Download

1 / 9

90 likes | 104 Views

This article discusses the funding model for transporters in the energy industry, including the costs and benefits associated with implementing changes. It also explores the various activities and services that are covered under this funding model.

E N D

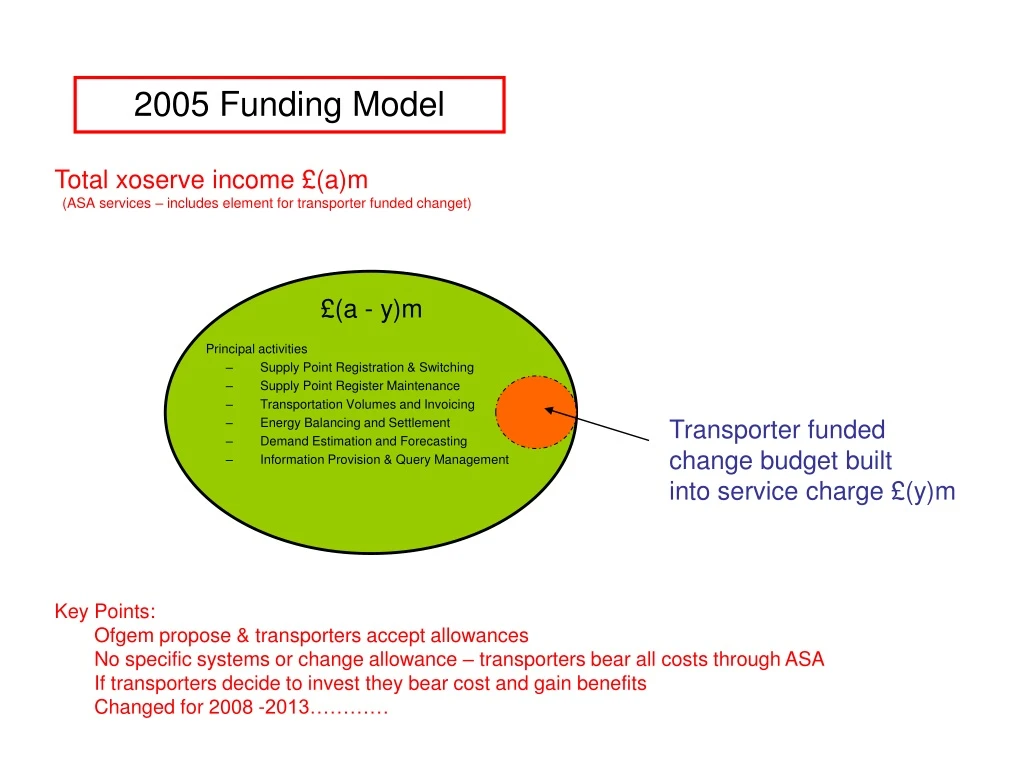

2005 Funding Model Total xoserve income £(a)m (ASA services – includes element for transporter funded changet) £(a - y)m • Principal activities • Supply Point Registration & Switching • Supply Point Register Maintenance • Transportation Volumes and Invoicing • Energy Balancing and Settlement • Demand Estimation and Forecasting • Information Provision & Query Management Transporter funded change budget built into service charge £(y)m Key Points: Ofgem propose & transporters accept allowances No specific systems or change allowance – transporters bear all costs through ASA If transporters decide to invest they bear cost and gain benefits Changed for 2008 -2013…………

2008 – 2013 Funding Model Total xoserve income £ a (includes base lined services & change budget) £(a-y)m £(y)m • Transporter funded change budget £(y)m • e.g Pricing changes

£(b)m 2008 – 2013 Funding Model • Day 1 Code User Pays £(b)m • Must Reads • AQ amendments • Shipper Agreed Reads • User Admission Total xoserve income £ a (includes base lined services & change budget) + b £(a-y)m £(y)m • Transporter funded change budget £(y)m • e.g Pricing changes

£(b)m £(c)m 2008 – 2013 Funding Model • Day 1 Code User Pays £(b)m • Must Reads • AQ amendments • Shipper Agreed Reads • User Admission Total xoserve income £ a (includes base lined services & change budget) + b + c £(a-y)m £(y)m • Transporter funded change budget £(y)m • e.g Pricing changes • Day 1 Non-code User Pays £(c)m • IAD (SCOGES) • Bespoke reports

£(b)m £(c)m 2008 – 2013 Funding Model • Day 1 Code User Pays £(b)m • Must Reads • AQ amendments • Shipper Agreed Reads • User Admission Total xoserve income £ a (includes base lined services & change budget) + b + c + x • New Code User Pays £(x)m • Incremental Service Lines • USRV resolution (Mod 192) • Development Cost Reclaims • Mod 224 development cost £(a-y)m £(x)m £(y)m • Transporter funded change budget £(y)m • e.g Pricing changes • Day 1 Non-code User Pays £(c)m • IAD (SCOGES) • Bespoke reports Key Points: Incremental change funded by incremental revenue Better cost targeting Although PCR forecast allowance mechanism remains for bulk of xoserve funding

GDPCR – Final Proposals (Dec 2007, Section 8.9) £(a)m £(b)m £(c)m £(x)m

CAPEX What did the Final Proposals say …… 4.50 Non Operational capex includes GDN expenditure on System operations, IS systems, xoserve, tools and vehicles. Our consultants have reviewed the proposed levels of expenditure considering historical expenditure by the GDNs and project specific expenditure for projects above a materiality threshold of £0.5 million.

CAPEX - FAQ • So how does Capex work in practice? • Capex allowances were set by Ofgem during GDPCR1 • Working from the PCR submission gives £40m - £45mallocated to xoserve from Capex Budget (all DNs) • (Not just Nexus – includes “Tech Refresh”, Conquest / IAD / IXN Replacements, as well as new UK- Link Hardware) • Forecast capital spend is added to RAV during period & then reconciled (“trued-up”) to actuals after 5 years • What does that mean for year-on-year income? • We get 1/45 of per year as depreciation plus our RoR on the RAV - recovered through transportation charges • So have we had the money? • No!!! • Its not like Opex, capex allowances aren’t recovered year on year through transportation income • All capital has to be raised through markets (debt / equity) and recovered over 45 years. • What happens to any Over / Under-Spend? • All capex must be necessary and efficiently incurred – otherwise there is a risk of disallowance. • Symmetrical sharing for over & under spends – for NGG the sharing factor is 36% • Over-spend: shareholders bear the loss of return and depreciation for the first 5 years …… • Under-spend: shareholders benefit from the recovery of return and depreciation based on the allowed capex for 5 years …... • …… before the allowance is replaced by actual spend in the RAV • Why do it this way? • Simple: to set the correct incentives: • Risk / Reward framework is designed to incentivise efficient CapEx forecasting and spending • Sets a financial incentive to ensure investment is only made once requirements are clear & regulatory sign-off achieved