Download

1 / 14

140 likes | 236 Views

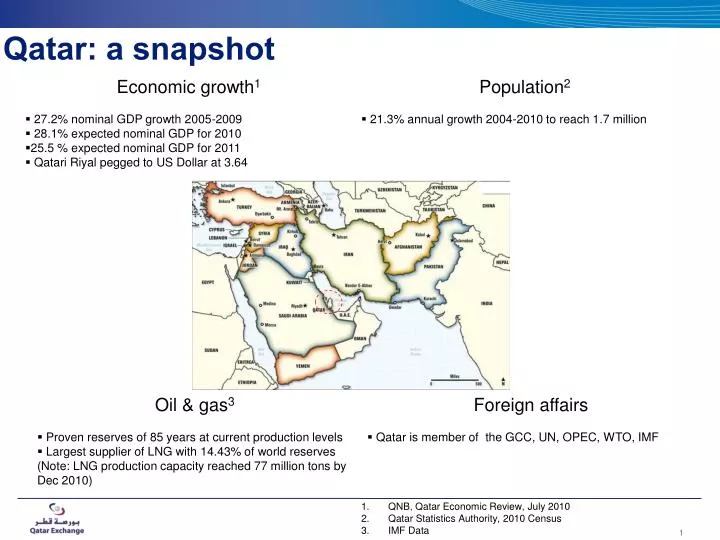

Qatar: a snapshot. Economic growth 1 27.2% nominal GDP growth 2005-2009 28.1% expected nominal GDP for 2010 25.5 % expected nominal GDP for 2011 Qatari Riyal pegged to US Dollar at 3.64. Population 2 21.3% annual growth 2004-2010 to reach 1.7 million. Oil & gas 3

E N D

Qatar: a snapshot • Economic growth1 • 27.2% nominal GDP growth 2005-2009 • 28.1% expected nominal GDP for 2010 • 25.5 % expected nominal GDP for 2011 • Qatari Riyal pegged to US Dollar at 3.64 • Population2 • 21.3% annual growth 2004-2010 to reach 1.7 million • Oil & gas3 • Proven reserves of 85 years at current production levels • Largest supplier of LNG with 14.43% of world reserves (Note: LNG production capacity reached 77 million tons by Dec 2010) • Foreign affairs • Qatar is member of the GCC, UN, OPEC, WTO, IMF QNB, Qatar Economic Review, July 2010 Qatar Statistics Authority, 2010 Census IMF Data

2010 and beyond: economy remains buoyant * Preliminary ** QNB Forecasts • Growth estimates • One of the highest growth rates in the world • Impact of global financial turmoil has been limited • Dependence on oil & gas • 2009 first year that oil & gas sector was • overtaken • Government is actively diversifying • revenue sources Source: QNB: Qatar Economic Review July 2010. QNB Capital Forecasts

QE History • 1997 First day of trading of securities at Doha Securities Market (DSM). • 1999 Investors were able to sell their purchased shares on the next day following their purchase (T+1) • 2001 Start of electronic trading project to replace manual trading systems. • 2005 Non-Qataris permitted to invest in up to 25% of the shares offered for trading. • 2009 Signed strategic partnership agreement with NYSE Euronext to transform Qatar Exchange into world-class market. • April 2011 • Implementation of DVP • SFTI • connectivity • 1998 Introduction of the Central Registration System. • 2000 Implementation of companies’ linkage project through the internet the first of its kind in the GCC • 2002 Investors able to sell their purchased shares on the same day; approval of a new market index • 2007 Became correspondent of World Federation of Exchanges (WFE). • 2010 launched NYSE Euronext Universal Trading Platform

QIA - QE - NYSE Euronext partnership 80% shareholding of QE through Qatar Holdings 20% shareholding of QE • In June, 2009 QIA and NYSE Euronext formed a strategic partnership agreement – Qatar Exchange. The Exchange is part of a comprehensive national strategy that aims to establish Qatar as a world-class international market and reinforce the Country’s position as regional financial centre by introducing new trading products, technology and international investors and issuers to Doha. Qatar Exchange is regulated by the Qatar Financial Markets Authority

QE Strategy Objectives: • Develop a successful regional and international exchange with strong domestic roots • Offer diversified range of investment and trading opportunities for investors and members • Provide access to domestic and international investors for listed companies from Qatar and abroad Competitive Advantages • Strength of the economy • Support and commitment from State of Qatar to reform financial & regulatory system • Building on solid foundations - not a start up struggling to attract business but a reasonable sized domestic exchange • Partnership with NYSE Euronext - shareholder with vested interest - expert knowledge in developing international markets

QE Strategy • Best trading environment • New trading opportunities • Efficient post trade system • Companies and IPOs meet • international standards • Cash product diversification • Derivatives • Broaden membership base • Lower barriers to entry • Diversify services provided • Broad access • International best practices • Education & training

QE Strategy • Disclosure & IR practices • IPO process • Free float requirement • Corporate actions • Indices • Cash market: ETFs & bonds • Derivatives • GCC IPOs • Dual listings with NYSE Euronext • Adjusted trading model • UTP • Liquidity providers • Lending & borrowing • Covered short selling • CCP Regulation Education • Banks • DMA • SFTI • QFCRA licensed institutions • Segregation of roles in value • chain • Foreign participation • WFE & MSCI • Education & Training • Trading hours • Global Custodians

QE: a snapshot • Growth 2004-2010 • 24.75% growth in the QE20 index during 2010 • 206% growth in the market cap • 270% growth in number of annual transactions • Investors • Foreign institutions account for 22.5% of the annual trading turnover • Qatari institutions account for 20.5% of the annual trading turnover • Over 1200 foreign institutions and funds investing in QE stocks directly QE was the best performing market in the MENA region for 2010

QE today • 41 listed companies and four sectors (plan to move to 7 sectors in line with international standards) • Total market cap: over $120 billion • QE Index covers 20 companies • Ten brokers, 3 of which just started in 2011 • Fees: 27.5 bps (charged by brokers) • 22 bps to brokers • 5.5 bps to the Qatar Exchange • SWIFT in place between QE, custodians and QCB • UTP successfully implemented– Sept 2010 • New Tick Sizes • Enhanced Trading hours

The QE Central Registry Department (CRD) • Fully integrated within QE • 25 staff • Nasdaq-OMX Equator technology • 3 Custodians: HSBC, Qatar National Bank, Standard Chartered • Dual listing with ADSM(QTEL)

The CRD’s Missions • NIN Account Openings • Exempt (off-market) Transfers • Processing of Pledges and Court Orders • Monitoring of the Brokers’ Settlement Cap • Corporate Actions • Foreign & Single Ownership Limits • DvP & Failed Trades Management • Daily Settlement Procedure • Cash-settlement Process with the QCB

The CRD in Numbers (2010) • 10,708 Exempt Transfers • 1,444 Pledges • 5,035 new Accounts opened • 263,747 Account Statements • 0 Failed Trade

2011 so far & still to come • Successful DvP Implementation • Buyer’s Compensation Enhancement • New Custodians • Securities Lending Program • Margin Lending • VaR-based Risk Management • SWIFT Developments • ANNA membership

Longer Term Plans • Creation of a fully-integrated CCP • 100% QE-owned separate legal entity • CCP for Cash, Derivatives & OTC • Settlement Cap replaced with Guarantee Fund • Creation of a Third-Party CSD • Separate legal entity with QE stake