Download

1 / 21

210 likes | 292 Views

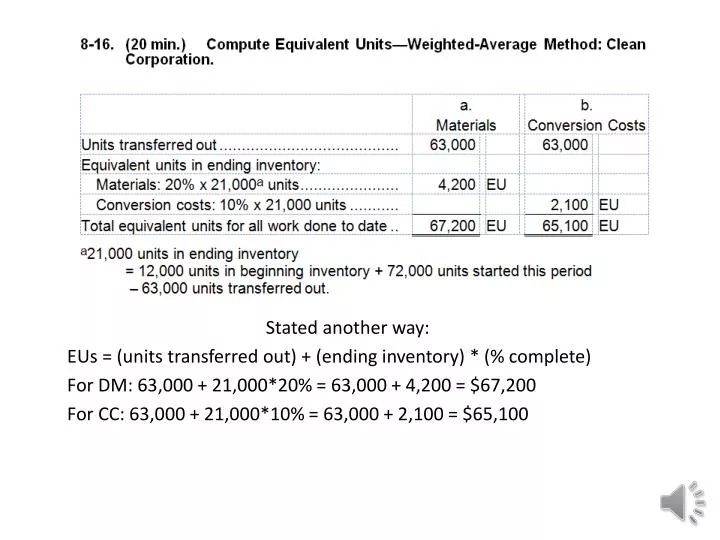

Stated another way: EUs = (units transferred out) + (ending inventory) * (% complete) For DM : 63,000 + 21,000*20% = 63,000 + 4,200 = $67,200 For CC: 63,000 + 21,000*10% = 63,000 + 2,100 = $65,100. 8-21: Compute Equivalent Units—Ethical Issues: Aaron Company.

E N D

Stated another way: EUs = (units transferred out) + (ending inventory) * (% complete) For DM: 63,000 + 21,000*20% = 63,000 + 4,200 = $67,200 For CC: 63,000 + 21,000*10% = 63,000 + 2,100 = $65,100

8-21: Compute Equivalent Units—Ethical Issues: Aaron Company.

8-21: Compute Equivalent Units—Ethical Issues—cont’d • The change will reduce the unit cost for the units transferred to finished goods. • $$$/(larger EUs)=smaller unit cost • Larger % completion means higher EI cost • It is not ethical; there is no reason to believe the change reflects anything other than a desire for reporting better results. • What is violated in IMA Code?? (p. 23) • It is unlikely to be successful for long. An accounting system keeps track of actual costs. If a manager postpones reporting them this period, they will be reported next period or shortly thereafter.

Institute of Management Accountants Code of Ethics Competence Confidentiality Integrity Credibility

Competence Members have a responsibility to: 1. Maintain an appropriate level of professional expertise by continually developing knowledge and skills. 2. Perform professional duties in accordance with relevant laws, regulations, and technical standards. 3. Provide decision support information and recommendations that are accurate, clear, concise, and timely. 4. Recognize and communicate professional limitations or other constraints that would preclude responsible judgment or successful performance of activity.

Confidentiality Members have a responsibility to: 1. Keep information confidential except when disclosure is authorized or legally required. 2. Inform all relevant parties regarding appropriate use of confidential information. 3. Refrain from using confidential information for unethical or illegal advantage. 4. Monitor subordinates’ activities to ensure compliance.

Integrity Members have a responsibility to: 1. Mitigate actual conflicts of interest, regularly communicate with business associates to avoid apparent conflicts of interest. Advise all parties of any potential conflicts. 2. Refrain from engaging in any conduct that would prejudice carrying out duties ethically. 3. Abstain from engaging in or supporting any activity that might discredit the profession.

Credibility Members have a responsibility to: 1. Communicate information fairly and objectively. 2. Disclose all relevant information that could reasonably be expected to influence an intended user’s understanding of the reports, analyses, or recommendations. 3. Disclose delays or deficiencies in information, timeliness, processing, or internal controls in conformance with organization policy and/or applicable law.

8-21 concluded 3. It is unlikely to be successful for long. An accounting system keeps track of actual costs. If a manager postpones reporting them this period, they will be reported next period or shortly thereafter.

8-52 cont’d These costs, plus the cost of material, make up the cost of units completed and the ending inventories of WIP. See next slide…

8-52 cont’d The material costs per unit are: Cost of units transferred to finished goods:

8-52 cont’d Work-in-Process Ending Inventory, Stitching. * 140 units, 40% complete

Pr. 52 concluded Customizing Department:. * 50 units, 20% complete

Comments on 8-52 • The problem is a little odd in that there are two process-costing-type departments and no job costing department. • It seems that the Customizing department would take a job-costing approach. It might perform truly custom work on the different models, such as adding custom designs or corporate trademarks, etc. • If so, individual jobs would be tracked in the Customizing department for truly custom work.