Download

1 / 21

210 likes | 225 Views

Learn to convert nominal rates, match cash flow intervals, and tackle continuous compounding in financial contexts like credit cards and investments.

E N D

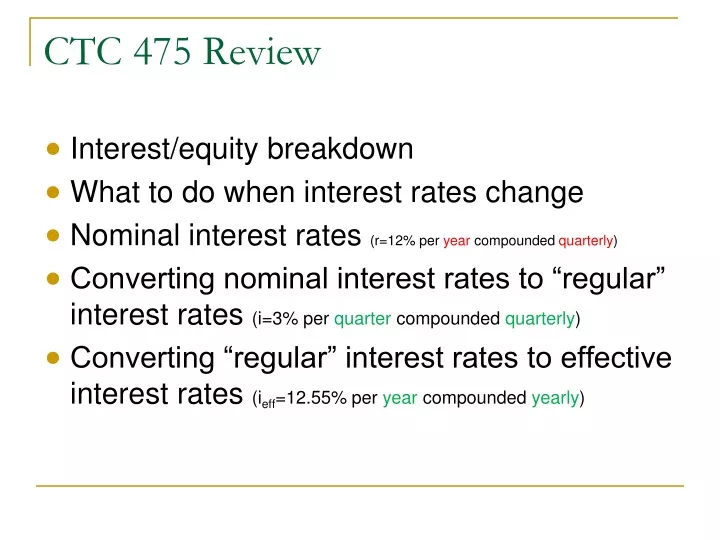

CTC 475 Review • Interest/equity breakdown • What to do when interest rates change • Nominal interest rates (r=12% per year compounded quarterly) • Converting nominal interest rates to “regular” interest rates (i=3% per quarter compounded quarterly) • Converting “regular” interest rates to effective interest rates (ieff=12.55% per year compounded yearly)

CTC 475 Changing interest rates to match cash flow intervals

Objectives • Define APR and APY • Know how to change interest rates to match cash flow intervals • Understand continuous compounding

APR and APY APR-annual percentage rate Credit cards, loans, house mortgage Nominal APY-annual percentage yield Investments, CD’s, savings Effective

What if the cash flow interval doesn’t match the compounding interval? • Cash flows occur more frequently than the compounding interval • Compounded quarterly; deposited monthly • Compounded yearly; deposited daily • Cash flows occur less frequently than the compounding interval • Compounded monthly; deposited quarterly • Compounded quarterly; deposited yearly

Cash flows occur more frequently than the compounding interval • Use ieff=(1+i)m-1 and solve for i • Note that a nominal interest rate must first be converted into ieff before using the above equation

Cash flows occur less frequently than the compounding interval • Use ieff=(1+i)m-1 and solve for ieff • Note that a nominal interest rate must first be converted into i before using the above equation

Case 1 Example Cash flows occur more frequently than compounding interval Solve for i

Example--Cash flows are more frequent than compounding interval (solve for i) • 8% per yr compounded qtrly (recognize this as a nominal interest rate and convert to 2% per quarter compounded quarterly) • Individual makes monthly deposits (cash flows are more frequent than compounding interval) • We want an interest rate of ?/month compounded monthly • Use ieff=(1+i)m-1 and solve for i

Example-Continued • Use ieff=(1+i)m-1 and solve for i • .02=(1+i)3-1 (m=3; 3 months per quarter) • 1.02 =(1+i)3 • Raise both sides by 1/3 • i=.662% per month compounded monthly

Case 2 Example • Cash flows occur less frequently than compounding interval • Solve for ieff

Example--Cash flows are less frequent than compounding interval (solve for ieff) • 8% per yr compounded qtrly (recognize this as a nominal interest rate and convert to 2% per quarter compounded quarterly) • Individual makes semiannual deposits (cash flows are less frequent than compounding interval) • We want an equivalent interest rate of ?/semi compounded semiannually • Use ieff=(1+i)m-1 and solve for ieff

Example-Continued • Use ieff=(1+i)m-1 and solve for ieff • ieff =(1+.02)2-1 (m=2; 2 qtrs. per semi) • ieff =4.04% per semi compounded semiannually

Continuous Compounding • As the time interval gets smaller and smaller (eventually approaching 0) you get the equation: • ieff=er-1 • Therefore the effective interest rate for 8% per year compounded continuously = e.08-1=8.3287%

Continuous Compounding • If the interest rate is 12% compounded continuously, what is the effective annual rate? • ieff=er-1 • ieff= e.12-1=12.75%

Continuous Compounding • Always assume discrete compounding unless the problem statement specifically states continuous compounding

Continuous Compounding; Single Cash Flow • If $2000 is invested in a fund that pays interest @ a rate of 10% per year compounded continuously, how much will the fund be worth in 5 years? • Find effective interest rate • ieff=er-1 = e.10-1 = 10.52% • F=P(1+i)5 = 2000(1.1052)5 = $3,298

Continuous Compounding • The continuous compounding rate must be consistent with the cash flow intervals (i.e. 12% per year compounded continuously won’t work with semiannual deposits)

Next lecture • Methods of Comparing Investment Alternatives