Download

1 / 4

40 likes | 84 Views

Do you have a PAYDEX business credit score, but you’re not sure exactly what went into it, and how to read it? It’s time to start decoding your PAYDEX business credit score. For more details please visit at https://www.creditsuite.com/blog/decoding-the-paydex-business-credit-score/

E N D

Decoding the PAYDEX Business Credit Score https://creditsuite.com/blog/decoding-the-paydex-business-credit-score/

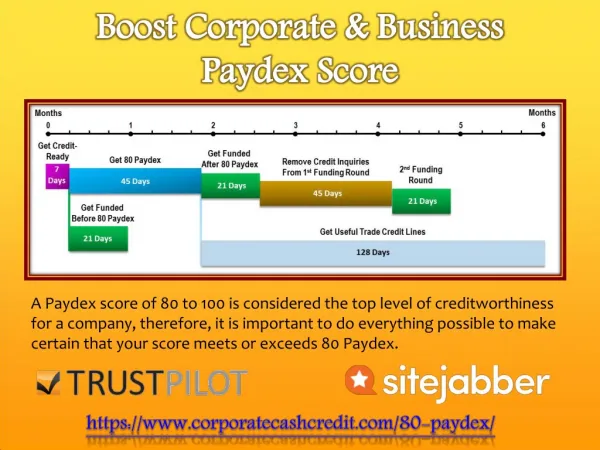

What is PAYDEX? Do you have a PAYDEX business credit score, but you’re not sure exactly what went into it, and how to read it? It’s time to start decoding your PAYDEX business credit score. A PAYDEX business credit score serves as Dun & Bradstreet’s dollar-weighted numerical rating of how a business has paid its bills over the past year. D & B bases their scoring on trade experiences as reported by various vendors. So these can be a business’s landlord, suppliers, etc. It depends on what will apply to your particular circumstances. The Dun & Bradstreet PAYDEX Score is reported in a range running from 1 to 100. As you might expect, higher scores mean a better payment performance. That is, your business pays its bills on time or early, and it pays them as close to fully as possible. These can keep your PAYDEX score in a better range. https://creditsuite.com/blog/decoding-the-paydex-business-credit-score/

Getting Your Business’s First PAYDEX Score Your PAYDEX score does not start to be figured until your business has a DUNS number, so that comes first. There are other means of improving your PAYDEX score, including establishing business credit which is separate from your personal credit. Your PAYDEX score comes from your DUNS number and your payment history, so it’s imperative to get your DUNS number first. https://creditsuite.com/blog/decoding-the-paydex-business-credit-score/

The Basis of Your Business’s PAYDEX Score Dun & Bradstreet’s PAYDEX business credit score has a basis in payment details which are reported to the bureau. Or they may be reported to data-gathering businesses partnering with the agency. D & B uses this data, as well as a credit score and financial stress score, so as to advise just how much credit a creditor should extend to your business. So as to get a PAYDEX number, you have to have a DUNS number, plus the bureau will need to have reports of your payments with four or more vendors. Your business’s PAYDEX score reveals if your payments are typically made on schedule or ahead of schedule. As you might expect, a higher number is better. https://creditsuite.com/blog/decoding-the-paydex-business-credit-score/