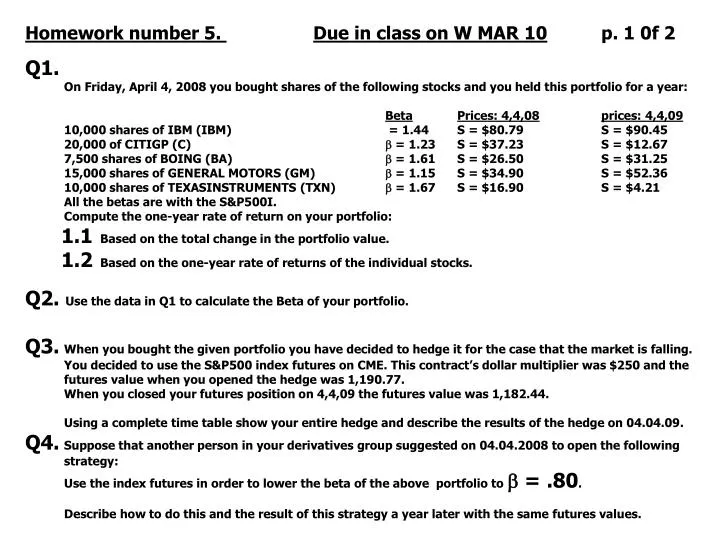

Homework number 5. Due in class on W MAR 10 p. 1 0f 2 Q1. On Friday, April 4, 2008 you bought shares of the following stocks and you held this portfolio for a year: Beta Prices: 4,4,08 prices: 4,4,09 10,000 shares of IBM (IBM) = 1.44 S = $80.79 S = $90.45

E N D

Homework number 5. Due in class on W MAR 10 p. 1 0f 2 • Q1. • On Friday, April 4, 2008 you bought shares of the following stocks and you held this portfolio for a year: • BetaPrices: 4,4,08prices: 4,4,09 • 10,000 shares of IBM (IBM) = 1.44 S = $80.79 S = $90.45 • 20,000 of CITIGP (C) = 1.23 S = $37.23 S = $12.67 • 7,500 shares of BOING (BA) = 1.61 S = $26.50 S = $31.25 • 15,000 shares of GENERAL MOTORS (GM) = 1.15 S = $34.90 S = $52.36 • 10,000 shares of TEXASINSTRUMENTS (TXN) = 1.67 S = $16.90 S = $4.21 • All the betas are with the S&P500I. • Compute the one-year rate of return on your portfolio: • 1.1 Based on the total change in the portfolio value. • 1.2 Based on the one-year rate of returns of the individual stocks. • Q2. Use the data in Q1 to calculate the Beta of your portfolio. • Q3. When you bought the given portfolio you have decided to hedge it for the case that the market is falling. You decided to use the S&P500 index futures on CME. This contract’s dollar multiplier was $250 and the futures value when you opened the hedge was 1,190.77. • When you closed your futures position on 4,4,09 the futures value was 1,182.44. • Using a complete time table show your entire hedge and describe the results of the hedge on 04.04.09. • Q4. Suppose that another person in your derivatives group suggested on 04.04.2008 to open the following strategy: • Use the index futures in order to lower the beta of the above portfolio to = .80. • Describe how to do this and the result of this strategy a year later with the same futures values.

p 2 of 2. Q5. Trader A holds a short position in 25 NYMEX Gold futures for MAR 2009. Every contract is for 100 ounces. B was A’s counterparty on the 25 short contracts. The Settlement price two nights ago was $800. Yesterday, at 11:00AM A closed 10 contracts for $802/ounce. When A closed these 10 contracts the counterparty was C. The Settlement price last night was $799/ounce. A, B and C did not engage in any other trades. Calculate the cash flows to the margin accounts of A, B and C. Q6. Bonus problem. Not mandatory. Suppose that we decide to hedge a spot trade of commodity A by opening two futures positions. One of these futures positions is on A itself. The other one is on a different commodity, B, and it is known that the futures prices on commodities A and B are uncorrelated. Develop the minimum variance hedge ratios so as to determine the optimal number of futures for each of the commodities.