Download

1 / 19

320 likes | 832 Views

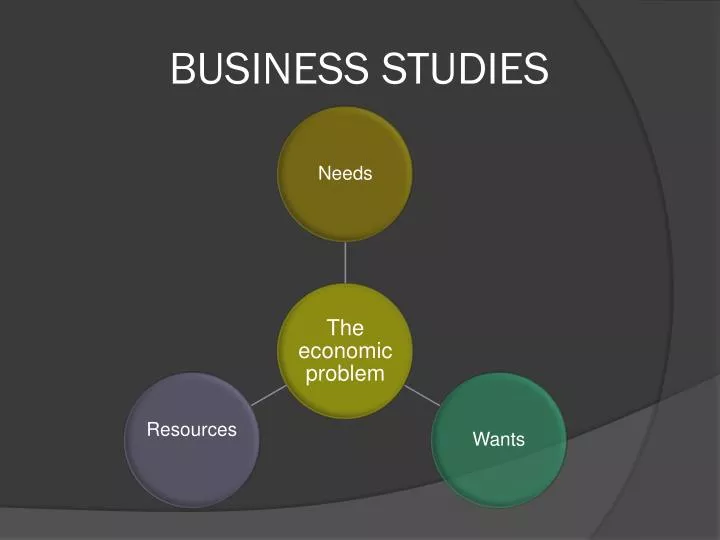

BUSINESS STUDIES . NEEDS. Goods or services essential for living. WANTS. Goods or services that people would like to have which are not essential for life. RESOURCES. Factors of production Land - Natural resources Labour - Efforts of people Capital - Finance and equipment

E N D

NEEDS • Goods or services essential for living.

WANTS • Goods or services that people would like to have which are not essential for life.

RESOURCES • Factors of production • Land- Natural resources • Labour- Efforts of people • Capital- Finance and equipment • Enterprise- skill to bring the resources together to produce a good or service. (Person: entrepreneur)

SCARCITY • The factors of production are limited in supply. • There are never enough to produce all the needs and wants of a whole population. • There is an economic problem.

THE NEED TO CHOOSE • As there are limited resources for unlimited wants, people have to decide which wants they will satisfy and which they will not.

OPPORTUNITY COST • Itisthenextbestalternativegiven up bychoosinganotheritem. • A B • Car A or car B? • The individual chooses car B. • Therefore, car A istheopportunitycost.

COSTS – REVENUE - PROFIT. • COSTS- Expenses incurred by a firm in producing and selling its products. They include expenditure on wages and raw materials. • REVENUE- It is the amount of money a firm gets from selling a good or service. • PROFIT- It is the difference between what it costs to produce something and what it is sold for. (Price-Costs).

COSTS • FIXED- Are the same regardless the production. • VARIABLE- Increase with the amount produced. • TOTAL- Are fixed costs + variable costs. • AVERAGE- Are Total Costs devided by the output.

EXERCISE Team textiles sells shirts at £ 24 each. Complete the chart below. Is the firm making any profit?

EXERCISE Complete the following table for Team Textiles, assuming that its fixed costs are £ 4000 each week and its variable costs are £ 12 for each shirt produced.

EXERCISE Complete the following table for Team Textiles.

BREAK- EVEN POINT • Break – even point is the point at which an organisation covers its costs with the money it makes through sales. • A break-even chart is prepared in advance to see how much the business needs to sell at a particular price.

BREAK- EVEN POINT • Break – even point is expressed in terms of the quantity of items made or sold. • An alternative method for calculating break-even is to devide the total fixed cost by the contribution from selling each unit. • The contribution of a product is selling price less variable cost.