Download

1 / 25

290 likes | 488 Views

Capital Budgeting, Public Infrastructure Investment, and Project Evaluation. Troy University PA6650- Governmental Budgeting Chapter 6. Capital Expenditures. Purchase of public capital assets Public infrastructure for private purposes Roads, sewers, transportation systems

E N D

Capital Budgeting, Public Infrastructure Investment, and Project Evaluation Troy University PA6650- Governmental Budgeting Chapter 6

Capital Expenditures • Purchase of public capital assets • Public infrastructure for private purposes • Roads, sewers, transportation systems • Crucial for private economic growth • Public infrastructure for public purposes • Schools, parks, hospitals, jails, police/fire stations, bases

Capital Budgeting • Focuses decisions • Facilitates financial planning • Smooths tax rates over time • Regularizes the provision of projects that: • Have a long life (10 or 15 years) • Have a high price tag • Are non-recurring

Why Have a Capital Budget? • Separate consideration can improve both efficiency and equity of projects • Won’t be cutting capital projects from a tight ops budget • Big-ticket items don’t make a budget appear abnormal • Capital budgets can stabilize tax rates • Special review of capital budgets necessary because projects have high cost and high impact • Capital budgets are a good tool to manage resources

Capital Budget Process • 5 steps: • Capital Asset Inventory • Development of the Capital Improvement Plan (CIP) • Development of the financing plan • Implementation of the capital budget • Execution • Concerned with: • Selection from a multitude of alternatives • Timing of the expenditure of the projects • Impact on total government finances

Capital Asset Inventory • Assessment of the existing situation • Inventory of capital facilities including: • Age • Condition • Degree of use • Capacity • Replacement cost • Repair or build new?

Capital Improvement Plan • A list of projects for the next 6 years or so • Includes narrative and cost data • Screening for costs, interrelationships, priorities • Scheduling to avoid waste (new sewers precede paving) • Based on growth • Based on strategic goals

Financing Plan & Analysis • Must stay within financial capability • Review of revenue, debt structure • Present and anticipated revenue • Partnering with other governments & agencies • Recurring expenditures • Buy it when it is affordable

Implementation of theCapital Budget • Prioritization process • Functional areas (safety, recreation, health) • Problem severity (alligators in swamp) • Status of support (mandate, referenda) • Formal scoring system • Legislative review, executive signs

Execution of the Capital Budget • Special attention to: • Rules (bidding, procurement) • Controls (keep it on schedule) • Monitoring project cost (no overruns)

Problems In Capital Budgeting • Assumes a continuous cycle of reappraisal due to a dynamic world. Things change. • Which projects belong in the capital budget? • Availability of funds can distort priorities • Different pots/colors of money • A strong bias towards borrowing • Difficult to establish priorities

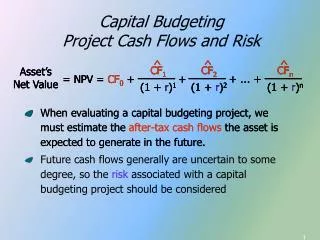

Accounting for Time • Discounting • The process of converting a stream of returns or costs incurred over time to a single present value (net present value, or NPV) • Compounding • The time value of money calculating principal and interest (interest can be compounded annually, semi-annually, quarterly, monthly, weekly, or daily)

Discounting and Compounding • Examples of discounting • Bond market • Early payment of invoice • Lottery payoffs • Examples of compounding • IRA • Certificate of Deposit

Time Value of Money r = interest rate (usually a decimal…6% = .06) FV = future value PV = present value n = number of years FV = PV (1 + r) p.258 compounding example: 1050 = $1,000 + ($1,000 x 0.05) For multiple years, FV = PV (1 + r) n If compounded semi-annually, then: FVn = PV (1+ (r/x))2n

Time Value of Money r = interest rate (usually a decimal…6% = .06) FV = future value PV = present value n = number of years p.260 discounting example: PV = FV1 (1+r) For multiple years, PV = FVn (1+r)n

Practice • R = 6% • PV = $1000 • FV after 1 year? • FV after 2 years? • FV after 1 year compounded semi-annually?

Practice • R = 6% • PV = $1000 • FV @ 1 year? $1000 x (1.06) = $1,060 • FV @ 2 years?$1060 x (1.06) = $1,123.60 • FV after 1 year compounded semi-annually? $1000 +($30 + $30.90) = $1060.90

Discounting • Works backwards…$1000 next year is worth $952.38 right now assuming 5% interest compounded annually • NPV Analysis • Used to compare dissimilar projects • Look at page 261 • Project A is the best choice at 10% interest • Project B is the best choice at 3% interest

Cost-Benefit Analysis • A means to prioritize and decide • Does not necessarily outweigh politics • One measure of efficiency • Helps evaluate alternative proposals • 5 steps: • Categorizing project objectives • Estimating the project’s impact on objectives • Estimating project costs • Discounting cost & benefit flows @ appropriate rates • Summarizing findings for decision makers

Cost-Benefit Analysis • Project objectives • What desirable benefits and results? • Annual cost, revenue, loss • Benefits estimation and valuation • Pilot studies for impact • Worth of the impact measured in dollars • Estimation of consumer’s surplus = “What would a consumer be willing to pay?” • Contingent Valuation Method

Cost-Benefit Analysis • Estimating project costs • Construction • Operating • Opportunity • Life cycle • Three adjustments necessary • Undesirable effects (negative externalities) • Unemployed resources with no alternative use • Social costs (other possible uses)

What Discount Rate? • Cost of borrowed funds (what the government has to pay for borrowing) • Opportunity cost (what private resources could earn) • Sidebar 6-2

Decision Criteria • Summarize the economic case for the project • Benefit/Cost Ratio (BCR) (greater than one desired) • Cost/Benefit Ratio (CBR) (less than one desired) • Net Present Value (greater than zero desired) • Payback Period (time taken to recover the cost) • Internal-rate-of-return (interest generated compared to discount rate – it should be higher)

Special Problems ofCost-Benefit Analysis • Multiple objectives • Economic • Income redistribution • Distribution effects • Social benefits • Cost of human life • Can’t account for everything • Politics

Conclusion • Public capital infrastructure contributes to both public and private production • Most capital projects involve a stream of income or payments • Cost benefit analysis helps to determine what the return will be. • Numbers are important. There are, however, other considerations.