Download

1 / 2

20 likes | 27 Views

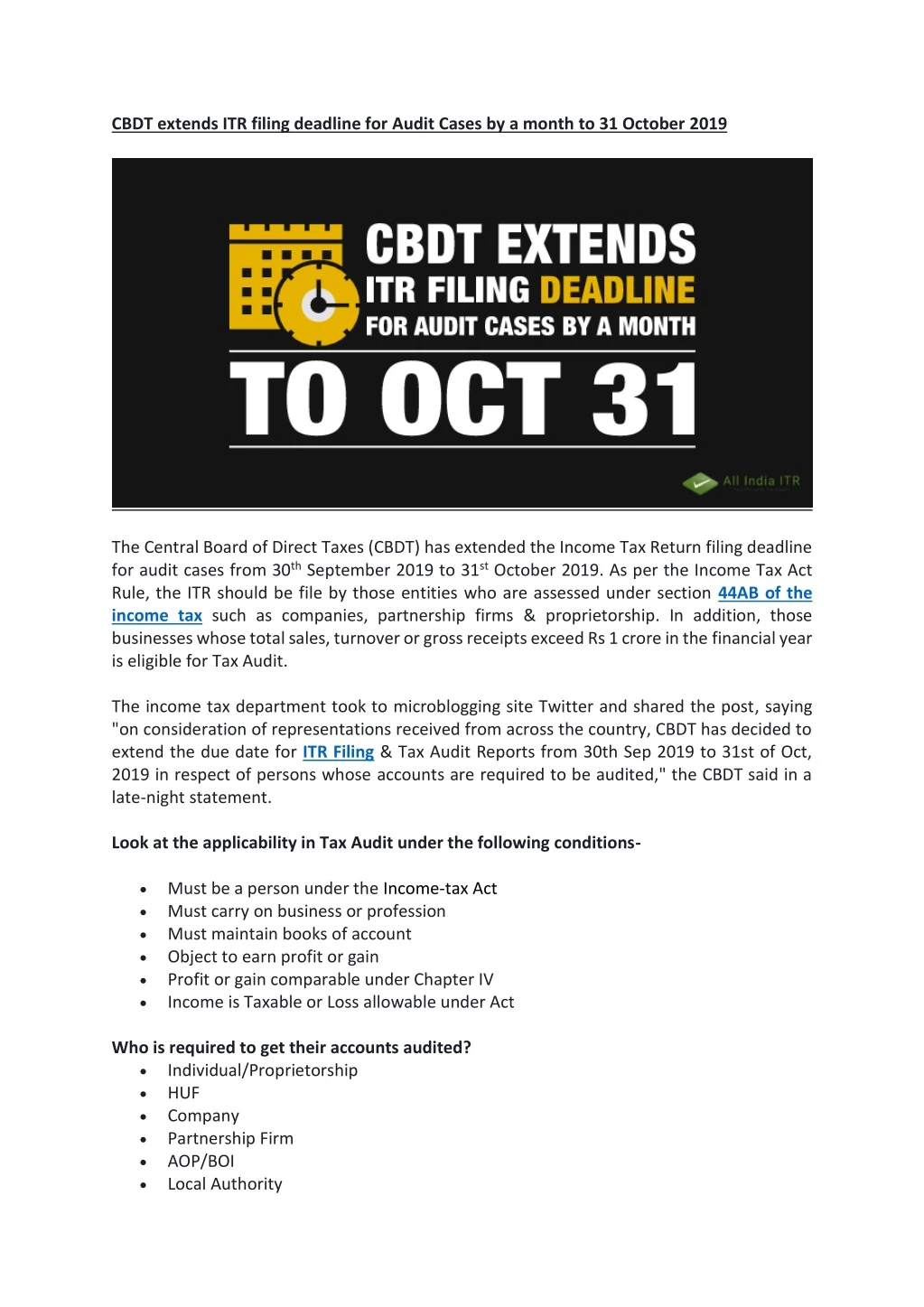

The Central Board of Direct Taxes (CBDT) has extended the Income Tax Return filing deadline for audit cases from 30th September 2019 to 31st October 2019.

E N D

CBDT extends ITR filing deadline for Audit Cases by a month to 31 October 2019 The Central Board of Direct Taxes (CBDT) has extended the Income Tax Return filing deadline for audit cases from 30th September 2019 to 31st October 2019. As per the Income Tax Act Rule, the ITR should be file by those entities who are assessed under section 44AB of the income tax such as companies, partnership firms & proprietorship. In addition, those businesses whose total sales, turnover or gross receipts exceed Rs 1 crore in the financial year is eligible for Tax Audit. The income tax department took to microblogging site Twitter and shared the post, saying "on consideration of representations received from across the country, CBDT has decided to extend the due date for ITR Filing & Tax Audit Reports from 30th Sep 2019 to 31st of Oct, 2019 in respect of persons whose accounts are required to be audited," the CBDT said in a late-night statement. Look at the applicability in Tax Audit under the following conditions- Must be a person under the Income-tax Act Must carry on business or profession Must maintain books of account Object to earn profit or gain Profit or gain comparable under Chapter IV Income is Taxable or Loss allowable under Act Who is required to get their accounts audited? Individual/Proprietorship HUF Company Partnership Firm AOP/BOI Local Authority

Co-operative Objective of Tax Audit As the name suggests, the Tax Audit specifies the proper analysis or audit of accounts of any business or profession carried out by taxpayers from an income tax perspective. Even though it makes the process of income computation for filing of return of income easier. Here are the objectives of a tax audit- Ensure proper analysis and correctness of books of accounts and certification of the same by a tax auditor. Checks frauds and malpractices in filing income tax returns. To note down any discrepancies while reporting observations of books and accounts by a tax auditor. To report prescribed information such as tax depreciation, compliance various provision of Income Tax Act law. Penalty for Non-Compliance of Tax Audit Non-compliance of tax audit regulations by taxpayers attracts a penalty of whichever is lower from the following: 0.5% of total sales Turnover or Gross receipts Rs. 1,50,000 For more details about efiling of income tax return online visit our website: https://www.allindiaitr.com